A Case Study of Eastman Kodak

How the Bankruptcy of One of America’s Oldest Blue Chip Stocks Would Have Turned Out for Long-Term Investors

One year ago, Kodak declared bankruptcy after more than 130 years in business as a leading blue chip firm that gushed profits for its owners. I wrote Kodak’s demise at the time.

In the final decade, those profits disappeared and the inevitable spiral into wipeout occurred. Some people use Kodak as an example of how even the best companies can make you lose everything but, in doing so, display the same folly I’ve been warning you about for years: You cannot just look at a stock chart to gauge the performance of a business. You have to do your homework and perform a case study to understand what happened over time.

Before we begin the case study, I apologize for an odd bit in the math: I had wanted to do an apples-to-apples comparison of our case study of General Mills, but after I did the calculations, I realized that I should have begun in 1987 not 1986! With Kodak declaring bankruptcy last year, there was no financial data for 2012, so counting backward ended me one year further in the past than should have been the case. I didn’t catch it until the end and didn’t want to have to redo all of the work.

I performed a few back-of-the-envelope calculations and figured out that it wouldn’t matter much had I begun a year later; depending on the year you invested, you would either add or subtract a percentage point for the most part. That’s a by-product of holding for 25+ years, which is half of an investing lifetime. Starting cost basis figures matter a lot less when you get into the powerful effects of compounding.

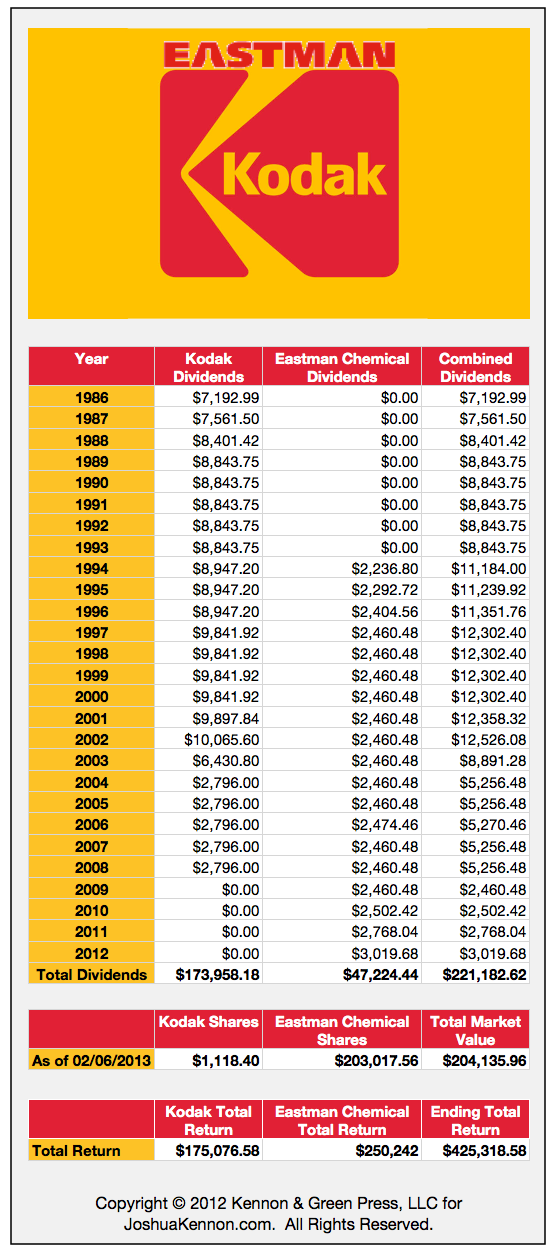

A $100,000 Investment In Eastman Kodak 25+ Years Ago

Imagine it is 1986. You have $100,000 in cash. You decide to invest it in shares of Eastman Kodak, the photography and chemical giant. On the first day of trading that year, January 2nd, you invest the entire amount at the opening price of $26.82 per share. Ignoring the relatively small commission you would have owed, you would end up with 3,728 shares. You have no intention of buying or selling additional shares, so you will incur virtually zero expenses or management costs for the remainder of your holding period.

