Both the World and Capital Markets Feel Strangely Similar to 2006

For the past two or three weeks, I’ve found myself experiencing a strong sense of déjà vu. So many aspects of the world, and capital markets, today feel similar to the period following when Aaron and I graduated college; the time during which we built our early economic foundation. To give you just a brief sense of what I mean, consider we finished school in 2005. Thus, 2006 was our first full-year post-bachelor degree as independent, educated adults.

Housing is Almost the Same – Absolutely and Relatively – In Both Pricing and Financing Costs

- The median price of buying a home in January 2006 was $247,700, which on an inflation-adjusted basis is equivalent to $408,193 today. That puts it in the same ballpark as the median home price of around $405,300 as of the most recently available figures from 12/31/2025 as per the Federal Reserve Bank of St. Louis (with inflation adjustments performed separate via the Bureau of Labor Statistics).

- 30-year fixed-rate mortgages on January 5th, 2006 were 6.21% versus the most recent data from the day-before-yesterday of 6.38% as per the same source.

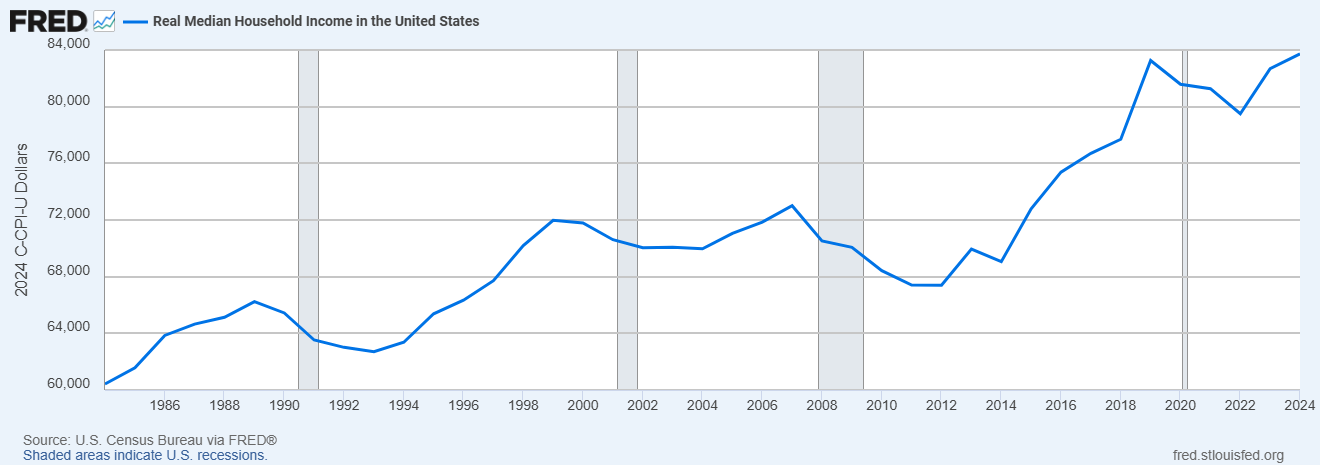

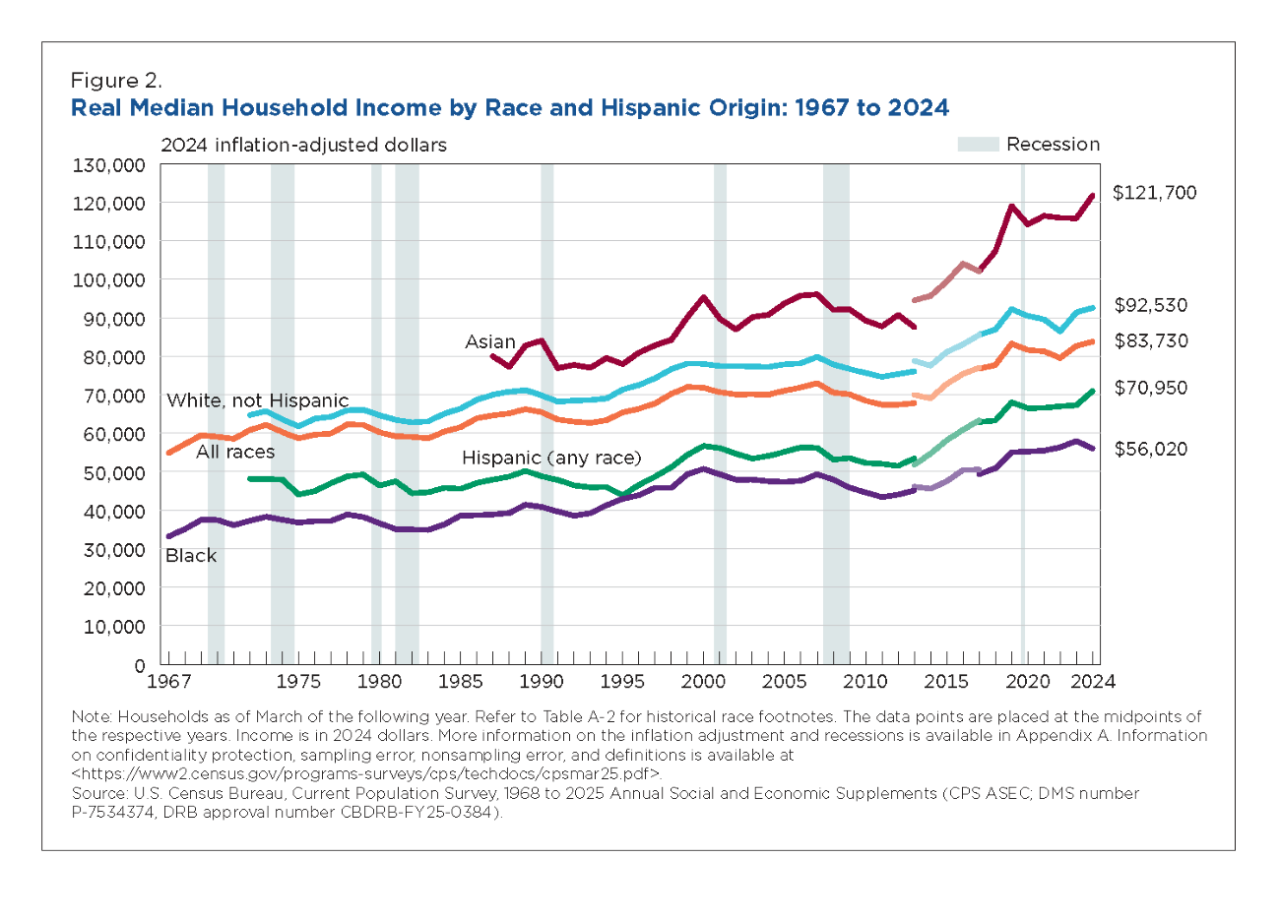

- Real median household income (that is, adjusted for inflation / cost of living changes) in 2006 ended at $71,850 versus $83,730 in 2024 (which is a year lagging due to reporting timing differences; the actual figure is higher than even that today), once again as per what is likely the best data source in the world.

We Were At War in the Middle East Causing Energy Prices to Spike

