Economic Reality Isn’t Always Reflected on Your Account Statements

There is an account I handle as a favor for someone I know. This account has a very unique mandate. It holds a handful of stocks, has practically zero turnover, and once a new position is acquired, the dividends must be automatically reinvested into that business, cost-free, until disposition. The entire portfolio is held within a Roth IRA and this person is still more than 40 years away from retirement. Even if he or she never contributes another penny, the account balance at present, with average rates of return, will be worth several million dollars by the time they reach senior citizen age and are ready to begin making withdrawals.

The expense ratio in most years is 0.00%. After the initial positions were established quite awhile ago using a lump sum that was transferred into the account, annual costs are non-existent as I refuse to charge them a fee or any sort of management contract. It is passive investing of the highest order. They had me build them a ghost ship, in effect, that would run itself. The holdings are well-balanced across the economy, global in scale, and would survive another Great Depression even if several of the firms on the roster were wiped out entirely.

Watching the ghost ship sail over time, with me periodically deciding which positions get added, has proven interesting. The thing that strikes me is just how non-intentionally deceptive brokerage house accounting records are. They provide a completely distorted view of what is actually happening with one’s portfolio, overstating the importance of capital gains.

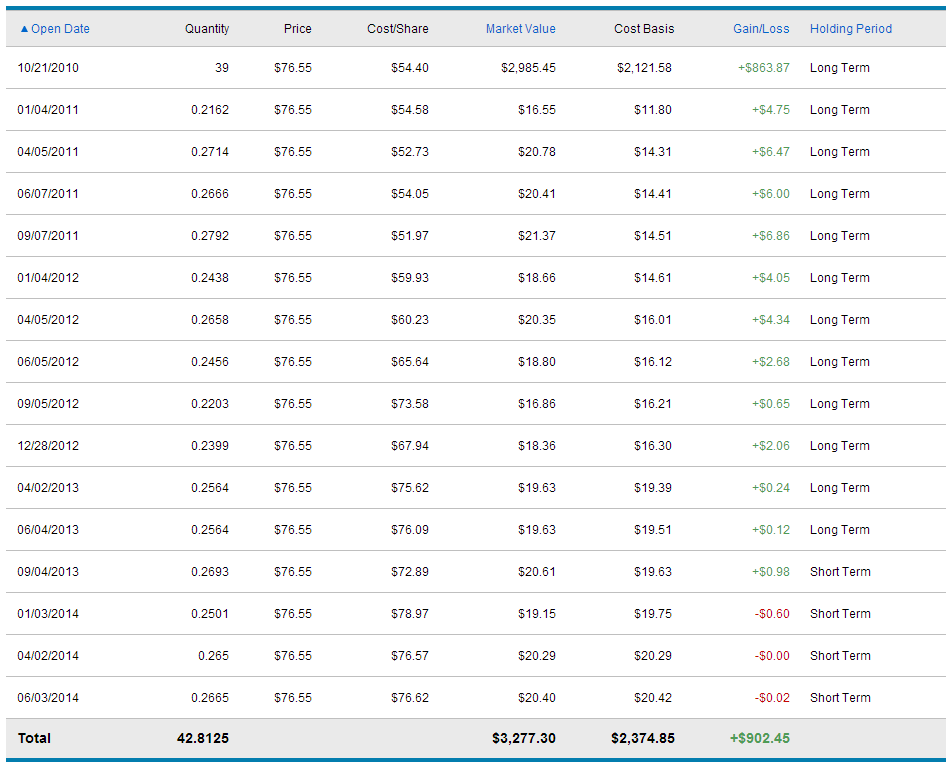

To demonstrate, let’s look at a relatively small position in this account. On October 21, 2010, I used $2,121.58 of this person’s savings to purchase 39 shares of Wal-Mart Stores, Inc. Since that day, Wal-Mart has made 15 cash dividend deposits into their account, which the broker reinvested for free. The combination of additional shares and the board of directors hiking the dividend rates has resulted in the quarterly dividend deposit growing from $11.80 to $20.42 over the 3 years and 8 months that followed.