Over the next couple of decades, three events standout that are of importance to you:

- In October of 1987, shares split 3-2. This brings your total share count to 5,592 shares of Eastman Kodak

- On January 4th, 1994, Kodak spun off its Eastman Chemical division, mailing 1 share to stockholders for every 4 shares of Kodak owned. With 5,592 shares of Kodak, you received 1,398 shares of the chemical business.

- In October of 2011, Eastman Chemical split 2-1, bringing your total chemical shares to 2,796

You do nothing. You sit back for years and collect cash dividends from your investment, which start at a rate almost exactly the same as the then-long-term-Treasury-bond-yields, waiting for the bankruptcy filing shortly after the end of 2011. What happens? How did you fare? Was your $100,000 lost? Let’s take a look.

At the end of it all, before taxes, you are sitting on $425,319 from your $100,000 investment. Of this, $221,863 came in the form of cash dividends, which were mailed to you over the years. The other $204,136 is from, mostly, the market value of the Eastman Chemical shares, with a small amount available were you to liquidate the bankrupt Kodak shares, which have now been delisted.

Not only did you not lose 100% of your money, you actually compounded at around 5.5% per annum before taxes even with the near total wipeout of the Kodak shares. (It’s difficult to say what the after-tax figure would be because it depends on your income tax bracket and whether or not you held the shares in a tax-shelter or retirement plan of some sort. Then, in the midst of this holding period, dividend taxes were slashed to much lower rates than ordinary earned income. At the end, you’d also have a tax credit for the capital loss, which could shelter future income had you held your stock in a plain vanilla brokerage account.)

Had your Eastman Kodak shares been held as part of a collection of high quality stocks, you still would have had fantastic returns. If you put $100,000 into Eastman Kodak and $100,000 into General Mills, 1 out of 2 of your initial stocks would have gone bankrupt and been wiped out to nearly $0 per share. That is a catastrophic failure rate. However, your $200,000 starting portfolio would have ended up worth $2,523,400+ and you’d own shares of a chemical business, a restaurant chain, and the cereal firm. You would have compounded your money roughly 10% pre-tax.

Let me repeat the lesson: You cannot just look at stock charts to gauge the performance of your holdings. Sometimes, you can walk away with more money even though your shares experience a 100% loss. Wipeout losses are always bad – you should do everything you can do avoid them – but they are often not the entire story.

The Bigger Lessons – Warning Bells Should Have Been Going Off Nearly a Decade Before Kodak’s Bankruptcy

As a part owner of the business, in 2000, when you received your annual report in the mail, you would have seen per share profits at $4.59 fully diluted. At the same time, digital cameras were starting to show up on the scene, but let’s imagine you didn’t notice that the days of taking physical film, dropping it off at a drug store or photo labs, and waiting days, or weeks, to pick it up were coming to an end.

In 2003, diluted earnings per share had fallen to $0.83, a drop of 82%.

That should have set off alarm bells because you need to focus on the profits and dividends your businesses generate. Without profits, there can be no dividends. Certainly, good companies are going to experience decreases in profits during times of economic distress but 2003 had already witnessed the recovery of the post-2001 recession caused by September 11th. Things were good elsewhere in the economy.

The falling profit line would have driven your earnings yield down. It would have shown up on your spreadsheets when you saw your portfolio’s share of the net earnings collapsing. That warrants a serious investigation. Good holdings should be increasing that figure over time.

Even worse? Shortly thereafter, Kodak had to restate earnings to $0.66 per share – a huge further decrease! That means something was going horribly wrong and management didn’t have a handle on the accounting records. That is the second major red flag.

The following year, profits fell to $0.28 per diluted share.