- The U.S. was boots deep in its ground war in Iraq and Afghanistan. Israel launched an offensive into the Gaza strip after Hezbollah fighters attacked, captured, and killed Israeli soldiers. Gasoline began January 2006 at $2.304 per gallon, which is $3.86 today. By July, it had spiked to $2.948 per gallon, which is equivalent to $4.73 today. You can see the data at the U.S. Energy Information Administration for yourself.

Employment Markets Were Tight

- In 2006, unemployment ran about 4.6%, whereas today it is doing better at about 4.0% to 4.2%.

Markets Had Some Strange Similarities

- There turned out to be some really attractive opportunities as the uncertainty unfolded in more conservative businesses.

- Silver and gold had spiked dramatically, going on a run that ultimately would continue for several years before then experiencing a lost decade in inflation-adjusted terms. (Interestingly, gold only recently exceeded its former inflation adjusted peak from back in the early 1980s. It had been great for trading, but horrific for those who just accumulated and held it rather than owning wonderful businesses. The opportunity cost was staggering.)

There Are Other Things, Too …

It doesn’t stop there.

There were fears in the public health sphere about declines in vaccination; e.g., hundreds of people contracted polio in India panicking global officials. Meanwhile, experts were terrified of a particularly bad strain of tuberculosis that resisted treatment which had appeared overseas. The technology landscape had some major stories in the news …

Amazon Web Services launched, Google was taking over everything, Facebook opened up to the general public.

