A Good Business versus a Great Business: A Look at Carnival and McCormick

There was a question that landed in my inbox from a reader named Jeremy. He wrote:

First off even if you don’t reply to this I’m very grateful for the content you provide. It’s nice to see some fresh light and an everyday take on different financial situations. Plus I enjoy your enthusiasm!

I bought carnival cruise lines a few months back for 32 a share. I bought it with the intentions of holding it for years and just wanted to get your take on the company itself.

I normally avoid discussions of individual businesses unless I bring them up out of the blue because a lot of inexperienced people out there are off their rocker when it comes to reasonable expectations or knowing how the equity markets work. If I say Company ABC is overvalued and it goes up another 50%, they’re likely to think, “See? I knew I should have bought it! I never should have listened to that guy!”, not aware that stupidity in valuation can feed on itself. Likewise, if I say, “This is a great opportunity” and the stock collapses further, they are likely to think, “Why did I listen to him? He’s an idiot.”

It wouldn’t matter if I turned out to be correct in the long-run because most folks won’t be around for the long-run. That’s why I often repeat the warning that neither I, nor anyone, has a clue what will happen to stock, bond, or real estate prices in the next year, or even five years. Instead, I think of my task of coming up with a fairly good range of probabilities for what is likely to happen over more extended periods. It’s the nature of the game. All else equal, certain enterprises should be worth much more decades from now than they are today. As for gold prices, interest rates, or the market value of Monet paintings, it’s all a guess.

Still, since Jeremy is not asking about the stock, but about the business, I thought it would be a good opportunity to have an academic discussion highlighting the contrast between a mediocre, but still satisfactory, company and a truly excellent enterprise.

McCormick vs. Carnival: A Case Study In Business Quality

Over long periods of time, a great company is one that can earn high returns on capital while protecting its competitive advantages; a firm where every dollar the owners put to work generates a lot more dollars.

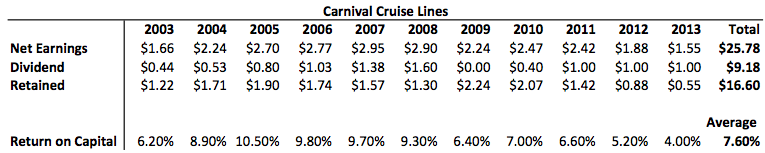

It took some effort, but I found a corporation that matched this description – McCormick & Company, the spice giant that has dominated the North American spice, extract, and seasoning industry for nearly 125 years – that was trading at roughly the same valuation as Carnival, with the same earnings, and the same dividend per share. I used Value Line’s figures, so we’ll examine the 2003-2013 time period since that is the easily accessible information they make available, with the 2013 figures including 4th quarter analyst estimates.

Imagine back in 2003, you bought $100,000 worth of Carnival Corporation when the stock market opened, paying $24.96 per share. That was a base earnings yield of 6.66%. This got you 4,006 shares in total. Today, the stock is at $39.89, giving your stake a market value of $159,799.34 plus you collected $36,775.08 in cash dividends along the way for a grand total of $196,554.42.

Is that good? Yeah, it’s fine. It represents a compound annual growth rate of around 6.3%. You beat inflation during a decade of war, two economic collapses, and significant political change so that’s something about which to be happy. This is roughly in line with Carnival’s average long-term return on capital, which is low because it requires billions of dollars worth of cruise ships, is highly sensitive to the economy, must utilize a large amount of debt to conduct operations, has non-diversified base of revenue, and suffers from high economic brand equity risk (e.g., one ship poisons a lot of people, all the ships in the fleet are going to experience a drop in ticket sales). You suffered a pretty horrific dividend cut in there, which was later restored (hope you weren’t living off that money otherwise you might have had to scramble to cover your bills!).

Now, let’s compare that to McCormick & Company. It is a far superior business by every conceivable metric; good returns on capital, a low debt burden, 41% of sales from international markets, a diversified product base operating under multiple brand names, an astonishing record of raising the cash dividend every single year for 89 years in a row, greater stability in profits even when the world is falling apart; the list is endless. It’s a beautiful company. So beautiful, in fact, that I bought some this week for my own mother’s long-term account that I expect her to own for the rest of her life. While profits started out around the same level as Carnival, the fact that management can put that money to much better use, at much greater returns, exerts an influence on the numbers.

