Let’s Talk About Investing in Oil Stocks

I’ve received a significant number of requests over the past few months asking that I discuss what is happening with oil, natural gas, pipeline, and refining companies; to explain how I look at the situation and the sorts of things Aaron and I discuss when we’re allocating our own capital or the capital of those who have entrusted their assets to us.

It’s a big topic with a lot of niche considerations but I want to take some time today to address the oil majors; the handful of mega-capitalization behemoths such as ExxonMobil, Chevron, Royal Dutch Shell, Total, ConocoPhillips / Phillips 66, and BP, with resources that rival entire governments and have a diversified operating structure, typically consisting of some combination of 1.) exploration and extraction, 2.) refining, 3.) chemicals, and 4.) distribution or retail sales rather than specializing in any one thing, allowing each to benefit from economies of scale and lower overall operating costs. This diversified business model arose in no small part due to the experience of John D. Rockefeller and his fellow oil tycoons around the world back in the 19th century when they witnessed firsthand how poor planning could turn an otherwise lucrative partnership or corporation into a money-losing, life-destroying nightmare. In 1866, by way of illustration, the price of a barrel of crude oil fluctuated in non-inflation adjusted terms from $0.10 to $10.00; an oscillation that is all but unthinkable today, making the recent movement in the commodity look cute in comparison.

By making sure they built empires that could survive all environments, and provide comfortably secure dividends for owners through “the cycle”, as it is sometimes called, they created these rare powerhouses that are among the biggest, oldest, and most widely held of the blue chips. They represent a good chunk of the underlying holdings of certain index funds, such as the S&P 500, and have a cherished place in the portfolio of nearly every pension, widow, and conservatively managed trust fund in the United States. They’re also an enduring favorite of many of the secret millionaires we so frequently discuss. When former Mobil secretary Phyllis Stone died, a local charity was shocked to discover her donation following the revealing of a $6,000,000 fortune she had built up consisting mostly of tens of thousands of ExxonMobil shares, acquired over the decades from her modest income. Perry “Bit” Whatley, a retired machinist, amassed nearly $2,000,000 due, in part, to his ExxonMobil stake, which ultimately led to a protracted legal fight after a family drama involving attempts to seize the portfolio. A barber named Earl Doren never made it through eighth grade but following a career in the United States military, he went into business for himself, working for more than forty years. Some of his clients were smart businessmen, to whom he listened. He ended up with a $1,800,000 fortune that he gifted to a charitable trust, which included a sizable ExxonMobil position. On and on the roster goes, all the way up to old money and royalty; the Queen of the Netherlands is a major shareholder in Royal Dutch Shell, making her family billionaires, as is Queen Elizabeth of England.

If you’re reading this and you have any investments, anywhere, the odds are good somehow, some of that money is being generated from one or more of the oil majors. You are big oil and your family is an oil family. It is the backbone of the global economy; the producers of hydrocarbons that make possible the manufacturing, production, and distribution of everything from paint to carpet, chemicals to electricity. Without it, modern civilization could not exist.

Oil Companies, and Thus Oil Stocks, Have Unique Characteristics That Make Their Business Model Different from Most Operating Companies

If you own a business, whether it be a retail store, a doughnut shop, a medical supply company, or a manufacturing plant, you are typically looking to increase sales and profits with each passing year; to examine this twelve-month period in the light of the former twelve-month period to see if things are improving. As seemingly arbitrary as it is, we use one trip around the nearest star as the line of demarcation for every period of measurement even though it doesn’t have any particular relevance to the actual cycles of most firms. When you go to sell shares of your business either to cash out or to get an infusion of capital to increase the speed at which you can grow the enterprise, investors will examine the recent results, determine what they think the future results will be based upon the financial statements and other variables, then offer you a multiple. “I see here, Mr. & Mrs. Smith, that your chocolate business generates $3,000,000 in after-tax profits every trip around that star, and has historically grown at 6% per annum. We’ll offer you $40,000,000 to acquire it.”

The oil majors aren’t like this. They have extraordinarily long cycles of identifying, sourcing, extracting, refining, producing, distributing, and selling their products and services, sometimes stretching for 30 to 50 years or longer. Their executives, operators, and shareholders cannot think in terms of quarters, but rather, they must look at the income statement, balance sheet, and cash flow statement through the lens of decades or generations. Part of this is logistical – you don’t wake up one morning and decide you need to find huge oil reserves, having them fall into your lap; you have to search, plan, and pay for them far in advance – part of it is a by-product of the fact that demand for the oil majors’ primary products, ranging from crude oil, jet fuel, gasoline, heating oil, motor oil, and more, ebbs and flows with the larger business cycle of economic expansion and contraction. You can have multi-year periods when you’re on the receiving end of torrents of earnings that drown you and your fellow owners in record-shattering profits only to be followed by the spigot getting shut off, mass layoffs, and forced curtailing of planned projects to save on the capital expenditures as you want to reserve as much cash as you can.

The oil majors are not just oil companies. They are so much more. Most are integrated with refining businesses that then turn the raw materials into higher-margin substances, such as jet fuel or engine oil. They own huge chemical companies (ExxonMobil, by way of example, would be one of the largest stand-alone chemical businesses in the world if it were forced to divest its subsidiary). They own transportation businesses. They own franchise operations (gas stations and convenience stores).

In practical terms, for existing and potential owners, it means you’re missing the big picture if you try and look at the current price-to-earnings ratio, earnings yield, price-to-sales ratio, or many of the other popular metrics in any given year. It’s entirely possible for your oil major stock to be significantly overvalued at 10x earnings and significantly undervalued at 20x earnings based on where we are in the cycle (the former is known as a “peak earnings value trap“).

Take, for example, the old Standard Oil of California, or as most people know it these days, Chevron. It has fallen from a high of $129.53 in the past 52 weeks to $71.45 as of this moment. Yet, if you knew for certain that the price of crude was going to stay below $40.00 per barrel for the next five or ten years, you could objectively state that it is significantly overpriced. In fact, if you knew for certain that the price of crude was going to stay below $40.00 per barrel for the next five or ten years, you could objectively state that the entire oil sector in the S&P 500 is the most overvalued sector in the index by a wide margin.1

For the oil majors (as opposed to the pure plays, which are a different story), that’s not the whole picture. It is entirely possible for a trader or hedge fund manager to say oil stocks are overpriced at the moment, calling for them to decline and a long-term investor to say that oil stocks are undervalued at the moment, preaching you should use your funds to load up on them. That seems almost nonsensical; a paradox. Nevertheless, it’s true when you understand one fundamental fact: When you buy a share of the oil majors outright, paying for it in cash and locking it away, you are being paid to absorb volatility over multi-year periods.

Read that last paragraph, again. Think about it for a few minutes. Let it sink in so it becomes a permanent part of your investment file.