To perform the case study on an Eastman Kodak investment, including the bankruptcy of the photography business, I went through almost 30 years of records, adjusted for splits, and added up the dividend accumulations and ending share values. Then I had to double check it all for errors, line by line. This sort of exercise is useful. I would encourage you all do to it if you are interested in businesses.

Think about where you are at this point. The rest of the United States is experiencing a huge boom due to technology and real estate. Life is good. You own 5,592 shares of Kodak that, in 2000, generated net earnings of $25,667, of which $9,842 or so was paid out to you. Now, in 2004, your stake generated net earnings of $1,566 and the company dipped into its reserves to pay dividends of $2,796 to you; profits alone couldn’t cover those distributions.

The profit drop of your stake from $25,667 to $1,566 while the rest of the world is having a party and a major threat (digital cameras) shows up on the scene should have sent you into utter panic. The stock was trading at $32.25 at this point, giving your Kodak shares a market value of $180,342.

You have $180,342 invested in a company that generates $1,566 in profit with that money. You are earning a return of 0.86%. At that exact same moment, the moribund, boring oil stocks that were too big to grow, like Royal Dutch Shell, were offering earnings yields of 9.84% with dividend yields of 4.22%.

Why would you have sat on your hands, owning a company that already dominated its market (in a market that was dying to low-cost digital cameras (in which it would have no advantage)), had no real growth potential, was trading at an insanely high valuation relative to profits and dividends, and couldn’t even figure out its own accounting records, at a time when you could have switched into a boring-as-watching-paint-dry oil giant that generated – literally – 1,000% more profit? Even if you had bought into a firm like BP, which was about to experience the worst oil spill in history a few years later, you would have still come out miles ahead of the game.

It’s one thing to accept those kinds of valuations and risks with a start-up that could make you millions of dollars overnight. It’s patently stupid to accept them as part of owning a large, established, slow growing business in a declining industry.

For me, the huge warning sign would have been the dividend cut between 2002 and 2003, when the 5,592 shares went from generating dividends of $10,066 per year to $6,431 per year. With a further cut to $2,796 the year after that, I think most reasonable long-term income-oriented investors would have been out by 2004. It wouldn’t have mattered if the stock had fallen off its highs; what counted would be cost basis, not the peak of the share price. Despite the troubles, you would have made a good amount of money from your initial investment, plus you’d own the chemical shares. The opportunity cost of holding those remaining 5,592 shares of the photography business would have been too high relative to the competing uses. Kodak should have been jettisoned from the portfolio.

Telling a Kodak from a General Electric or Wells Fargo

How do you separate that sort of development from the dividend cuts experienced by General Electric and Wells Fargo during the Great Recession? Why was I buying more of those firms as few years ago despite the falling profit? In those cases:

- The businesses were not experiencing isolated trouble; there was a macroeconomic superstorm hurting nearly everybody

- The companies were in industries that were growing and thriving, not at risk of becoming extinct

- The businesses dominated their respective competitors

- The businesses had strong balance sheets that would be quickly repaired by using the money that had been going out as dividends to fill the holes caused by the housing bubble collapse

This is why I am so insistent that some people should not own individual stocks – they need to buy only low-cost index funds. If you can’t look at a business and understand how it makes money, and think about the threats to those profits or the opportunities for those profits to grow, you need to stop holding specific equities! You are speculating, even if you don’t realize it. You are going to convince yourself that Wall Street is a giant casino, when the problem is really your own incompetence.

One final warning: We sometimes use earnings yield as a starting point to look at valuation but you cannot rely on it as the sole measure of how cheap a business is. In 2000, when things looked good at Kodak, those $4.59 per share earnings came from a stock price of $39.38, representing an 11.67% earnings yield. The stock had fallen substantially from the year before when the earnings yield was 6.53%. The market was telling you something was going on and you should have paid attention. Kodak was, at this moment, something referred to as a “value trap”.

Reader Comments (11)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

weixiluo

February 6, 2013

Lesson to be learned : Business paying out dividends held in the long term can significantly protect capital from wipeout risk, not mentioning that business paying out dividends are generally safer in the first place because they force discipline over management.

lokgp

February 7, 2013

Thanks, Joshua, for the great work and article!