Taylor Swift was making a name for herself breaking into the Billboard Top 100, where she still sits today.

The political environment had gone from neo-liberal progressive to more insular and regressive both at the Federal and state levels. The White House faced levels of disapproval that had been almost unthinkable in the past.

Schools in the Western World were moving back to phonics after certain areas had migrated away from it due to ideological capture.

It’s just very, very strange … the generalized sense of anxiety combined with seeing opportunities that get me very excited for the next ten years crossing my desk. Even the fear is so misplaced. The typical person is way too concerned about some of the news headlines while ignoring other things that are much more important. For example, it was a bit astonishing watching software companies start a sell-off recently after a single memo ran a thought experiment asking what would happen if A.I. (which really means large language models and is anything but) destroyed a good portion of white collar work within the next 24 months. The problem? No one placing trades, or writing in the media, seemed to stop for a moment to realize that even if people were able and willing to adapt to it so quickly, and if it were reliable without much supervision (it’s not – I cannot emphasize how terrible it is at complex financial analysis), there are half-a-dozen separate bottlenecks that make it physically impossible for it to happen on that timescale. (I mean it … physically impossible, as in the tangible real world. Hard drive sales are basically booked for the next year or two. RAM is experiencing substantial shortages. GPUs are impossible to come by. The energy grid cannot cope with that level of scale-up so rapidly. It. Could. Not. Happen. Even if we threw trillions more dollars at it as a society, it falls into that category that Warren Buffett once noted: “You cannot have a baby in one month by getting nine women pregnant.” Some things take time. The people living in this world have drunk the proverbial Kool-Aid.)

Fortunately, at work, I had been letting cash build up for a few quarters in most accounts. It’s time to start deploying money in a notable way. My staff has nearly every portfolio at the firm lined up in rotation for us to rapidly go through and begin rebalancing in the near future. I feel, strongly, that this is easily one of the top two or three moments in my career when an investor can buy an attractive amount of private income at conservative valuations with a good probability of future increases outpacing inflation. There are so many intelligent things to do right now even assuming, as I think one must, higher energy inputs acting as a drag for the next 36 to 60 months as the infrastructure will take time to rebuild causing artificially tight supply to persist beyond the end of conflict.

Even outside capital markets, where I spend my day-to-day … there are so many areas that are scalable; that don’t have barriers to entry they did when I was in my early twenties in 2006. The tools that a person can access today versus what was possible in 2006? My goodness. It’s so much easier now. The things I did in 2005, 2006, 2007 set me up for today. They built a foundation. There are so many people who will come out of this period and look back on it a decade or two from now as being the key to everything they’ve accomplished.

It’s strange seeing cycles repeat themselves. Ben Graham, directly and indirectly, used to write about the importance of assuming what has happened before will likely happen, again …

Reader Comments (30)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Clint

April 3, 2025

Josh,

This is a little off topic, but I remember a couple of old writings of yours concerning black swan events in the about[dot]com days, and I was wording if those were still available?

Reading through JP Morgan analyst views on tariff levels today, "the tariff rate represents the largest tariff increase in over 100 years, making it difficult to analyze the impact, as there is simply no precedent for a modern economy to increase borad trade barriers of this magnitude." And "we view the full implementation of these policies as a substantial macro economic shock not currently incorporated into our forecasts."

While their language stops short of using the term Black Swan, they do use pretty well the verbatim definition of a black swan.

James

May 25, 2025

Very inspiring. From the sounds of it, you are doing a great job.

At the same time, I don't think this can happen without a lot of paid childcare in the background that you have not alluded to. Children are boundary-testing machines. They are not rational beings that can be held by contracts, deals, and agreements. They want to be around their parents and will intrude into offices where Daddy is reading the Berkshire Hathaway annual report unless they are restrained somehow. They fight, have accidents and cry, get frustrated and need attention. Unless someone else is around to buffer these behaviors, the parents inevitably will have to intervene.

We have three boys. No nannies or grandparents. For our own desire for sleep on Saturday or Sunday mornings, we allowed screen use. I don't like it, but it allows me to actually have some time to myself to enjoy the intellectual things I enjoyed before I had kids.

