Morningstar Is Getting Closer On Its Intrinsic Value Figure for Berkshire Hathaway

It’s been 1-2 years since we talked about the intrinsic value of Berkshire Hathaway. The last time I publicly commented in any meaningful way was to say that I thought Morningstar was wrong in its model. This put me in the interesting position that rarely happens: I thought intrinsic value was higher than the analysts who were publicly writing about it. Normally, I’m the one exclaiming that the estimates and variables used were too rosy.

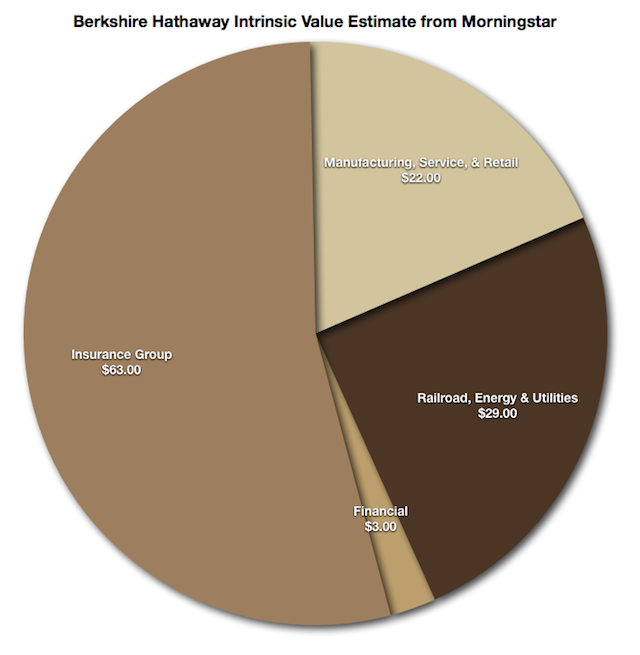

Back then, Morningstar said it believed Berkshire Hathaway Class B shares were worth $89 each. If the company had broken up by unit, the insurance businesses were worth $49, the manufacturing, service, and retail businesses were worth $16, the railroad, energy, and utility businesses were worth $20, and the financial business was worth $4. I pegged intrinsic value between $100 and $115 per share with a maximum justifiable valuation at $132 per share (e.g., you were going to buy a very large block for a very long time or take control of the business).

I spent much of 2011 and, if I recall, 2012, buying additional shares of Berkshire Hathaway for my own accounts, as well as those of my family members; though I did have to sell a block of shares at one point to help come up with the cash necessary to buyout the other members of one of my limited liability companies, which offered far higher returns than even a cheap Berkshire Hathaway ever could. In September of 2011, the stock hit a low of 1.075x book value, which is the most undervalued it has ever been in my lifetime. It’s since rebounded a bit, and trades at $96 per share against a book value of $76 or so.

The new model for Berkshire Hathaway’s intrinsic value seems much more reasonable, though I still think they are a bit too low. Morningstar argues that, were it split into four different companies, the sum-of-the-parts valuation would be as follows: That is a grand total of $117 per Class B share for the conglomerate itself.

That is a grand total of $117 per Class B share for the conglomerate itself.

I think the intrinsic value is between $125 and $130 per share, myself, compared to the $96 stock price. If the company is fairly valued 10 years from now – and there is no guarantee that it will be or that some horrific disaster won’t befall the firm or the nation – in a normal, ordinary blue-sky world of an average range of returns, the stock should have an intrinsic value of $250 to $500 per Class B share were there no dividend distributions. (Large dividend distributions, or even the introduction of an on-going dividend policy, would change that figure as less capital would pile up for management to invest.)

I’m content to stick with the no-dividend policy at present. I have shares on my balance sheet that were bought at a fraction of current market value and intrinsic value, paid for back when I was a student. I’m not really fond of the idea of selling unless it is for portfolio reasons (e.g., too high a concentration due to other factors), even if the stock became overvalued. The moment Warren Buffett and Charlie Munger are gone, however, I will probably be one of those in the chorus of people demanding some sort of reasonable distribution policy. The successors can’t poorly allocate that which has already been sent to the owners and empirical study after empirical study has shown that dividend policies force discipline onto management. Buffett and Munger don’t need discipline; they have it in spades.

Were Berkshire Hathaway to ever reach the limits of its size, and turn on the spigot, it would fundamentally transform my public stockholdings. There would be money coming in from nearly every account and in amounts that would significantly increase the cash I had to redeploy from common stock investments. I have one personal retirement fund where roughly half the assets are in low-cost Berkshire Hathaway shares bought over time. Even a small 2% to 3% annual dividend would radically change the characteristics of that plan. That wasn’t by design – I just bought what was cheap at the time and was appropriate for a very long-term, low-risk collection of assets.

This is on my mind today because I’m doing my first quarter review of all of our holdings; where the money is, how it is invested, what the correlated risks are, et cetera, and I happened to mention it in the post of Coca-Cola earlier.

Reader Comments (6)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

TomG

February 5, 2013

Hi Joshua,

Would you be able to share the method(s) you use to calculate the intrinsic value of companies such as Berkshire Hathaway? It is my understanding that there are various methods that can be used in order to gauge a fair price for a particular stock.

Keep up the great articles - they're helping me on my path to becoming a better investor!

Joshua Kennon

February 26, 2013

Replying to TomG

Berkshire Hathaway is a different situation. You have to split up the parts and value each of them individually. For example, you need to break off the insurance companies as their own group, and value it as you would a stand-alone insurance business. Then the same for the power plant utilities. Then the same for the railroad. Then the same for the other industry groups.