Got it? Now, let’s examine how it works.

Long-Term Investors in the Oil Majors Are Being Paid to Absorb Volatility Over Multi-Year Periods

In recent weeks, there have been several discussions in the comments about the highly-respected work of Dr. Jeremy Siegel at the Wharton School of Business. It seems only appropriate he would come up in the conversation today because a decade ago, he released one of my favorite books, which over nearly 300 pages provided an examination of the original S&P 500 components from February 28th, 1957 through December 31st, 2003; as if a buy-and-hold investor came in, acquired all of the stocks, and then sat on his or her behind. Dr. Siegel and his research assistants performed exhaustive calculations, tracing the compound annual growth rate of every component through mergers, spin-offs, split-offs, bankruptcies, buyouts, and more. For those of you who haven’t read it, the appendices alone are worth the price. Pick up a copy the first chance you get and read it cover-to-cover. It’s called The Future for Investors: Why the Tried and the True Triumph Over the Bold and the New.

Toward the end, he discusses the dominance of oil. In the original S&P 500 index of 1957, 9 out of the largest 20 firms were oil companies. Relatively, the oil sector has shrunk significantly in the meantime. Yet, for the almost half-century his study encompassed, he found that when he traced the results of those top twenty largest firms, the highest performing five businesses at the end of the period all came from the oil sector. In fact, 7 of the top 10 highest performing among the former largest component weightings came from the oil sector. The oil majors, as a group, outperformed the S&P 500 as a whole by 2% to 3% per annum for nearly half a century. (Don’t scoff at that. To put it into perspective, if you could earn an extra 3% over 50 years, you’d end up with triple the terminal net worth. It’s life changing.)

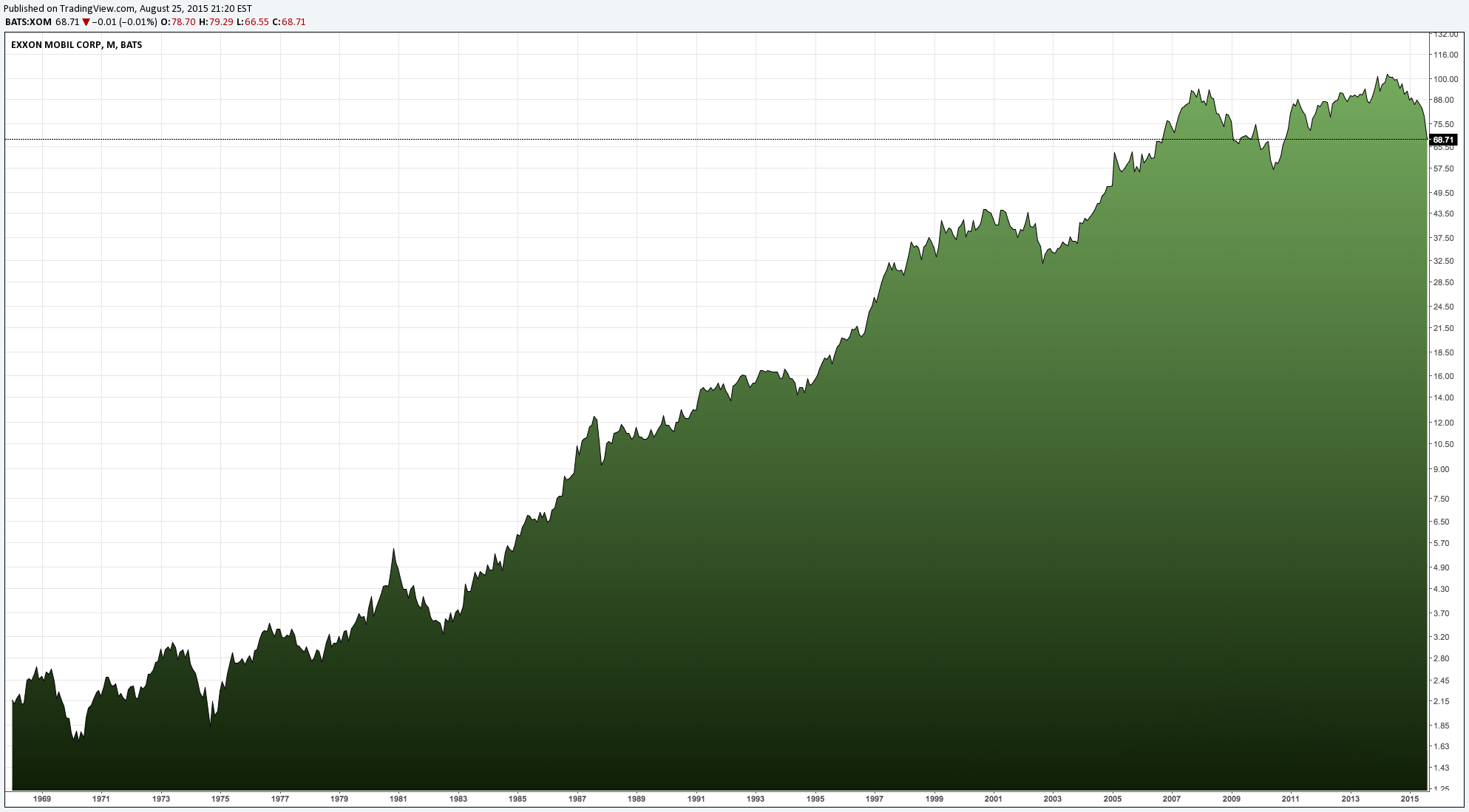

How could this happen? Oil shares are notorious for these boom-and-bust cycles; for skyrocketing then collapsing or going sideways for 5, 7, 10 years at a time. Indeed, when I did my 25-year case study of Chevron, I noted how the stock never seemed to trade outside of a range of $40 per share to $120 per share if you picked up the newspaper and weren’t paying close attention. How can it be that an owner of these massive corporations ended up not only matching the S&P 500, but substantially exceeding it over the same period to the point the ending differential in wealth was staggering? Take a look at the logarithmically-adjusted chart for ExxonMobil (it treats a rise from $10 per share to $100 per share the same as a rise from $100 per share to $1,000 per share since it represents the same mathematical gain and helps avoid skew toward larger numbers). The chart covers all of the past data I can easily access from a publicly created tool you yourself can replicate so it encompasses a slightly different period (the late 1960’s-today) than Dr. Siegel’s research did but the results are comparable because the same powers are at work.

What do you notice? There are many times when you’d buy ExxonMobil and watch it fall 20%, 30%, 50%, then take 3-5 years just to get you back to breakeven on a share basis alone. It does not appear to be a recipe for getting rich, let alone trouncing the indices but, somehow, someway, there’s a more than 30-fold rise in stock price. That doesn’t even include dividends or reinvested dividends, which are often a major part of the total return of big oil. What strange magic is at work? How could such a thing occur when you spend most of your time sitting on big losses or going sideways?