M Huang

June 1, 2025

I was wondering if you could elaborate more on your email system - how do you manage these 70-80 aliases? Could you give examples on how you organize and categorize and decide when a new email needs to be created? I have rental properties, do you do one for all utilities of all or per property? For family items, health related to one email for the entire family or per person? School? I have 3 children and it is a constant tug of being distracted with new things and fighting to focus on things that need to get done at the same time. And there is time "wasted" just getting to information and deciding to take action. I would like to know more how you manage your household with professional and personal administration.

Starks

September 27, 2025

Thanks for these posts! As infrequent as they are these days, I find myself still coming back to them for wisdom, especially in the comments. My son is almost 3, and I'll be having a daughter later this fall. I have been fortunate enough to work from home for the past 5 years and my wife has since left her job to be a full time stay-at-home mom, so we both get to spend an enormous amount of time with our son, which I wouldn't trade for anything. I agree the first 2 years were stressful, but he is now entering the very fun phase of constant questions, shadowing everything I do, and just being so pleasant and inquisitive in general. I am constantly humbled when seeing the world again through his eyes. Screentime is extremely limited, as we don't want him getting hooked on short-form content either. Thank you for sharing your thoughts and parenting strategies, as they help me to recalibrate my own thoughts and emotions during various scenarios. Keep on truckin' my friend 🙂

JB

March 28, 2026

Welcome back! Hope you and Aaron and the kiddos are doing well.

Joshua Kennon

March 29, 2026

Replying to JB

Thanks! We are and I hope you are doing well, too! I have a bit of time this morning as I work on some IT backend stuff I need to oversee myself so maybe I'll start working on an update about what we've been up to in the meantime.

Viresh Amin

March 29, 2026

Replying to Joshua Kennon

Any chance on commenting on Kennon-Green's fund performance?

Joshua Kennon

March 29, 2026

Replying to Viresh Amin

It's good to see you on the blog, again!

For regulatory reasons, I don't discuss the firm on my personal blog. There are a tremendous amount of SEC regulations around the presentation and calculation of figures to the point that it cannot be treated as an aside or approximate comment and I'm not going near it with a ten-foot pole considering our conservatism and insistence upon following the rules.

That said, to clarify because I don't want there to be any misconceptions: There is no such thing as a fund. We have never had a fund. Maybe, someday, I'll launch one in which case it would be easy to discuss because there would be an official release filed regulatory on a consolidated pool of assets.

Rather, the firm is structured a fiduciary for individuals and families in the high net worth space. That means every portfolio is completely unique, governed by its own fiduciary contract, and often has very specific goals.

For example, we may buy or sell assets because the client's CPAs and/or estate planning attorneys have other objectives that are trying to be accomplished in tandem; e.g., selling things that have appreciated despite wanting to buy more because an outside loss for the client can shelter that income, or selling things during a market correction we would rather be (and are) buying for other clients. We may have someone show up with an enormously concentrated position in a single tech stock they received and want us to develop a non-tech private income portfolio consisting of stocks, U.S. Treasurys, and corporate bonds with distributions taken (in a few cases, daily) monthly or quarterly, specifically noting they don't care it if overperforms or underperforms the market as the job of that money is to create regular payouts in the event they lose their employment or decide to retire; they don't want to have the entirety of their fortune tied to, say, Silicon Valley or another, single industry. We have highly successful investors on their own who want a diversification of risk analysis and to have a relationship in case, heaven forbid, they pass away they want their spouse and/or children to already know us so the entirety of their estate transfers to our management. There may be assets sold, transferred, divided, or gifted due to marriage or divorce. People have us rotate portfolio positions to pay for home renovations or boats; selling or buying businesses; mineral rights, oil fields, residential, commercial, and/or industrial real estate acquisition and/or development ... I've often joked - with some seriousness - that some folks simply found a way to put me on retainer; e.g., they kicked in several million dollars to an account but never want to discuss it, instead calling periodically to talk to me for hours and get my advice on their personal or business lives, interesting problems, opportunities, etc. We're like a private chef's table restaurant where every diner gets what they want, provided it is all French food (i.e., value investing).