As as result of dividend hikes and reinvested dividends, you can see that every single dividend received has been larger than the last one. The first was for $11.80, the next for $14.31, the next for $14.41, etc., until, a little more than 3 1/2 years later, the quarterly payout has nearly doubled to $20.42. That’s what you want – a stream of checks that grows on its own without a lot of effort from you.

In that short amount of time, the share count has increased 3.8125 shares, or 9.78%. Meanwhile, Wal-Mart has been buying back a lot of stock so each share outstanding represents more ownership than it did previously, which was partially responsible for the stock appreciating to $76.55.

Given how the brokerage firm calculates return for the investor, this makes it appear as if the profit is $902.45, or 38.00%. But that is not the whole story. That is a rough estimation of the tax basis for capital gains (which, in this case, isn’t even useful since it’s in a Roth IRA).

The real situation is that the account holder is $1,155.72, or 54.33%, richer than he or she was thanks to Wal-Mart. The initial outlay of $2,121.58 turned into $3,277.30 from the following sources:

- $863.87 came from capital gains on the original investment of 39 shares

- $241.51 came from dividends on the original investment of 39 shares

- $11.76 came from dividends on reinvested dividends

- $38.58 came from capital gains on reinvested dividends

While the differential may not seem like much in absolute dollars given the small amount of money in this illustration, in terms of percentage, it is breathtaking. Imagine if we were talking about a $100,000 investment or a $1,000,000 investment. Even worse, this is only a few years into an ownership position. By the time you saw 20 or 30 years, the gulf would be so large that it would completely distort the real world implications of holding the stake.

Why does this happen? The brokers aren’t being dishonest. It has to do with the tax code. The brokerage firm shows dividends as income in the period received so those who hold their shares in plain vanilla accounts can pay their bill to the IRS. From that moment, the dividends are treated no differently than any other source of freshly deposited money for accounting purposes. I know of no brokerage house that accurately tracks total return over time on the month-to-month statements, though a few have tried to move in that direction; e.g., Charles Schwab provides a quarterly portfolio review that gets you there in a round-about way.

Thus, you have a bizarre disconnect between economic reality and accounting figures shown on the brokerage statement. The economic reality is that an owner of Wal-Mart grew his or her money at 54.33%. The accounting figures on the statement make it appear to be only 38.00%. Personally, I have a sneaking suspicion this is how you get the mental disconnect between actual investment experience and perceived investment experience. It’s the reason people don’t understand you could have quadrupled your money with a company like Eastman Kodak despite the stock getting wiped out in bankruptcy.

To fix this, you have to keep records of your own and not rely on the statement in isolation, tracking every dividend check and allocation decision either in a spreadsheet or accounting software. Personally, given my fluency with numbers, I opt to run my household level accounts on a modified form of GAAP using QuickBooks Pro. Every dividend paying company is entered and deposits tracked not only by the issuing company but by sector and industry on the income statement, looking something like this:

This presentation allows me to watch both the trends in cash generation as well as historical sources of dividend income that funded the balance sheet growth. Others of you would be wise to build something like I did for the souvenir shares of Walt Disney I pick up from time to time, watching the dividends received on each lot acquired. (Today is the 59th birthday of Disneyland, by the way.)

I think the brokerage industry needs to find a way to fix this. A lot of people, for better or worse, treat their account statement as their accounting records despite the flaws. For retirees, it can get even more deranged, though still perfectly reasonable once you understand why it is happening. Case in point: While it is nothing special to any of you who are familiar with finance, new investors can often be surprised that in an environment where interest rates have fallen and you are buying a secondary issue bond, you’re going to often pay more than par value so the yield-to-maturity is comparable with new issues at the time. This creates a situation where you are collecting far more interest income than you otherwise should be as the coupon is the same, but you have a built-in loss on the bond so it works out to the appropriate result in the end. You could have an account statement, in certain circumstances, showing a ton of capital losses while you were actually making a positive return. To the non-financially sophisticated, the sea of red can cause panic.

The whole situation could be avoided if I could take over the brokers for a day, or maybe the SEC, and somehow standardize account reporting requirements. This isn’t a hard thing to fix.