The answer can be found in the difference between long-term investors who buy through the cycle, absorbing the volatility, and short-term traders who make money flipping the stock for short gains. Shorter-term investors (5 years or less) tend to buy or sell the stock based on what they think earnings are going to be or whether the stock will rise or fall. Longer-term owners look at the premier energy company on planet Earth and conclude that, when the shares are attractive, as long as they hold for several decades (and sometimes accept paper losses that last longer than entire Presidential administrations), the odds are good they will eventually emerge wealthier due to a combination of:

- The mathematics of increasing dividends reinvested at a time of declining stock prices. As the stock price falls, your dividends buy more shares. As the company raises the dividends, your dividends buy more shares. Working together, you get this effect that starts to make a huge difference once you get 15, 20, 25+ years out in the future.

- Share repurchases authorized by stockholders and overseen by the board of directors that increase the absolute equity ownership per share as outstanding share count declines

- The ability of the oil majors to use market wipe-outs to buy up their competitors’ assets for pennies on the dollar after the weaker competitors have to beg for mercy in bankruptcy court or who have to acquiesce given their inability to remain independent when cash is tight, unable to fight off non-desired suitors; an ability that arises from the integrated, multi-stream earnings model

Let’s look at ExxonMobil to illustrate how these work. We’ll start with the first two – reinvested dividends and share repurchases – then move on to the last point in a moment.

How the Major Oil Stocks Accelerate Returns with Reinvested Dividends and Share Repurchases

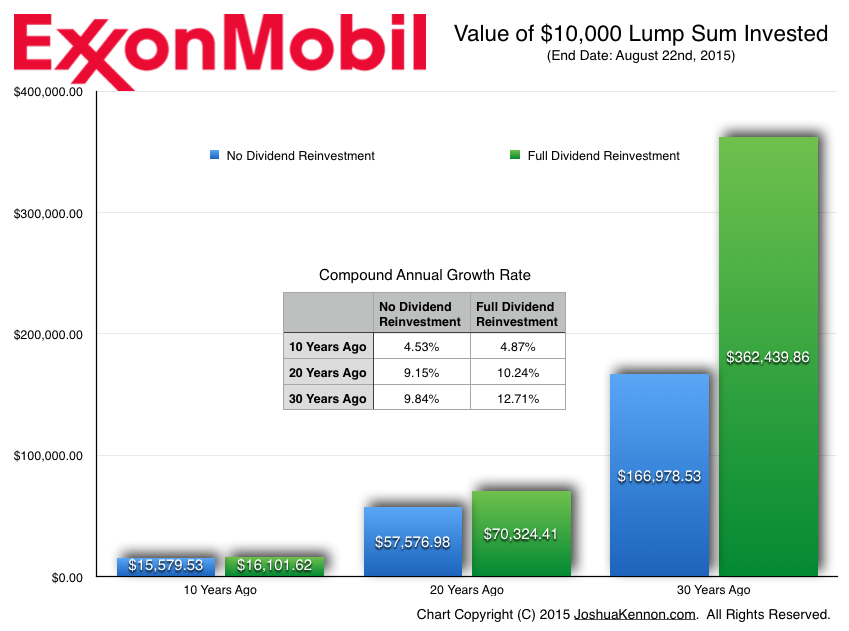

Keep in mind that since we are in the middle of an oil crash, the figures are far less attractive in terms of terminal value than they were last year, when they would have been nearly 50% higher due to the share price reaching almost $105. It’s the nature of the oil majors.

Note: The “No Dividend Reinvestment” figure shown in the chart is for total return (share appreciation/depreciation + dividends). Figures do not reflect taxes or inflation.

Even with the huge drop in ExxonMobil’s shares as we begin another crude oil crash – this one the worst since the legendary collapse of 1986, which took everyone from wildcatters to bankers by surprise and devastated the lives of millions of people – the full dividend reinvestment portfolio of ExxonMobil over the past 30 years has compounded at 12.71% compared to 10.61% for the S&P 500. That 2.10% differential might not sound like much but there’s a big difference between a $362,439.86 ending figure and the S&P’s $195,978.90 ending figure. It’s $166,460.96, or 84.94% more money. (Again, the number was much more impressive last year, underscoring the nature of the industry.) Generally speaking, you should not buy ExxonMobil unless you plan on making it a generational holding; one that is passed down through the family tree for you, your children, and your grandchildren to enjoy the stream of ever-increasing dividends while management figures out how to increase profits from all divisions.

The same pattern plays out over and over again. When Dr. Siegel looked at at the 1957-2003 original component S&P 500 returns, he found that:

- Royal Dutch Petroleum (now Royal Dutch Shell) compounded at 13.64%

- Shell Oil (now Royal Dutch Shell) compounded at 13.14%

- Socony Mobil Oil > Mobil (1966) > Now ExxonMobil compounded at 13.13%

- Standard Oil of Indiana > Amoco (1985) > Now BP (1998) compounded at 12.83%

- Standard Oil of New Jersey > Exxon (1972) > ExxonMobil (1999) compounded at 12.55%

- Gulf Oil > Gulf – Chevron (1984) > ChevronTexaco (2001) > Chevron compounded at 12.14%

- Standard Oil of California > Chevron (1984) > ChevronTexaco > Chevron compounded at 11.62%

- Texas Co. > Texaco (1959) > ChevronTexaco (2001) > Chevron compounded at 10.93%

- Phillips Petroleum > ConocoPhillips (2002) compounded at 10.76%

The only relative failure among the initial bunch was Rockefeller’s old Marathon Oil, which wasn’t even publicly traded on its own for a long time but was, instead, a subsidiary of U.S. Steel, drug down by the performance of the low-profit, high-capital steel industry.

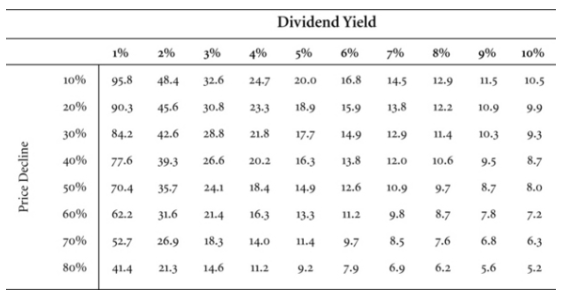

The secret is partially found in the higher-than-average dividend yields. Dr. Siegel produced two charts to explain the math to those who hadn’t run the numbers themselves (on pages 150 and 151 of the aforementioned book) demonstrating how reinvesting dividends in falling stocks of fundamentally good businesses could lead to lower breakeven points and outsized results down the line when the industry recovered; a perfect explanation for the boom-and-bust nature of big oil, refining, and chemicals. He calls this the “Return Accelerator” and explains, “Dividend-paying stocks do well through market cycles, since investors who reinvested dividends accumulate more shares during bear markets. Table 10.2 shows how many years it takes after a stock declines for investors to achieve the same return they would have received had the stock price not declined. These tables assumes the firm maintains its dividend. The investor recoups the price loss because the lower price allows dividend-reinvesting investors to accumulate more shares than they would have accumulated had the stock never declined. The value of these extra shares eventually surpasses the magnitude of the price decline, making the investors better off. As can be seen, the greater the dividend yield, the shorter the time needed for investors to recover their losses. Surprisingly, the table also shows that the greater the decline in price, the shorter the period of time needed to break even, since reinvested dividends accumulate at an even faster rate.”