Imagine back in 2003, you bought $100,000 worth of McCormick & Company when the stock market opened, paying $23.25 per share. This got you 4,301 shares in total. That was a good price. For an excellent business, you got a base earnings yield of 6.02%; quite a bit less than Carnival, but still very attractive relative to Treasury bonds at the time. Today, the stock is at $68.76, giving your stake a market value of $295,736.76 plus you collected $39,483.18 in cash dividends along the way for a grand total of $335,219.94.

Is that good? You bet. It represents a compound annual growth rate of around 11.6%. You crushed the S&P 500 over this period, and were free to ignore stock market fluctuations because the dividend checks got fatter every single year. You didn’t have to do anything and more money was mailed to you. Profits, dividends, all in tandem keep marching every higher, year after year, even in the midst of a total economic catastrophe, while shares outstanding keep dropping. The best part? It was done without a lot of debt. (And they send you spice-scented annual reports, which is nice.)

How Is This Possible When The Two Businesses Appeared To Earn the Same Profit and Pay the Same Dividends?

How can two seemingly similar companies have such drastically different results? A large part of the secret is hidden in the cash flow statement. Not all profit is created equally. Some companies require ever-increasing sums of money to be churned back into them, like a coal furnace, to operate. Other companies don’t need that so the profit is true surplus; free for the owner to do whatever he or she wants without harming the competitive position of the enterprise.

In other words, to briefly touch on an explanation of EPS vs Cash Flow when calculating intrinsic value, the profits may look the same, but McCormick is earning a lot more money. It’s one of those things that requires you to jump into the financials and rip apart the accounting.

To oversimplify it a bit, McCormick requires less capital to operate than Carnival and has none of the weaknesses of Carnival’s business. To produce its earning growth, it only had to plow $7.47 back into capital expenditures. The rest of the retained money was used for share reductions, acquisitions, and other productive uses. Meanwhile, to produce that same earnings growth, Carnival had to plow $25.78 of new money into capital expenditures, which retained earnings alone weren’t sufficient to cover so it had to increase its short-term debt.

Thus, despite seemingly equal beginning valuations, seemingly equal earnings and dividends, and seemingly equal present valuations, McCormick generated a lot more wealth for its owners – almost twice as much – than Carnival over the past eleven years. This doesn’t mean Carnival is bad. Far from it. It’s a perfectly mediocre business that does a lot right, especially as a leader in its industry. Heaven knows you could do a lot worse. It very well could be a great trade if you could get it cheaply due to some disaster or mishap. In fact, less-than-excellent businesses can often be a great way to make huge gains during an economic recovery (e.g., see Carnival competitor Royal Caribbean during the 2009 recession – shares fell from $55.50 a few years prior to $5.40, then rose, again, to $47.14 today; someone buying at the bottom could have made a hell of a lot of money – far more than buying McCormick on the cheap – but that is a different kind of operation with higher risks).

It’s just that a company like McCormick is so vastly superior without even trying that a company like Carnival can’t compete when the base valuations are identical. The McCormicks of the world are going to win over long stretches almost every time. (Again, for trading purposes, this is not true. There may be circumstances in which someone who wanted to trade a stock could do better with a short-term position in Carnival. That’s not really the type of investing we’re discussing.)

Carnival May Be a Better Short-Term Position Than a Firm Like McCormick. Who Knows?

This is why I am so forceful when I say that, personally, I don’t understand how anyone can want to own Carnival when it is selling for the same valuation as a firm like McCormick, or Coca-Cola, or PepsiCo. Over periods of 10, 15, 25+ years, the latter three should crush the former (though that’s not guaranteed – nothing is certain in this world, you can only tip probabilities in your favor using math). To buy it as a first choice for a buy-and-hold portfolio would be like passing a dinner of filet mignon, king crab, and Crème Brûlée so you can pay the same amount for a satisfactory ham sandwich. Sure, the ham sandwich is nice. It will satiate your hunger. You’ll go away happy. But it doesn’t compare. It wouldn’t come anywhere near my definition of “excellent”, nor would it be on the top, or even middle, of my wish list unless I could get it for a stupidly cheap price, which is not the case at the moment.