Again, though, I have to draw a hard line about talking about our operations. I want a clear, bright division regulatorily between my personal life and the firm. I am only responding to this question because 1.) you have been a member of the community for a long time, 2.) I don't want there to be any misunderstanding at all about what I do or how we operate. If you want more specifics on the day-to-day operations, I can only refer you to the Regulatory Documents and Disclosures page, specifically the "Form ADV Part 2A and 2B Brochure" dated March 18th, 2026. I just filed it recently. There are quite a few new risks about the world / economy / political environment I updated this year in Item 8 that I think are interesting.

Viresh Amin

March 29, 2026

Replying to Joshua Kennon

I figured this, but its always good to get a full response on your thoughts. Thank you for responding.

Gilvus

March 28, 2026

Confirmed: Great Recession 2.0 commencing in 2028. Whispered from the undead lips of Ben Graham's ghost.

Universa's Spitznagel has been predicting the "worst crash since 1929" for several years now. He seems supremely confident about the event occurring while also being agnostic about the timing of the event. Wouldn't it be poetic justice if it happened on October 29, 2029?

10/29/2029 is a Monday. It's a strong contender for challenging 10/9/1987 for the title of "Black Monday."

Joshua Kennon

March 29, 2026

Replying to Gilvus

Strangely enough (I keep using that word - "strange" - but it fits so many situations right now), while there are paths to a severe recession (an energy shock being the speed bump that throws the AI bubble off the rails and sets off domino effects), things are in much better shape than 2006 in so many areas.

A few years ago when I wrote Thoughts on the United States Returning to a Normalized Interest Rate Environment, the Housing Market, and Related Topics , I dove into some of the housing equity figures and they are wild. There is so much equity reserve now sitting in housing its wild. Of course, there was in 2006, too, but the difference is the mortgages today are of vastly superior quality; no part-time workers with three houses using adjustable rate ARMs that lack the protects that came post-Great Recession. Even then, though, if you look and the Households; Owners' Equity in Real Estate, Level report from the Federal Reserve Bank of St. Louis , it visually resembles twenty years ago.

https://uploads.disquscdn.com/images/285ae51a9c83ac8de5eea45cf114e9cf8da21abdfb8090d2e28c5317ef6d3b26.png

It's also interesting to me that a good deal of people are acting like this is the worst economic time in history when it's anything but ... the Great Recession, as pointed out in the massive economic tome, A Century of Wealth in America by Edward N. Wolff, was so extreme in what it did to quoted household net worth figures that by 2013, "median household wealth was back to where it had been in 1969!" He was talking about real inflation-adjusted median figures, which required a bit of work reconstructing several data series, but it was true; 45 years of wealth accumulation wiped out ... and that was a bit post-recovery or early recovery. At one point, in 2010, approximate median household net worth in real (2013) dollars had fallen to around, I think, $77,000 before climbing back to the $80,000 to $85,000 range. And then, of course, things came roaring back. The compound annual growth rate is really shocking for such a figure to get us to where we are now.

Folks have no idea. I have one draft I started working on a few months ago I should dust off ... we're now at the point where 1 out of every 5.5 households in the United States has a net worth (assets minus liabilities) of more than $1 million. In the 65 to 74 year old range, it's 1 out of every 2.7 households, or 37 out of every 100. The numbers are insane.

Seriously, though ... the energy tightness is so far more extreme and relevant in framing economic projections. That's especially true with data centers being so hungry for power; it's not going to be easy politically for AI companies to get the capacity they need. There are already a couple places working on citizen-backed constitutional amendments to require data center construction projects to meet certain standards, such as no subsidization of energy prices. There is a non-zero chance they pass. (On that note, it's a bit wild to me that so many people don't realize that several of the data center projects are really just the future infrastructure for a mass surveillance state on steroids. It's not an accident there has been a push for age verification laws, including for operating systems, at state levels. It's going to be ugly for awhile without restrictions. There was a grandmother in Tennessee, Angela Lipps, who spent months in jail because North Dakota started using facial recognition AI and it identified her as the suspect in a bank fraud case despite the fact she had never been to North Dakota and could prove she was somewhere else in Tennessee when the crime was committed. The way places are implementing these very, very imperfect tools is unhinged.)

* Corrected to North Dakota on 03/30/2026 at 10:24 a.m. Eastern

Devin Rippe

March 30, 2026

Replying to Joshua Kennon

It is great to see you posting again and hearing that things are going great for your family! I’m always thrilled to read your insights and would love an update on your house project(s). However, I think it was North Dakota using the AI to arrest that lady. We here in South Dakota are not that advanced yet. ;). We are still trying to work past the “Meth, we’re on it” Noem ads. Anyways, I look forward to hopefully a bunch more posts this year.