TABLE 10.2: YEARS TO BREAK EVEN AFTER PRICE DECLINES

Source: Jeremy Siegel Table 10.2, Page 150, The Future for Investors: Why the Tried and the True Triumph Over the Bold and the New

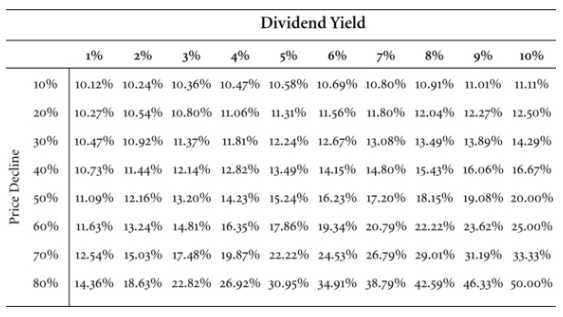

He continues later, saying, “Table 10.3 illustrates the return accelerator. It shows the return investors would earn if the price of the stock returns to its original level after the number of years indicated in Table 10.2. We noted above that if a stock had a 5 percent dividend yield and declined by 50 percent, it would achieve the same return in 14.9 years as a stock that had not declined at all. If after 14.9 years, the stock that fell 50 percent recovers to its original price, the annual return on the stock over those 14.9 years would rise to 15.24 percent, a return that is 50 percent greater than what the stock would have been had the stock not fallen in price.”

TABLE 10.3: ANNUAL RETURN WHEN PRICE RECOVERS

Source: Jeremy Siegel Table 10.3, Page 151, The Future for Investors: Why the Tried and the True Triumph Over the Bold and the New

In other words: The more painful the busts, the longer they last, the higher the eventual compounding return. You’re being paid to absorb volatility.

Firms that intelligently repurchase shares achieve the same effect as Siegel goes on to explain in the subsequent passages on buy backs. For ExxonMobil, this is a major part of the strategy, though there have been some less-than-ideal allocation practices in the past with most repurchases coming during boom periods to the dismay of certain financial journalists and analysts. Exxon was steeped in the Rockefeller culture and conservatism (up through the 1980s, the legendary old-time religion of the patriarch remained in the board room, which opened meetings with a prayer). It prioritizes the safety of the dividend over the amount of the dividend, having lower payout rates than its European counterparts. Instead, when times are good, it takes the earnings and repurchases unfathomable amounts of stock, destroying it to reduce the outstanding tally. Pull a recent ValueLine report on the firm and you’ll see that in 1999, there were 6.954 billion shares outstanding. This year, the oil giant is expected to have reduced that to 4.17 billion shares outstanding. That’s 2.784 billion shares gone. Each share bought in 1999 now represents 40% more ownership of the actual business. Spreading dividend distributions over fewer shares is one of the reasons it has been able to hike the dividend rate per share from $0.84 back in 1999 to $2.92 per share today. (The year I was born, the dividend was a split-adjusted $0.376 per share. Had you never reinvested any of your dividends, nor bought another share, you’d have watched your per share income rise 7.77 fold.)

Take it all together and the picture starts to emerge, fully alive and brilliant. You see how, especially in tax-sheltered accounts, it might be viewed by wealthy and experienced investors as a wise decision to buy firms like Royal Dutch Shell or ExxonMobil at the time the stock is collapsing, plowing the dividends back in on themselves, accumulating year after year despite seeing tons of red ink on your account statements. You start to understand how 40% unrealized losses brought on by an oil crash don’t mean much in the face of 4%, 5%, 6%, 10%+ (in the case of the 1930s and 1980s) cash dividend yields as you amass more shares with the rich payouts.

How the Major Oil Companies Strengthen Their Competitive Positions and Future Cash Flows During Oil and/or Stock Market Collapses

Meanwhile, the oil majors lay the groundwork for significant profitability increases down the road during crashes. The economies of scale they possess due to their enormous balance sheets and technical expertise allow them to drill or extract oil and natural gas at a fraction of the price their smaller competitors can under most circumstances. That means they can remain profitable for longer as the price of energy collapses. Their less profitable counterparts get into trouble, especially if they are in debt. Many go bankrupt and/or find themselves severely distressed, allowing the giants to come in and buy up their assets, debt, and in some cases, equity, for a mere fraction of what it would have commanded prior to the decline. They sail through the nightmare relatively unharmed (take a look at what has been happening at ExxonMobil and Royal Dutch Shell over the past year – with refining margins so high, it’s been softening the blow from the oil free fall).

Indeed, during the last major collapse caused by the Great Recession of 2008-2009, ExxonMobil geared up and acquired XTO Energy in 2010, paying $36 billion for the deal to close (it issued 416 million shares of stock and took on $11 billion in debt but, in exchange, became the largest natural gas producer in the United States). ExxonMobil then used the XTO subsidiary as a vehicle to acquire additional natural gas companies and acreage, tripling its size; e.g., see the 17,800 bought from LINN Energy almost a year ago. All of the newly issued shares have been repurchased and cancelled, undoing the dilution owners experienced, effectively converting it to a nearly all-cash deal (minus a necessary adjustment for the market price differential that occurred as the stock fluctuated in the interim, whereas it would have been a fixed amount in cash) but giving the old XTO owners the ability to defer capital gains taxes. Royal Dutch Shell announced recently it was acquiring BG Group for a whopping $70 billion, which will make it the world’s largest supplier of liquefied natural gas.

Twenty or thirty years from now, the price of these commodities will in all likelihood be considerably higher in nominal terms, the acquisition costs long paid in full. The stockholders of big oil will be collecting much larger dividend checks per share than they are now, perhaps not realizing that the nexus of those funds date back to this period. Those who watched their Royal Dutch Shell Class B shares go from $84.98 to $49.72 will have probably done extraordinarily well, their higher returns compensation for the volatility absorption they were willing to tolerate. And it will be deserved. A not-insignificant percentage of investors simply cannot function or remain calm when they see a huge, negative 41.5% next to their individual stockholding (one of the major benefits, and drawbacks, of index fund investing is it hides the underlying components from the inexperienced investor; he or she may have no idea that they’ve experienced identically proportionate losses to what they would have in a directly held portfolio of individual securities, allowing them to sleep better as night as bizarre as it sounds).