Michael Starke

February 7, 2013

I appreciate you going into further detail on Kodak. For me, the big takeaway from this is that the mantra "on what terms and at what price" is not a static determination. It's obvious from a study like this that a periodic review of ones holdings is essential to ensuring a solid portfolio.

Also, I think it's important to understand what a strong indicator dividends happen to be. The "proof of the pudding is in the eating" and "the proof of the company is in the strength of it's dividends." Distributing a dividend is the company "tipping its hand" regarding its forecast for the future, and proving that its past performance was not overstated. They actually have to *have the money* in order to send it out to shareholders.

Dividend cuts (unexplained by macro phenomena,) or a lack of dividend growth for an extended period of time, are two of the easiest rationalizations that I have for selling out of a position. There are enough choices of securities out there to invest in that I usually can find something to replace it in short order.

Joshua Kennon

February 7, 2013

Replying to Michael Starke

That last paragraph contains a great point - the lack of dividend growth for extended periods of time essentially amounts to a dividend cut when factoring inflation into the results. To me, if you're dealing with a mature company that doesn't have a lot opportunities to invest surplus capital, that is a big flag to me. I have passed on a few companies in the past few months alone because of that very situation.

Michael Starke

February 8, 2013

Replying to Joshua Kennon

Exactly! In the past I've been known to sacrifice a bit on current yield when I can see the potential for future dividend growth that's above-average (backed up by earnings growth that supports a relatively steady payout ratio). (Payout ratio is a whole other topic that I'd be curious to hear your thoughts on, if you have an existing post, or time to write one.)

Have you ever done a post regarding yield on cost? I remember reading that you're in favor of selective reinvestment of dividends for your own portfolios, and I am generally in favor as well, but what do you do in cases where you cannot find a new position that's "worthy?" Do you sit on cash or expand an existing position?

Marc

February 7, 2013

This would be the case that you'd turn out well if you didn't reinvest dividends... but if you had automatically reinvested dividends (which a lot of people recommend for the purpose of compounding), then you would have been cleaned out on the Kodak share portion. Is the lesson learned that we shouldn't reinvest dividends in the original company? Or that should we should always reinvest dividends but perhaps in something more diversified?

Joshua Kennon

February 7, 2013

Replying to Marc

I'm actually, as I write this, working on a huge case study of McDonald's that I (hope) to publish in a few hours. The issue of dividend reinvestment is going to have a huge influence on the results there, as well, so this is an excellent question.

If you decide to reinvest your dividends, there are two ways to do it. The first is to reinvest it in the shares of the business that distributed the dividend.

The second is to have all of the cash pool at the bottom of the account and then, when combined with new funds, serve as the money that is used to buy other investments. (Think of the Warren Buffett model - Nebraska Furniture Mart makes profits and then pays dividends to Omaha twice a year, where the money is commingled with the dividends GEICO, Dairy Queen, etc. and then used to buy other businesses.)

I am valuation driven. I compare stocks to all other assets and simply want to buy the most future cash I can. That means I tend to opt heavily for the second method. At this moment, virtually all of my household, business, and personal retirement accounts fall into that second category. The dividends pool and are then redeployed periodically. If I am buying shares of a new business, they are funded, in part, by my dividends from General Electric, Johnson & Johnson, Royal Dutch Shell, the distributions from my limited liability company investments, the copyright income from my publications, rents from real estate, et cetera.

The reason I like that method is because I could never have brought myself to reinvest automatically in shares of, say, Coca-Cola when it was more than 50x earnings. I just couldn't do it. It's going to end poorly. Likewise, when Kodak started having trouble with the underlying profits, I wouldn't have wanted my money to go back into a firm that would have been on my sell list.

In the case of Kodak, the reinvested dividends would have led to much more Eastman Chemical stock at the time of the spin-off so you would have recaptured some of the money you lost. But you are correct in that your ultimate results would have been far worse.