You’d have made a lot of money buying Carnival 25 years ago. You’d have gotten much richer buying any of the higher quality companies, even if you paid more for them.

This is absolutely not a stock recommendation. Again, I have no idea what is going to happen in the near future. Carnival may utterly crush McCormick, or Coca-Cola, or any other firm you can name. All I can say is that over the next quarter century, I’d bet my own money that the higher quality enterprises are going to result in greater wealth accumulation if you are the type of investor who buys blocks of stock to lock away in a bank vault, compounding for you year after year. Even if they didn’t, they sure as heck are going to be a lot more stable and safer about it, which has its own value.

That is how I think about situations like this. If someone were to show up and say, “You can pick 1,000 shares of either enterprise at present valuation, but you must hold the stock until retirement”, it’s not a difficult choice. In fact, it would take less than a second for me to reach for the McCormick certificate while gently whispering, “My precious”, as I visualized exotic cinnamon shipments, exciting peppercorn stockpiles, and warehouses of saffron. I’d let the other guy keep the cruise ships, unless they were part of a larger empire, like The Walt Disney Company, which has the internal resources to extract more value out of each dollar invested. Besides, McCormick supplies most of the commercial kitchens in the world, so I’d be making money off Carnival Cruises, anyway, as the guests on the boat ate their breakfast, lunch, and dinner.

Reader Comments

(14)

Comments are presented chronologically, with replies indented beneath

the comments to which they respond.

F

FratMan

December 28, 2013

Damn, that's what you call a kick-ass article.

Two questions.

First, you mention: "an astonishing record of raising the cash dividend every single year for 89 years in a row." Does that make McCormick the company in the US with the longest streak of annual dividend raises? You always hear about Diebold and American States Water, and stuff like that. Most of the lists I've seen only show annual dividend growth records dating back to the 1950s, but I could see how a company like McCormick could easily slip under the radar.

And secondly, this is a question that I should've asked a long time ago, but how do you prefer to be addressed: Josh? Joshua? Mr. Kennon? Something else? My bad on never asking that.

G

Gilvus

December 28, 2013

Replying to FratMan

- JAK (middle name)

- Koshua Jennon

- J-to-tha-oshua Kennon

- Jean Honk Onus

Last one's an anagram. I'll show myself out.

M

moshe

January 3, 2014

Replying to FratMan

Joshua is the one who brought the jews into the land of kennon

A

AMead

December 28, 2013

Joshua, for the "mechanically-minded" among us, where are you getting your CAPEX figures? I just did a quick "back of the Excel" analysis using Morningstar's data and came up with $7.14/sh. Close enough but just wanted to see where your data comes from. Google Finance perhaps? I've been eyeing MKC for a few years now myself. Great company, but the valuation is a bit higher than my liking (plenty of other places capital is needed in my life), and I'm not willing to dip into my liquidity just to earn a bit more interest/dividends, etc. Sorry for the digression there...fantastic article and thanks in advance!

K

kl

December 28, 2013

Hi Joshua,

Thanks for your blog articles. Regarding estimating/forecasting future EPS growth, some books (from memory I think buffetology does this) seem to imply it it ROE*(1-payout ratio) but when the company is leveraged it needs to take some earnings to service the debt and the above doesn't apply. E.g. CL's growth is no where near ROE*(1-payout ratio). Do you have a methodology for estimating EPS growth when ROE is very high due to debt?

All the best & happy xmas,

K

M

Mario

December 28, 2013

Replying to kl

K, I know Josh will have a more insightful answer, but I'll share with you what I know:

The above does apply to leveraged companies, since ROE is calculated using net income, meaning interest has already been paid. The key is to understand the assumptions of the model. From the top of my head:

- The return on marginal investments is the same as the return on previous investments.

- The capital structure stays the same.

- The dividend payout ratio is constant.