Strategies to Invest in the Stock of the Oil Majors

If you want to become an owner of the oil majors, here is what you might want to consider doing.

First, decide the valuation methodology you will use to acquire shares:

- Buy significant blocks when the businesses are being sold at prices that are objectively cheap on an absolute level compared to some sort of fundamental figure or figures such as ratios-to-book value, ratios-to-proven reserves, or sustainable-dividend yields (the stock simply falling [x]% is insufficient). For example, a handful of times, ExxonMobil has yielded more than 8% to 10%. When and if that day arrives, again, pay close attention. It is a few-times-in-a-century outlier. or

- Regularly dollar cost average into shares regardless of stock market or oil industry conditions, trusting that over 25+ years, it will work out for you. ExxonMobil, since we used it several times in this discussion, has the single best direct stock purchase plan I’ve ever seen. Almost everything is free; they pay practically all of your expenses and will allow you to have as little as $50 a month withdrawn from a checking or savings account to buy more stock. They want long-term, multi-decade, multi-generational owners.

Second, decide how you will construct the portion of your portfolio that resides in oil stocks:

- Buy one, specific firm or

- Create a basket that represents your own personal oil conglomerate, stuffing it with ExxonMobil, BP, Royal Dutch Shell, Chevron, Total, ConocoPhillips, Phillips 66, and a few other holdings, treating the basket itself as if it were one stock so an event like the BP oil spill doesn’t have too large of an effect on the overall portion (e.g., when BP blew out, oil prices went through the roof, increasing profits at competitors). You can weight them equally or you can create some sort of ratio that favors your preferred core holdings; e.g., 20% ExxonMobil, 20% Royal Dutch Shell, 10% Chevron, 10% BP, 10% Total, 10% ConocoPhillips, 10% Phillips 66%, 2.5% to four other firms.

Third, decide how you will treat subsequent allocations. Will you:

- Rebalance each of the holdings in accordance with their original weight once a year?

- Reinvest dividends into the firm that paid them or pool them at the bottom of the portfolio in cash then include those amounts in the annual rebalances and/or spread them evenly across all firms?

- Extract dividends to fund other investments a la the Rockefeller family trust funds, which for generations (up until recently in a fight over environmental causes) used their extensive energy investments to acquire a wide range of additional assets, including funding Apple and Gilead Sciences in the early days of those enterprises?

- Hold spin-offs?

- Sell spin-offs and reinvest in the parent company?

- What will you do if, as is prone to happen from time to time, one or more of your oil giants reduces or eliminates the dividend?

Next, stick with it for a quarter-century at least. Mentally make peace with the fact that you’re going to see jaw-dropping, horrific losses on paper from time to time and repeat to yourself, “I am being paid to absorb volatility others do not want on their balance sheet”. Make sure you won’t ever be forced to sell out early – don’t borrow on margin under any condition, don’t dip into your emergency cash reserves so you might have to liquidate at an inopportune time if disaster strikes. Then go on with the rest of your life.

You could very well buy a share of ExxonMobil (or whatever other oil giant you prefer, so insert name here) only to watch it sit at $0.60 on the dollar for the next seven years. That’s how this industry works. It’s during these times you accumulate more ownership as they go about gobbling up the world’s reserves from weakened competitors. (You’ll learn to take delight in the fact they reduce their own oil output when crude prices collapse but refining margins are high, buying other companies’ oil on the open market to feed into the refineries so they can keep their own reserves for the day when sky-high prices return.)

These aren’t empty words, it’s the way we handle our own capital. On Friday of last week, Aaron and I added some ExxonMobil to our portfolios through a couple of pension accounts that won’t begin payouts until 2042 at the earliest. Earlier this week, we substantially increased the stake to the point it is our fourth largest holding. There is a very real probability it falls to $50, $40 a share or less. If it does, we will dry our eyes with the 4.1%+ tax-free initial yield we managed to grab in the midst of the chaos; a yield that is all but certain to rise over time. Meanwhile, we take a more balanced, less concentrated approach for the accounts under our control; accounts that the people close to us will use to support themselves in old age with more equal amounts of ExxonMobil, Chevron, Royal Dutch Shell, BP, and Total shoved into their retirement and brokerage portfolios.

Some Final Thoughts on Investing in Shares of the Oil Majors

Are shares of the oil majors right for you? It depends on your timeframe and psychology profile. This is one of those areas where raw intelligence doesn’t seem to do much good. You’ll find drop-outs who went to work in the oil field but get the industry; understand its dynamics, when to buy, and how to hang on for dear life as if those equity certificates were the most precious thing in the world, enjoying a stream of checks for the rest of their time on this mortal plane and frequently amassing hundreds of thousands, or even millions of dollars in surplus wealth despite the volatility. On the other hand, you’ll have an otherwise brilliant person who falls apart at watching their $150,000 stake go to $60,000, hit the “sell” button, and swear off “playing the stock market”, as idiotic as that phrase is in this context, transferring the probable future payoffs to someone else with a stronger stomach and understanding of the economic cycle as it pertains to the real business model of the oil majors. (If you need to get a refresher course on how the world merely repeats itself – there is nothing new under the sun – go pull up past historical stories on crude collapses. The entire year 1986 New York Times archives is particularly useful as you could block out the date and almost exactly replay the current situation we are going through at the moment.)

One way you can alleviate this is to design the entire portfolio intelligently. There are certain industries, and companies, that do extraordinarily well when energy prices collapse; the oil majors’ pain is their gain. Consider that in the overall construction. Look to consumer staples like Coca-Cola and Hershey, which sail through booms and busts with equal aplomb. Hold some minimum level of liquid cash along with fixed income securities of short or medium-term duration to provide a buffer in the event of painful deflation. And above all, if you don’t understand what you are doing: Walk away. It’s easier for people who live near something like the Joliet refinery in Illinois to buy shares of ExxonMobil because they can see it. They watch the people walk into the plant every day. They see the products leave it. It’s real. They can reach out and put their hand against the fence or talk to the men and women drawing a paycheck. Never buy an ownership stake in something you do not fully understand or with which you are not fully comfortable.