Update: I restored this post on 05/05/2019 as part of a project meant to bring back some of the private archives that I feel have educational, academic, and/or entertainment value. However, on May 16, 2019 as part of that same project, I restored another post called An Example of Real World Value Investing Through the Lens of Dr. Pepper Snapple Group, to which I wrote an update detailing the subsequent experience of shareholders. It is a perfect example of why it is a mistake to attempt to use cost basis accounting from a brokerage statement to track investment performance. The summary version is that a single share of stock bought for $47.46 turned into $142.63 of wealth in a relatively short period of time. This was a fantastic return. Strangely, because of how the accounting was structured for a merger with Keurig, the single-serve coffee giant, the stockholder’s brokerage statement would now show an unrealized loss of 38.7%. It seems counter-intuitive that a person could have generated large gains while showing large losses yet that is precisely what happened. I cannot emphasize this point enough. The unrealized gains and losses on your statement are only part of the story and often can be misleading. You must measure actual economic results in the form of total return.

Reader Comments (16)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Tyler Phillips

July 18, 2014

I didn't know it was possible to buy partial shares. My broker will only buy whole shares.

In the case of a higher priced share like those of McDonald's, I would need at least 123 shares at the moment so that one dividend payment can buy one share. The rest of the cash simply gets deposited in my account if there isn't enough to buy another share.

Joshua

July 18, 2014

Replying to Tyler Phillips

That's odd. I've never heard of a broker that won't do this for you. Who's your broker?

Lord Squidworth

July 18, 2014

Replying to Joshua

Some brokers don't do DRIP, some do.

Of the brokers that do, some buy partial shares, others don't.

Joshua

July 18, 2014

Replying to Lord Squidworth

I'll have to make sure that I ask about this if I ever work with a different broker. Thanks.

Tyler Phillips

July 18, 2014

Replying to Joshua

Questrade. I'm in Canada, so it's a Canadian broker. They offer DRIP, but only if the amount of a dividend payment buys full shares. The remainder is deposited as cash. Maybe it's a Canadian thing.

Canadian Dripper

July 18, 2014

Replying to Tyler Phillips

I believe the only Canadian broker that will do a real drip (not synthetic) is "Shareowner" https://www.shareowner.com/index.html

I've never used their services so can't offer an opinion on them.

Of course, the other alternative is to DRIP directly with a company. For almost all Canadian companies, this involves buying a physical share, mailing it to the transfer agent, and then starting up a DRIP. There are many American companies for which you can purchase the first share directly from the transfer agent and start the DRIP - a much easier process.

Look here for more info:

http://www.dripprimer.ca/

http://dripinvesting.org/

peterpatch79

July 19, 2014

Replying to Tyler Phillips

I also use Questrade. No fractional shares, but since I am regularly buying stock I just use the dividends towards my next purchase which doesn't add incremental costs. Questrade is a great discount broker except for the USD currency conversions, the rates are insane (2%)! I would highly recommend that you use a simple technique called "norberts gambit" to exchange your CAD for USD and vice versa. Here is a video showing you how to do it in Questrade: http://www.moneygeek.ca/weblog/2013/10/18/how-exchange-usd-cad-cheaply-using-questrade/. I have done this with Questrade multiple times and it usually takes 3 business days for them to do the conversion and they haven't charged any fee's other than the brokerage fee for buying and selling the ETF.

jss027

July 18, 2014

Thanks for all you insight Joshua....your site is a primary resource for me. This article is timely for me, as I've been managing a few accounts for my family members (also unpaid:-)) and I also actively manage and track "ownership" records for each of them using google docs (that I modeled from one of yours by the way) as a tool I use to teach them to recognize the disparities between broker statements you've mentioned above and the "real" benefit of long-term ownership in great businesses. They're all hooked by the way...eyes opened. Thanks again for your generous teachings, it's my belief that I am progressing towards transitioning the family trees wealth direction permanently (from lower middle class to the 1% ...one day) as we speak...or type. The information is available for those that seek to learn.

jss027

July 18, 2014

Oh yeah...I'm utilizing Merrill Edge's platform where I received 30 free trades per month as a platinum preferred customer. Now that it's set up and designated...the expense ratio will be 0% as I continue to accumulate. The 30 free trades are spread across my accounts (taxable and roth) and the kids UTMA accounts!