Joshua Kennon

March 30, 2026

Replying to Devin Rippe

You're absolutely right - thanks for bringing that to my attention! I fixed it and noted the correction. (Probably a professional bias as I think about South Dakota quite a bit given its central role as one of the nation's premier trust domiciles, whereas North Dakota barely crosses my radar.)

The house projects ... I have so much to update. There should be some major renovation later this year so maybe I can get something out about it after it is done.

Infinite Ben

March 28, 2026

Great to see you back, Joshua!

Continuing with this analogy, does this imply something nasty around the corner? There certainly is a dancing around the edge of the volcano vibe in the world right now.

Joshua Kennon

March 29, 2026

Replying to Infinite Ben

A few seconds ago, I sent a reply to a comment Gilvus made that gave some of my thoughts on it so check that out if you can. Expanding upon it, I think it's wise to always assume a recession could happen at any moment regardless. They certainly were more frequent when I was younger, and in American history. Most are not like the Great Recession; nowhere close. They were speed bumps as the economy recovered and adjusted. To be fair, we have better signals now; businesses can see in real-time which products are selling, cash projections, you name it. This could mean that compared to the past, when the gears start to slow they can spin up, again, much faster provided we don't go into a liquidation that becomes self-fulfilling. In that case, we'd see fewer recessions but the ones that did happen could be more severe.

Similarly, seeing what September 11th did to the world in a matter of hours, I also think it's wise to run your life in a way that you'd be economically fine, all things considered, if you woke up in, say, Kansas City or Houston or Denver or Jacksonville, for example, and there had been another major attack on the scale of those that happened in 2001. This is probably a by-product of my particular age cohort; coming home from elementary school and seeing the Oklahoma City building bombed out and so many people murdered; watching the towers fall in college; listening to the older generations talk about Pearl Harbor and what it was like waking up and suddenly all the male family members being shipped off to war, some dying. There was a general sense of, "There but for the grace of God go I" in all things and at all times. My late grandma Kathryn passed away in her 90s. Right before Aaron and I left Missouri for California to have kids, we went down to spend time with her, staying overnight. You'd open doors to guest rooms and they'd be filled with food stores in case another Great Depression or war rationing happened. Shelves of sugar, canned goods, coffee ... you name it.

In the broader economic picture, there is a lot of "AI washing" going on right now, where companies that had overexpanded payroll or who want to perform layoffs to optimize cost structures are laying it on the technology. Sure, some corporate giants were bloated and had folks earning salaries for work that could be rote automated, but that's not really what happened. It sounds much better to sell a layoff as a mass productivity boost than to say, "Hey ... the cost structure is getting to be a problem and we over-hired coming out of the pandemic." In that sense, a lot of tech workers are acting like this is somehow an unprecedented change brought on by a new technology; as if the IT field was somehow immune from the forces that every other career and profession faced. This is the same sort of pain that was felt in the post dot-com bust era ... the 2001, 2002, 2003 period.

But no ... the biggest risks I see right now are always, 1.) a nuclear device, which cannot be diversified away. 2.) people mass adopting AI and blowing a hole in decades of security best-practices, causing potentially catastrophic failures or vulnerabilities. In some cases, these may be across the whole system, in others they may be contained to a single enterprise (e.g. Clorox got very cheap as a result of having its business temporarily destroyed by one of the worst cyberattacks in corporate history a few years ago). 3.) There is a huge migration of wealth to no-tax and low-tax income states right now that is reshaping power and politics in the United States. This country will not look the same in 20 years as a result, yet New York, New Jersey, California, Washington, Massachusetts, Minnesota, etc. are all acting like they can do what they want with no consequences. It's not going to end well. The latest IRS data for the 2022-2023 year came out in the last couple of days and the trend is continuing. 4.) There is some really terrifying data coming out of a 7-year or so cohort in the education system as a particular micro-generation of folks grew up around the time of school closures in the pandemic, the widespread adoption of IT in classrooms, the abandonment of phonics and written handwriting. As a group, there is nothing like it since we started keeping historical records on educational advancement in the mid-1800s. They are the first generation in history to do worse on every measure of cognitive performance despite the fact they have more schooling than the past, which usually was a directly-linked relationship. They can barely read. Their math skills are horrendous. They can't type or navigate computer file structures since they existed in a world of Chromebooks. The kids younger than them will be fine as things have been course-corrected to some degree, often by state legislation (Mississippi is doing phenomenally in this area). The generations older than them will be fine. I don't think there is a way out for that group, which could cause a lot of self-destructive political action with everyone suffering collateral damage. Of course, there will be superstars in that micro-generation but they will be even more notable for being the exception.