As for the other areas of oil investment and speculation – the pure play exploration companies, the companies leasing equipment to producers, drilling rights, royalty unit trusts – it is not a place for beginners nor intermediate investors. It is totally unnecessary to becoming financially independent and you run a real risk of losing a substantial portion, if not all, of what you lay out to more experienced capital allocators who understand the industries. The only exception I think passes muster would be something like a directly-held, individually-built, equal-weight portfolio of some kind where diversification was in the hundreds (or more) of individual securities. It’s a very different thing to buy ExxonMobil or Chevron regularly, through boom and busts, than it is to buy Tidewater at $80.00 back at the high of 2007 only to watch it fall as low as $14.35 this year. It’s not a Hershey. It’s not a Clorox. It’s not a Colgate-Palmolive. It looks like a $10,000 investment with dividends reinvested over the past 30 years in that particular firm is now worth $16,417.81 for a pre-tax, pre-inflation compound annual growth rate of 1.67%. I’d have to check and see if there are any spin-offs or weird situations distorting the numbers but it’s a business on which one speculates, not makes long-term commitments. (In comparison, the same $10,000 lump sum invested in been-around-since-the-1800s Colgate-Palmolive 30 years ago with dividends reinvested is now worth $796,117.37, or 15.70% compounded annually. Give me dish soap and toothpaste any day. Johnson & Johnson? That comes to $639,929.85, or 14.86% compounded annually. Even General Electric, which makes the stuff for the oil and natural gas industry? That came to $231,169.85, or 11.03% compounded despite the worst meltdown since the Great Depression, which saw the legendary blue chip cut its dividend due to mismanagement of the banking operations.)

The last paragraph reminds me of a story that was relayed to me. Many, many years ago, I was visiting with a successful analyst at a white-shoe wealth management firm. This firm had a lot of extremely rich clients. All of the partners were rich, too. The analyst told me about a long-term client for whom they had accumulated a lot of riches; crushed the market over the decades their relationship endured despite occasional periods of underperformance due to the nature of their strategy, which involved seeking out deep value. During one particular era, when technology stocks were going through the roof, the investment committee of this firm looked over the client portfolio and for something like 2 or 3 years, didn’t have hardly a single buy or sell order executed, but rather kept him in highly appreciated positions of business like Johnson & Johnson, the deferred taxes effectively leveraging the compounding rate without much additional risk. One day, he called them agitated. “What the hell am I paying you for if you’re going to ignore me? For years I’ve watched all my friends buying these technology stocks and make a killing and you aren’t doing anything. You know how much money that 1.5% per year I pay you is on an account balance as large as mine?! I’m making you rich!”

The partner who took the call, and who had known this person for a long time if I remember correctly, said something along the lines of, “You’re paying us to make you money – and we have made you a lot of money over the years. Right now, we believe the best course of action is to do nothing; to keep you from your own worst instincts and stop you from making a mistake by selling these wonderful businesses we acquired at opportune times when they were being given away. Even more importantly, we want to keep you from then taking the cash you raise and plowing them into garbage that happens to be en vogue at the moment; companies with no real earnings, no real business models, and no hope of survival. You pay us for our advice. Our advice: Go play golf.”

That philosophy is perfectly suited to a position in the oil majors should you decide to become an owner. That can be hard. Go back up to the top of this post and enlarge the chart of ExxonMobil then think about whether or not you could sit there, owning the stock between 1969 and 1976 having made seemingly no progress were it not for the additional shares you held from the dividend reinvestment. Strap yourself in and be prepared for a wait that may last a significant part of the rest of your life. If that’s appealing to you, great. If not, nobody says you have to add more diversification by picking up a few of them. It is your money, after all. Do what makes you most comfortable within the bounds of prudence.

Footnotes

1 Complicating it further is you reach a point at which oil stocks fall so far they no longer trade as proportional ownership in a productive business based upon earnings alone. They either function as 1.) a mechanism for competitors to come in and buy the proven reserves (the commodity itself, with the business having no value), or 2.) a stock option or other derivative that exploits the operating leverage inherent in the business model and thus should be valued using some sort of Black Scholes approach; a speculation mechanism that can lead to speculator gains or losses. Both of those are far beyond the discussion we are having now and wildly inappropriate for nearly everyone reading this.

2 Some reinvestment calculations are from the Quandl data set and generated by a tool created by PK, a software engineer living in Silicon Valley. I haven’t verified the end figures by hand because it’s late and I need to move on to other things. They look roughly approximate enough, in my experience and in light of the past case studies I’ve done, to say they’re correct but I can’t personally vouch for the results. Be aware of that.

Reader Comments (53)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Todd

August 27, 2015

I love this stuff. I get so excited when you write about stocks and holding them many generations. My oldest holding is Walgreens since May 31 1988. My uncle who guided me in value investing stared me with Walgreens. He first bought Walgreens in 1964 and my aunt still holds it to day. He also bought Union Carbite in the 1960's and has the spin off today Pacair and Dow, Texaco he bought in the early 1970's and now is Chevron and Phillup Morris and all there spin offs. He Passed away 2009 / She is holding theses stocks for over 45 + years. And I have been told that I will inherit them which I plan on passing down to my children. It like the century Farm passing it down.

Ang

August 27, 2015

It strikes me that this post is only necessary because a lot of the readers of this blog (though not all) haven't invested for long periods of time and thus have no personal experience with the cycles and the actual psychological effects one feels when everyone around you is commenting on it. There's a huge difference between watching a cycle play out on paper in academic studies and living through the times and getting daily input/feedback from your community and work exposure.

This is my favorite part of this post - more generally applicable to subjects other than oil investing: "It depends on your timeframe and psychology profile. This is one of those areas where raw intelligence doesn’t seem to do much good." I've been thinking a lot lately about how important temperament is when it comes to wealth creation/preservation. It doesn't matter how smart someone is because no one can predict the future, though mathematical aptitude does help. If someone were to approach me and ask me for my limited knowledge on investing, what it is, what its purpose is, and how to get started, my answer would be the following:

1. Investing is owning slices of actual businesses that generate cash for the owner, in forms of either cash dividends, buybacks to increase stock price, or growing the business to increase earnings so stock price increases

2. Investing is not a way to get rich quick, instead, it is a way to park/preserve your wealth generated from your economic engine (read your red ring post last night so this is fresh on my mind) so that you don't lose purchasing power due to inflation/opportunity cost. This is an important point because I get the feeling a lot of beginner investors look at the market as a way to make money, and not as a vehicle for parking money they already generated

3. Investing requires a certain temperament, before going out and learning about investing/reading any books at all, you should practice patience and remaining calm/composed in face of obstacles and unpleasant experiences, more than anything that will lead to either your success or failure. If you happen to discover that you don't have quite the right temperament, create systems/structures so that you are not exposed to the volatility (and thus removing the incentive to act - it's a return killer). A good way to do this is taking money off the top of your economic engine/paycheck and averaging into a diversified stock fund, and never looking at the balance except once a year. To borrow a mandate from you Joshua, know thyself.

Muhammad

August 27, 2015

That explains it. thanks! 🙂

Brandon Higginbotham

August 27, 2015

Thank you for this post Josh! I've helped my mother load up on shares of these majors and look forward to years down the road when the dividends received exceed her cost basis!

Nirav Desai

August 27, 2015

Great write up.