- There are no share repurchases.

If an assumption is violated, then actual growth might differ from projected growth.

Hope this helps!

K

kl

December 28, 2013

Replying to Mario

Hi,

Thanks for your reply Mario - makes sense, in the case of CL, even using the highest payout ratio from 2008-2012 and lowest ROE to get an estimate for EPS growth doesn't explain the gap.

ROE * (1-payout ratio) ~= 50%

and realised EPS growth is not as high, not for basic/not for diluted EPS :/ therefore share buybacks or dilution won't close the gap between projected growth and realised EPS growth.

By changes in the capital structure do you mean that assuming eps growth = roe(1-payout) assumes silently that shareholder equity also grows by roe(1-payout) ?

All the best,

K

D

Divi Me Up

December 28, 2013

Wow, first time I have come across your blog and I find this gem. Great article! While I have MKC on my list of stocks I track, I haven't looked into it in depth as I wasn't excited about its valuation at first glance. Will have to take a deeper look. This article will give me something to think about each time I look at a new potential purchase. Thanks!

J

Joshua Kennon

January 18, 2014

Replying to Divi Me Up

Welcome to the site!

J

James

January 30, 2014

MKC took a little tumble yesterday. I would love to own this company but it still seems too expensive. This seems like a company Buffett would buy in its entirety; only has a market cap of $8B. I'd rather own it that way than buy it myself.

M

mrcolesmith

November 3, 2014

Good day Joshua,

I really appreciate the amount of effort and time you have devoted to writing these insightful articles. I'm not an expert myself so naturally, there are some things that I do not get.

One of them is: how is the return on capital for McCormick (i.e. 16.62%) calculated in the table you show?

Thanks in advance for helping out. 🙂

M

Muhammad

January 24, 2015

this is one of my favourite posts on the site. the other being the one on how Jack Mcdonald made 188 million USD by investing in the stock market. Another one i liked a lot was the one on Walter Schloss and how he left Graham and Newman in order to strike out on his own. All these posts are very close to my heart. thanks again Joshua! ur work is awesome! 🙂

M

Muhammad

March 17, 2016

Hello Joshua, hope you are well. I just wanted to ask you if I buy something online by following a link from your website then do you get paid for it? I'm asking cause I sometimes shop on-line and would like for your website to benefit from my purchases. The reason why I want this is because your writing/writing has helped me a lot and I would like to return the favour in my own small way.

The issue that I face is that once i have made a purchase I then start getting links to the same products afterwards, on your website. Since I have already made the purchase in most cases i dont think its the most effective strategy to market the same product to me after I have just purchased it.

P.s: I'm about to make a purchase from Old Navy USA website. Please let me know what I can do so all my online purchases are through your website.

Thanks!

G

galacticduck

March 30, 2016

McCormick was such a brilliant pick. I don't usually piggyback, but I bought this stock because of you, Joshua and am very grateful that I did. Nice coriander-scented annual report, too!

{kind=link}

FratMan

December 28, 2013

Damn, that's what you call a kick-ass article.

Two questions.

First, you mention: "an astonishing record of raising the cash dividend every single year for 89 years in a row." Does that make McCormick the company in the US with the longest streak of annual dividend raises? You always hear about Diebold and American States Water, and stuff like that. Most of the lists I've seen only show annual dividend growth records dating back to the 1950s, but I could see how a company like McCormick could easily slip under the radar.

And secondly, this is a question that I should've asked a long time ago, but how do you prefer to be addressed: Josh? Joshua? Mr. Kennon? Something else? My bad on never asking that.