The short version: Any time it gets near book value, it's a steal. The companies are worth far more than the current book value. It's attractive all the way up to 1.5x book value, in my opinion. I would not pay more than 2x book value. Anytime it is at 1.25x book value or less, I am probably writing checks (though I did have to sell a big block last year to fund the buyout of one of my private companies, even though I would have loved to have hung on to the stock; debt doesn't sit well with me so I didn't want to go to a bank.).

One very important caveat: Those figures could change if Berkshire Hathaway engages in a huge share repurchase program. Why? It has to do with the way the accounting rules work under GAAP. When stock is bought back, the figure is taken out of the equity section of the balance sheet, which reduces the carrying book value. However, the company actually gets more attractive if the repurchase price was reasonable. That is why a company like AutoZone has a book value of NEGATIVE $43.63. The firm has bought back massive quantities of shares over the past decade, and it's been a great deal for long-term owners. The retailer is generating $1.2 billion in operating cash on a book value of negative $1.5 billion. That's an accounting quirk. Once money is returned through this backdoor method, the multiple-to-book-value isn't really useful. It gets skewed too far to be indicative of anything meaningful.

There are also a few other cases you have to watch out for that. Real estate firms that build projects can actually, in certain cases, capitalize the interest expense it paid and classify it as an asset on the balance sheet, meaning that past interest expense paid is counted toward positive book value! It sounds insane, but it makes sense in the scheme of things when you understand why it is done; still it can be a problem that makes multiples to book value not work very well when valuing firms in that type of sector.

FratMan

February 14, 2013

So Buffett got his hands on Heinz...

Joshua Kennon

February 14, 2013

Replying to FratMan

I had just woken up and checked the blog on my iPad. This comment caused me to flip over to the news, jump straight up on the mattress and wake my spouse by yelling, "We just bought Heinz!".

If I recall, you have a position as one of your core 4 or 5 holdings, don't you? This should mean a fairly relatively large influx of cash for you if that is the case.

You have some shopping to do.

(Pro tip: If you don't think the bid will be raised - which is a gamble, but with Buffett, a higher bid is unlikely because he tends to make take-it-or-leave-it offers - if the market price exceeds the offering price, you might consider selling to take advantage of the overvaluation, plus you should pay just the ordinary commission, not the reorganization fees or other expenses a brokerage firm might charge you for handling the paperwork depending on the situation. It can also save you several months of just sitting around, waiting for your stock to be taken. Whatever happens, do not feel pressured to do something or buy something just because you are suddenly sitting on a pile of cash. Cash tends to burn a hole in investor's pockets. Unless you are dollar cost averaging into a low-cost index fund (which I think a majority of people should do), training yourself to overcome the need to constantly acquire, and instead wait for something that is attractive, is a lucrative discipline.)

FratMan

February 14, 2013

Replying to Joshua Kennon

Thanks! I was hoping I could be the one to break the news. Congrats on taking the Ketchup-maker off my hands--I hope it takes care of you as much as it has me.

And you are correct. Heinz had been in my top four (before today's run up, dwarfed only by Johnson & Johnson, General Electric, and Conoco Phillips in current market value). I had actually considered doubling down on Heinz a couple months ago, but decided to buy BP instead (unfortunately, at a price not much lower than the current $43 market price). Of course, I couldn't resist the urge to break out the calculator and see what I would have had if I "doubled down" on Heinz, but luckily I was able to use my mental strength to counter that impulsive knee-jerk reaction of greed* by reminding myself: (1) I acted on information I had at the time about Heinz and BP, obviously without this Buffett purchase expectation, and (2) I largely agreed with your articulation recently that if we can only find a couple places to put our money, we're doing something wrong. It fits in well with my goal to have enough passive income so I never have to rely on one employer, and I'd much rather have enough holdings so I can think of each as a collection of my 20-50 employees rather than only having a few stock holdings that were effectively by employer, even though the income came passively.

To put #2 in coherent English, I'd never want to be as dependent on the income from one stock holding as some people are on their employer, so I don't want to create stock holdings that are effectively surrogate employers. Although this would have been the "good side" of owning a concentrated portfolio, I am much more concerned about avoiding the "bad side" of a concentrated portfolio, so that made it very easy to make my peace with not doubling down.

And you are correct, I sold all of my Heinz today in a tax-protected account. I agreed with your statement that Buffett is unlikely to raise the price, and as soon as I saw the price clear $72.50 this morning, I did my first ever market order with a meaningful amount of money. Boy, that was a mistake. I got $72.45 for it instead of around $72.54-$72.56. I'm not going to cry about a dime, but I have no idea what happened in that 1-2 second stretch that made the difference between selling at greater than the settle price and below it. Yeah, I'll never do another market order. Relatively cheap lesson learned.

You're absolutely right on that last line. This is the highest amount of cash I've ever held (my temperament is best suited for full investment unless we enter a world where consumer staples are trading at 35x earnings and therefore holding can't be justified), and it will be interesting to see what comes next. You're right--shopping time. I'm probably just going to put it off for a couple weeks, and then spend some time thinking about what to do next. Thanks for your last line there. I probably would have just dumped it into three coequal piles of Coca-Cola, GlaxoSmithKline, and Becton Dickinson and then been done with it, but now I'll give this more deliberation. Thanks Joshua.

*I'd become a sad little man if I reacted to good fortune by thinking, "I could easily have more..." I'm glad I was able to successfully defeat that impulse. I hope that always continues to be the case.

FratMan

March 5, 2013

Replying to FratMan

Decision got made. Heinz money got put into roughly equal piles of BP, IBM, Wells Fargo, and Royal Dutch Shell B shares.