Do you feel the same way about other commodity stocks, like BHP?

Brandon Higginbotham

August 27, 2015

Replying to Nirav Desai

I've also had BHP on my radar. The dividend yield is very attractive and worth looking more deeply into the financials.

Adam @ AdamChudy.com

August 28, 2015

Replying to Nirav Desai

BHP's been written about before here. I think you'll find similar posts if you search.

Jeff

August 28, 2015

Replying to Adam @ AdamChudy.com

I believe Rio Tinto has been mentioned as well.

jack's smirking revenge

August 27, 2015

Great post! Two questions:

1) Any thoughts on the viability of oil companies for the next century? Oil is drying up (slowly), and with climate change getting very urgent we may be forced to cut fossil fuel usage a LOT. Perhaps the next century won't be so kind to oil investors?

2) What are your favorite investing platforms?

Kapitalust

August 27, 2015

Replying to jack's smirking revenge

Let me start off with this statement so that there is no confusion: humanity is spewing a lot of CO2 into the atmosphere and it will effect the climate.

Now, with that being said, the entire modern world is built off the backbone of hydrocarbons. There is little chance humanity can switch completely away from the vast hydrocarbon infrastructure very quickly; I'd wager unlikely in our lifetime.

Will it always be so? Of course not. Renewable energy makes so much more sense than burning up coal/oil/gas. But the switch will take time... a lot of time.

Peruse the Exxon Energy Outlook to 2040. One of the more interesting graphs is the projection of energy usage by 2040. You'll see that there will be no projected growth in coal usage, minimal 0.8% growth in oil, and 1.6% growth in natural gas.

On the other hand, growth in wind/solar/biofuels energy is predicted to be a robust 5.8%. Yet, since wind/solar/biofuels make up such a small portion of the total energy consumed worldwide today, that 5.8% growth will hardly make a dent: global energy consumption will still primarily be based off hydrocarbons in 2040.

It seems unlikely that we will not be using hydrocarbons anytime soon despite the potential dangers of anthropogenic climate change.

lnt90

August 27, 2015

Replying to Kapitalust

ExxonMobil has a great competitive advantage in that I would say that there management team may very well be the smartest and balanced management team in the corporate america. The way they talk in terms of growth....not quarters but in DECADES!! I wish all companies would do this and not just focus on getting the share price boosted up quickly and making a quick buck.

lnt90

August 27, 2015

Replying to jack's smirking revenge

Excellent first question! I would have to say you need to take a long hard look at what exactly your dealing with here. (Using ExxonMobil as an example). Energy has evolved in many different forms over the last few centuries; steam, solar, wind, etc. The energy companies are not idiots, they know there are other competing forms but they also know that atm none come close to the convenience, and ease as oil & its byproduct natural gas. There is simply too many things that are made from oil in our modern societies that would threaten oils reign anytime soon (25 years or so).

This list includes plastics, cell phones, lubricants, clothing, pharmaceuticals, asphalt, tires, paint, shampoo, makeup, fertilizers, and even in our food! This si only to name afew!!

However over the super long term, changes are sure to come and the trick here is THERE WILL ALWAYS BE A NEED FOR ENERGY!! While the form may change it will always be needed. But the Supermajors are in the best position long term to capitalize on it. If a new form of power emerged that threatened oils viability long term the majors would be the first to capitalize on it with there sheer size and expertise. Example: When natural gas made serious headway several decades ago Exxon & Chevron were able to use there size and scope to capitalize on it and now are among the biggest producers of not only oil but natural gas as well.

The next century will hold much prosperity for investors in these companies long term for the simple fact that no other group of companies in the world are better endowed than the Exxons & Chevrons of the world to capitalize on the opportunites that arrive in the energy sector!

lnt90

August 27, 2015

Replying to lnt90

Also, if your worry is about Chevron or R.D.S running out of oil than you need to monitor the reserve replacement ratios. ExxonMobil has the highest ratios and biggest reserves with over 16 years of it I believe. You wanna see that your refilling the reserves over 100% on a consistant basis, this means your running a sustainable operation long term. R.D.S. has had problems with this I believe, but still there fine, its just Exxon & Chevron are the best.

Joel

August 28, 2015

Replying to lnt90

How do you square this with the fact that 40% of oil production today is used by passenger vehicles. I see no good reason why oil use won't decline given the advent of cheaper and more efficient technology in the form of electric/batteries. We have lived for the past 50 years during a time of steady increases in oil consumption worldwide. What happens when/if it slows down?.. How do the oil majors respond?

I am sure there are second level thought approaches, but the idea that these businesses are "adaptable" to this situation just seems.. unlikely.. In a world where oil consumption declines, it would seem the economics of the business do too, except, perhaps for the top of the heap.. Exxon etc. But I'm not sure I can rely on that.

I want someone to prove me wrong, and I want the confidence to invest for 20+ years.

lnt90

August 28, 2015

Replying to Joel

The wonderful people at Exxon & Chevron already know this.

While smaller firms may not be able to adapt, the big boys I have 100% confidence will be able to deal with this.

They are able to offset the decline several ways. One is that over time they have gotten better at controlling costs and finding new and more efficient ways to get better yields at less cost. This includes refining and petrochemical integration and scale along with new processes of refining, drilling, etc at less cost which equals more profit. Even with NO growth or declining growth a 2-3% cost reduction for a firm with the size of Exxon or Chevron can result in hundreds of millions of dollars long term!!

Second, is growth markets. While Europe & the Americas are mature markets that are slow growing and in decline in several key areas in oil consumption you forget places like India, Africa, the Middle East, and Asia are still developing and will see very high energy demand. So over 20 years while American consumption may decline by 10-15% Asia will grow by DOUBLE alone. This is a big focus for the majors as they know the growth will come from these key regions especially Asia.

Finally while traditional gasoline use global is expected to AT BEST grow low single digits or decline even, the use of SPECIALTY fuels like diesel, jet fuel, natural gas and other niche fuel types are expected to increase which are MUCH MORE expensive (ex Natural Gas) and result in higher margins and thus WAY more profit, the downstream segments of the oil companies understand this and over the coming decades are already adding on to be able to meet this demand.

Finally as its already been said, if any new revolutionary substance came along rivaling the light bulb or Model T in change the majors would just buy up the competition. I would highly recommend looking at a 5 year history looking at ExxonMobils financials, the sheer magnitude of the numbers is jaw dropping.

Anything can happen in the future but think of all the changes that have happened since Standard Oil formed over 100 years ago. Yet The same companies continue to dominate. It's because of the sustainable competitive advantage the Major Sisters have had and will continue to have.