Bottom line: If you are good at capital allocation, have the skill to evaluate a business, and manage the portfolio well, I think the second method (dividend pooling then reinvestment) is superior. If you don't know what you are doing, or you don't want to think much about your holdings, I think the first method (automatic reinvestment into the security distributing the cash) is superior, provided that it is part of a reasonable diversified collection of high quality holdings.

Of course, I think if someone can't evaluate companies, they should probably just own a low-cost, dollar-cost-averaged index fund that mimics something like the S&P 500 but there are all sorts of reasons people might want to own individual securities. If you worked at McDonald's or psychologically preferred owning specific businesses you could see were doing well - like Walmart or Pepsi - that's your prerogative.

That is just my personal opinion. Others may feel differently.

Joshua Kennon

February 7, 2013

Glad you found it useful =) I'm working on one about McDonald's that I hope to publish tonight but it's complicated due to the Chipotle spin-off. If you liked this post, you should probably check that one out, as well, when I can get it online!

Mirmer

July 29, 2014

If I follow your strategy of using DRIP... I think it would be a different result...

Joshua Kennon

July 29, 2014

Replying to Mirmer

There are two ways to handle reinvested dividends.

1. Pool them in a money market account and reinvest them regularly with additional cash deposits, sometimes paired with a dollar cost averaging plan

2. Use an individual-DRIP on a security-specific basis, sometimes paired with a dollar cost averaging plan.

I, personally, use the first method. All dividends come from all sources, tied to a CCDA, and then get reinvested based on what I want to acquire at the time. The Kodak study results on the initial investment would be identical to those shown here. For example, I just recently used dividends from Coca-Cola, Royal Dutch Shell, Wells Fargo, etc., to buy a bigger stake in another blue chip position.

If you opted for the second method, your results would be lower on the Kodak-specific account but still not zero as the spin-off shares would have been significantly higher and still retained their value. Also, when put together in a portfolio of blue chip stocks - the magic number seems to be three companies when analyzing a statistical probability of positive outputs over longer periods of time - the overall compounding rate of the aggregate portfolio still would have put you squarely in the black (which is why I tell people they should never have all of their net worth in a single security. As Benjamin Graham put it, your portfolio is like an insurance company writing policies for car owners. You need to structure your affairs so that the occasional claim (loss) ends up being inconsequential.)

The reason this is possible is because of the mechanics of compounding. A basket of stocks earning average rates of return only ends up slightly less than average if a handful of the firms go bankrupt, provided you are holding for a 25-year time period.

Jessica Knappe

May 1, 2015

I was looking up historical dow todand other businessesy, which is what brings me to this post. Its good to blog and discuss, if just to write down thoughts. Kodak sort of disappeared for a while. Then the banking crisis, looking at citi group makes me feel ill. Im going to have to agree with indexing, but the current yeilds are killing me. I have a valuation model to share, ebitda5.

Ebitda x 5, for a recent sale of aprivate industrial firm in NH. In 2012 as a starting point.rule of thumb

Interestingly enough, valuations of private equity are similar, in time, with their respective sector indexes. The indexes, as the average, private firms are or seem to be riskier but cheaper.

Similar p/sales. Similar pe. Simikar marketcap to revenue. Similar by many measures. I suppose if a person wanted to value a small public business, its relevant sector index could be a good starting point. Comparing e (8.5 + 2g) 4.4/by. Very very similar.

So I want to share, value of reits or real estate can be determined similar. I used to be realtor and machinist. Im finding reit index is also inline with private sphere.other than ffo, try

(Annual Rent local sq foot ave. - tax - maintenance)=e. Growth rate is gdp, 2-3%

It should line up with residental sales.

Im finding private valuations to be so much like indexes, seems the indexes could be safer. But you just cant raid the cash register or pay yourself as ceo. But the numbers just line right up.

Try sp 500 intrinsic value based on a 2 or 3 percent growth. Beta 1. Then comparepremium