But, generally? Life in 2026 is, with few exceptions, so much better than life in 2006. Sure, some people might prefer the latter if they had family members who hadn't passed away, yet, or they were in better health, but I'm talking about the idea if you were a reasonable intelligent adult, had a modicum of self-discipline, and were curious about the world ... there are so many more opportunities, so much more access ... just to build on the main topic, if a genie snapped his fingers and took everyone back to the 2006 median household net worth figures, folks would feel like the world had ended. It is exceedingly easy to ignore the progress that has been made in the past few decades. (The starry-eyed longing for the 1950s and 1960s is even crazier to me ... absolutely delusional. There is, of course, the obvious civil rights horrors. Going beyond that ... do you know how much of this country did not have indoor plumbing when, say, Warren Buffett or Charlie Munger were in their early twenties!? It was not a small percentage.)

Red OnRed

March 29, 2026

welcome back 🙂 it's been a while, been reading you since 2015. I have since early retired from full-time work in big tech, in part thanks to your advice from reading your blog.

Joshua Kennon

March 29, 2026

Replying to Red OnRed

Congratulations on your success!!! Hearing about it made my day!

Joe Pierson

March 30, 2026

Nice to hear from you! I've been wondering how you deal with the pressures of managing client's life savings. I guess confidence in your abilities is key. You probably have some interesting stories.

The brutal correction of the boring Blue Chip companies you talked about a few years ago seems to have no end, much worse than 2008, maybe they'll all get bought out idk. General Mills at 5 then 10 now 15-year lows. Mostly due to single digit P/E compression. Brown Forman, McCormick buyout talks is wild, I doubt the Forman family will go for it but they may be frustrated with the stock performance and throw in the towel.

Anyway I know you can't talk about any of that, the "AI" seems magical for the first 5 or 10 prompts doesn't it? But then it goes downhill after that. AI seems to know everything but can't learn anything after the model has been developed. It's still a very useful tool though. I use AI like a super Excel/Word combo. Import a document, graph out charts, summarize, correct grammar etc.

John Carmack's new company is dedicated to researching a learning AGI, he thinks in 5 years we'll have something equivalent to a child. I'm not sure how you verify that. Interesting times.

stonkhunter

March 30, 2026

Thank you very much for the update Joshua,

Do you think Abu Dhabi listed equities such as Emaar offer once in a generation opportunities at current prices ?

Many Thanks )

Felipe

March 31, 2026

Joshua, it’s been far too long! Very happy to get an update from you and to hear that everything is well with you and the family. Always nice to catch a glimpse of your opinions on the world.

Working in IT, I must confess the past few months have been quite strange. We are building systems faster than ever, but at the same time, I have the same fears that you mention when it comes to security, quality and scalability of “vibe coded” systems. Quality control can quickly become a nightmare, and junior developers miss out on very important experience that you only get from coding yourself.

At the same time the opportunities that are arising are really exciting and I am having the most fun working that I’ve had in years. I am truly divided on everything that’s going on.

When it comes to financial analysis I have been testing different approaches the past year or so, and using AI as a tool to help me organize my thoughts and build systems that help me analyze companies have been quite an interesting learning experience, but on this point I feel like I have very little to offer someone as knowledgeable as yourself.

Please keep posting, it is always a joy to catch up. I’ve learned so much from you.

Dividends are Coming

April 5, 2026

Replying to Felipe

Seeing how fast AI is evolving has me a bit worried about the future, too, and what the implications are for the labor market and society as a whole. I'm in IT myself, and the last couple of months have been wild. Last year, we were still mainly using chatbots and stuff like auto-completion, but once you start using agents, everything really starts clicking together. Suddenly, you have LLM-powered systems capable of longer-running tasks.