Gilvus

December 28, 2013

Replying to FratMan

- JAK (middle name)

- Koshua Jennon

- J-to-tha-oshua Kennon

- Jean Honk Onus

Last one's an anagram. I'll show myself out.

moshe

January 3, 2014

Replying to FratMan

Joshua is the one who brought the jews into the land of kennon

AMead

December 28, 2013

Joshua, for the "mechanically-minded" among us, where are you getting your CAPEX figures? I just did a quick "back of the Excel" analysis using Morningstar's data and came up with $7.14/sh. Close enough but just wanted to see where your data comes from. Google Finance perhaps? I've been eyeing MKC for a few years now myself. Great company, but the valuation is a bit higher than my liking (plenty of other places capital is needed in my life), and I'm not willing to dip into my liquidity just to earn a bit more interest/dividends, etc. Sorry for the digression there...fantastic article and thanks in advance!

kl

December 28, 2013

Hi Joshua,

Thanks for your blog articles. Regarding estimating/forecasting future EPS growth, some books (from memory I think buffetology does this) seem to imply it it ROE*(1-payout ratio) but when the company is leveraged it needs to take some earnings to service the debt and the above doesn't apply. E.g. CL's growth is no where near ROE*(1-payout ratio). Do you have a methodology for estimating EPS growth when ROE is very high due to debt?

All the best & happy xmas,

K

Mario

December 28, 2013

Replying to kl

K, I know Josh will have a more insightful answer, but I'll share with you what I know:

The above does apply to leveraged companies, since ROE is calculated using net income, meaning interest has already been paid. The key is to understand the assumptions of the model. From the top of my head:

- The return on marginal investments is the same as the return on previous investments.

- The capital structure stays the same.

- The dividend payout ratio is constant.

- There are no share repurchases.

If an assumption is violated, then actual growth might differ from projected growth.

Hope this helps!

kl

December 28, 2013

Replying to Mario

Hi,

Thanks for your reply Mario - makes sense, in the case of CL, even using the highest payout ratio from 2008-2012 and lowest ROE to get an estimate for EPS growth doesn't explain the gap.

ROE * (1-payout ratio) ~= 50%

and realised EPS growth is not as high, not for basic/not for diluted EPS :/ therefore share buybacks or dilution won't close the gap between projected growth and realised EPS growth.

By changes in the capital structure do you mean that assuming eps growth = roe(1-payout) assumes silently that shareholder equity also grows by roe(1-payout) ?

All the best,

K

Divi Me Up

December 28, 2013

Wow, first time I have come across your blog and I find this gem. Great article! While I have MKC on my list of stocks I track, I haven't looked into it in depth as I wasn't excited about its valuation at first glance. Will have to take a deeper look. This article will give me something to think about each time I look at a new potential purchase. Thanks!

Joshua Kennon

January 18, 2014

Replying to Divi Me Up

Welcome to the site!

James

January 30, 2014

MKC took a little tumble yesterday. I would love to own this company but it still seems too expensive. This seems like a company Buffett would buy in its entirety; only has a market cap of $8B. I'd rather own it that way than buy it myself.

mrcolesmith

November 3, 2014

Good day Joshua,

I really appreciate the amount of effort and time you have devoted to writing these insightful articles. I'm not an expert myself so naturally, there are some things that I do not get.

One of them is: how is the return on capital for McCormick (i.e. 16.62%) calculated in the table you show?

Thanks in advance for helping out. 🙂

Muhammad

January 24, 2015

this is one of my favourite posts on the site. the other being the one on how Jack Mcdonald made 188 million USD by investing in the stock market. Another one i liked a lot was the one on Walter Schloss and how he left Graham and Newman in order to strike out on his own. All these posts are very close to my heart. thanks again Joshua! ur work is awesome! 🙂

Muhammad

March 17, 2016

Hello Joshua, hope you are well. I just wanted to ask you if I buy something online by following a link from your website then do you get paid for it? I'm asking cause I sometimes shop on-line and would like for your website to benefit from my purchases. The reason why I want this is because your writing/writing has helped me a lot and I would like to return the favour in my own small way.

The issue that I face is that once i have made a purchase I then start getting links to the same products afterwards, on your website. Since I have already made the purchase in most cases i dont think its the most effective strategy to market the same product to me after I have just purchased it.

P.s: I'm about to make a purchase from Old Navy USA website. Please let me know what I can do so all my online purchases are through your website.

Thanks!

galacticduck

March 30, 2016

McCormick was such a brilliant pick. I don't usually piggyback, but I bought this stock because of you, Joshua and am very grateful that I did. Nice coriander-scented annual report, too!