David Evans

July 18, 2014

Joshua,

So if you pool your dividends and choose to allocate them to an existing position that is trading in the market at a favorable valuation, do you add the "new pooled dividend capital" to your cost basis for that position in your personal records or, as you seem to indicate in this article, do you treat the pooled dividend capital somehow differently than capital derived from other sources?

Joshua Kennon

July 18, 2014

Replying to David Evans

When a dividend is received, it is ascribed to the payee (allowing all transactions related to a certain company to be analyzed later) and credited to an income statement account based on its sector; e.g., Income > Dividends > Mining & Industrial Metals.

At that point, the cash has made its way onto the balance sheet and can be used for any purpose - spending, building reserves, donating to charity, or funding a new investment. If I were to buy a new investment, it would count toward the cost basis, just like the broker. However, unlike someone relying on the brokerage statement years down the line, I'll still be able to see exactly how much of my portfolio came from those historical dividends because the dividend is going to show up in several places.

First, I have a specially formatted 11"x17" yearly and monthly roster that is memorized as a report, showing all sources of income. When I run it, I can see, over time, exactly how much dividend income has been generated from a certain sector both in absolute amounts and as a percentage of all income sources.

Second, I can run an entity-specific figures. If I wanted to see all transactions related to a company, let's pick a random firm like BHP Billiton, I could generate a series of reports and see all outlays to acquire new shares, all incoming dividends, all ADR fees, all foreign taxes paid, etc. A bit of back-of-the-envelope math would then allow me to calculate the total return from owning BHP as long as I knew the market value of the position at any given time, which would take a few seconds to research.

I also keep a series of spreadsheets external to the accounting software, allowing me to get more detail and write notes to myself. For example, I have one master spreadsheet that has a detailed breakdown of exactly how many shares are parked where - in this IRA, in that LLC, etc. - calculates our cut of the look-through earnings, annual dividends, total return, etc. Given how little activity I generate (it's mostly new purchases as fresh cash comes in), once the setup was done, it didn't take much work to achieve.

David Evans

July 18, 2014

Replying to Joshua Kennon

Thank you for your detailed response. How to account for pooled & reinvested as well as DRIPed dividends has been a bit of a quandary for me since I adapted a spreadsheet for my own and my children's portfolios that I cribbed from an article you posted several years ago. I eventually settled on the method you describe. The spreadsheet has been immensely helpful, by the way. I very much appreciate all of the knowledge that you take time to pass our way. Thanks again,

Dave

innerscorecard

July 18, 2014

I would support a Kickstarter or simply pay you money to buy software (either an app or a cloud service) developed by you that translates brokerage statements to economic reality. I know everyone can do it themselves but as Joel Greenblatt realized when he went from You Can Be a Stock Market Genius to the magic formula to running a fund again, people really just want you to do things for them and will pay good money for it!

Mario

July 19, 2014

Hi Josh,

"Wal-Mart has been buying back a lot of stock so each share outstanding represents more ownership than it did previously, which was partially responsible for the stock appreciating to $76.55."

Am I correct thinking that share repurchases are NPV-zero transactions whenever the shares are fairly priced, leading to no change on share price? Are you implying that Wal-Mart made the repurchases when the stock was undervalued?

Thanks,

Mario

SB

July 21, 2014

Nothing to contribute to this particular discussions but I would like to say that thanks for all the information you provide. I stumbled to your website when I was doing some Google search. I would like to say that yours is probably the best PF blog that I found (or probably a tie with mrmoneymustache). Thanks.

Matthieu Croce

December 10, 2015

This is one of the biggest complaints I have when looking at brokerage statements. It's what led me to creating my own set of books for tracking my investments when I was in college.

I'm setting up an investment club for a group of friends and may point them here to help them understand this very issue.