These days, I often feed ideas to the LLM, and then it just builds the whole thing much faster than I ever could. After some iterations, I'm often able to achieve higher code quality and test coverage than I would have if I'd done the whole thing myself two years ago -- and much quicker too. It's wild. Yet, I'm also worried about quality and slop, as I know not all developers have the same values as me. Some people just want to complete tickets as quickly as possible and don't care if it's slop. In the wrong hands, these tools can and will wreak havoc on enterprise code bases over time.

At the firm I'm working for, most developers are still taking baby steps with agentic AI, but there's already a big push coming from the top to mandate AI use to speed up development. Given the focus on cost-cutting, I would not be surprised if we see mass layoffs in the near future. It's still a very nascent market. AI models are getting better, tools to use LLMs are getting better, and developers are reskilling. Writing code is becoming less of a bottleneck, but getting everything reviewed, QA, and getting it tested is becoming problematic.

Honestly, I have no clue how this is going to ripple through the economy. Ten years ago, I thought I would be comfortable if I just saved up every month in dividend stocks until I hit a financial independence-like level of dividend income. Now I'm not so certain about that future anymore; to me, this feels like a big inflection point.

Dheeraj

April 7, 2026

Joshua Kennon. He has risen!

Walidad Ali

May 9, 2026

Joshua, I've been a silent reader of this blog for as long as I can remember. I think you are underestimating AI. If you believe it cannot produce complex financial analysis, I would love to prove you otherwise.

Nicholas Archer

May 14, 2026

Beautiful bird at the top of the page. ;0)

Joshua Kennon

July 12, 2026

Replying to Nicholas Archer

It's a violet backed starling, one of my favorite birds in the world. It's found in parts of Africa including Kenya. They are just incredible looking - if they could exist in a Midwestern climate, I'd re-landscape my entire house to attract them! https://uploads.disquscdn.com/images/d25d88072de9247d45ddfd87af996297f271c84db5923ac65af6450fdac2e6e3.jpg https://uploads.disquscdn.com/images/3dd88b6a8411d3a4c511f928af75af0991e1429d7441351d95abee28dc247caf.jpg https://uploads.disquscdn.com/images/80d9f1e938eb0ce1476faab4a863a8c9a429d84f73f736eeb0012b91c409dcc3.jpg

Seb

May 27, 2026

I remember eargerly waiting for your articles in Investopedia yeeeears ago when I was a bachelor student in finance! Miss you so much!

Macho Man, Randy Savage

June 3, 2026

It's a bit late, but happy belated Nestle dividend date!!!

I miss your blog updates, but I appreciate all of your advice through the years be it finance, or appliances! I wish the best to you and your family.

Usually posted as engineer7006.

Joshua Kennon

July 12, 2026

Replying to Macho Man, Randy Savage

Likewise! It's funny because over the years, I've ended up with Nestle in a bunch of different places including the [NSRGY] ADRs, the [NSRGF] held as a foreign security in a domestic custody account, and the actual [NESN] on the Swiss exchange that Nestle dividend day has become a rolling event for me with cash coming in at different times. I have a really interesting story / issue I've been dealing with in the financial system related to Swiss dividends for a few years now. I should make a post about that sometime ...

J. Dias

July 4, 2026

I know this is a personal blog but I'd really like to know more about the your investment firm. I.e. whether I can and should invest with you. I've read this blog since the beginning and now with a sizable portfolio 100% in the S&P 500 I'd like to know more about the opportunities you are seeing right now.

Joshua Kennon

July 11, 2026

Replying to J. Dias

It's good to see you! Your comment made me do a quick search because I was curious and your first post was 15 or so years ago! That absolutely made my night!!! I can't believe how much time, and life, has gone by.

Re: Your question. I'm happy to talk to you about it. As this is my personal blog, I can't respond here, I can only communicate about firm-related things or answer those types of questions through one of our approved "regulatory channels" (that way regulators can see email exchanges, etc.) Either way, it'd be good to actually talk to you since you've been around the community for so long.

I'm 99% certain I have your direct contact info from some information I can see in the admin panel from a past comment so I'll have an email sent to you from the Client Services Department at Kennon-Green & Co. Be on the lookout shortly after I respond here to a message from an email address ending in the kennongreen.com domain. If for any reason you don't see it, let me know. I look forward to it!