Joshua Kennon

August 28, 2015

Replying to lnt90

It makes me so happy to see someone refer to them as the "Sisters"; sort of took me by surprise. You don't really hear that anymore for obvious reasons now that they've mostly merged; at least not in the mainstream press (leaving aside the Financial Times attempting to dub a new generation of siblings). I wonder if people even know who the original Seven Sisters were or which firms now control them all. They held - what? - 85% or so of the entire world's oil reserves half a century ago.

I think it's because it takes me back to childhood when I was first learning all of this and throwing myself into it in a world before the Internet - library reference sections, copy machines, printed Value Line reports, biographies, old magazines and newspapers. When I was reading in the early to mid 1990's, almost everything came from the 1960's, 1970's, and 1980's (I still remember it being "normal" to see 6%, 7%, or 8% dividend yields on utility stocks in the historical quotes of the ValueLine reports!) Maybe it's watching the Peter Lynch clip I posted yesterday and how he was the major influence in my life that helped me discover, through his writings, what I wanted to do with my career.

joe pierson

August 28, 2015

Replying to Joel

Joel,

Oil companies were able to adapt to gas from oil because it is similar technology, solar and wind are completely different skillsets. Very few newspapers were able to adapt to the internet, even though it was just reporting news in a different way. I believe few of the oil companies will be able to adapt to solar or wind, the technology is completely different. Polaroid is still making instant cameras. Zenith (picture tube maker) was still saying fairly recently LCD TV's would never compete with tube TV's. Sears never adapted to online purchasing.

The basic problem is these large companies hang on too long to the old technology before it is too late, mainly because the senior engineers are skilled in the old technology, so they have zero incentive to change. That is my experience. When solar or wind will become practical I don't know, oil still has a long run.

Derek

August 29, 2015

Replying to joe pierson

You bring up a good point that many industry leaders have failed to successfully adapt to technological changes. One issue newspapers faced was that the barriers to enter their industry were so low. All that was required was a computer with internet access, a little know how for building a website, and employees to write content.

Large wind and solar developments are massively expensive and time consuming to build. The infrastructure to transport the energy to consumers is expensive and time consuming to build. The opportunity is there for these energy behemoths to move into leadership roles in developing these projects. The balance sheets provide an unrivaled amount of capital to develop these large projects, but there's no guarantee they will.

It's definitely worth some thought when thinking about the future of companies like XOM, BP, etc...

That said, I started a Direct Stock Purchase Plan with full dividend reinvestment in Exxon a couple months ago. I have no problem with the volatility of the industry, and oil is used for far more than most people realize. This slide in oil prices seemed like an opportune time to start building a position I hope to hold for decades.

LordSquidworth

August 29, 2015

Replying to Joel

I'm still not sold on batteries becoming viable on the large scale. The lack of range for these vehicles isn't a quick fix. The technology in batteries is pretty dated. The issue isn't so much man engineering them how they need them to work, but rather the inability for the materials at our disposal to hold enough of a charge.

Eric

September 6, 2015

Replying to LordSquidworth

Not only is battery technology improving at such a rapid pace, but there is more incentive than ever for it to happen. I'd be very worried about renewable energy technology if I were an oil shareholder

LordSquidworth

September 6, 2015

Replying to Eric

No... It isn't...

Battery technology progresses at 5% a year, while computing technology can double in 18 months. It's a slow moving sloth. New technology can take decades to reach commercial markets. The first battery (lead) was invent in 1859. Edison's battery idea took 40 years to get to market. The NiMh cell took 22 years, around the same for lithium.

The stuff you read about in labs is great... but putting it on a commercial scale is really, really difficult. On top of that, Lithium was the last of the "easy" metals. From here, it gets far more complex.

Eric

September 12, 2015

Replying to LordSquidworth

Look at all the companies scaling up their battery production - tesla, BYD, Foxconn, Apple, lg Chem, Samsung, and Panasonic. There's nothing wrong with lithium ion batteries and the demand for them is growing through the roof.

Jeff

August 27, 2015

I hear and understand the cyclic issues of oil, the psychological issues of seeing the stock drop, the amazing power of plowing dividends (or buybacks) back in during the lows. This all makes intuitive sense to me, and isn't new to anyone who has read your blog for a while.

One thing I *think* I'm getting from this article is that the oil majors' strategies (and temperament/culture) for dealing with these cycles is a major source of their competitive moats. I assume the other source is owning low cost oil fields / refining machinery. The brand name of Exxon has little value at the gas pump, so I know that isn't the moat.

I've been reading up on fracking, and seeing the estimates of companies like Granite Oil that indicate they are getting MUCH more oil out of the same well when they use injection techniques. They think they can sustain their dividend indefinitely at $50 / bbl. The giant jump in oil output in the US seems to support the concept that the supply part of the supply / demand curve has shifted in a major way.

I guess what I am trying to understand if "it is different this time" because of fracking and why/why not? On top of fracking affecting supply, we have a vast improvement in the *knowledge* of how to build more efficient homes and vehicles, even if we aren't creating them in bulk yet - putting what looks like a cap on demand. Not to mention we should expect solar power will continue to drop in price.

I am *sure* this is something you've looked into, and yet you don't mention it. I am wondering if the reason it might not matter that the supply/demand has changed could be that the supply/demand isn't the source of profit - handling the wacky market swings intelligently is.

lnt90

August 27, 2015

Replying to Jeff

The Moat's of the Supermajors are among the most incredible business structures I ever seen, as Joshua pointed out very well. Although I agree with the brand name recognition at the pump not having much effect in building a competitive advantage, I believe the names are very well used with Mobil 1 lubricants for consumers. I know MANY car enthusiast of all ages who will only stick with a certain brand, my family uses only Mobil 1.

OldManMase

August 27, 2015

Replying to Jeff

As far as the "cap on demand" that you mentioned, I am curious if this is true or will ever come to pass. Sure, things are being made that use energy more efficiently, but the total production of world energy is still set to increase rapidly over the coming decades, particularly in China, India, and other high growth nations. I wonder if the super-long term outlook however is a greater equilibrium between supply and demand, because the Earth's overall population growth is slowing.

Dheeraj

August 27, 2015

i want to climb on the tallest building in my city and scream "I LOVE IT !!!!!!!"

Dheeraj

August 27, 2015

typo phillips 66 not 66%

MODS please delete

FratMan

August 27, 2015

1.It is interesting that you did not include Kinder Morgan even though it has a higher market cap than Conoco as well as Phillips 66. Was it excluded because its business model is not that of an oil major, or because you deemed the company to be of inferior quality for inclusion on the potential generational holdings list?

2. Also, you mentioned that Exxon has become your fourth largest holding. For something to become a Top 5 or Top 10 holding in your portfolio, is there a quality standard that must be passed before you consider investing heavily into it? Are the candidates cut off to those 100 firms or so that seem likely to be making profits in 2050?

It's theoretically possible that a low-quality or mid-quality company could offer the best risk-adjusted returns out of any opportunity presented to you. For instance, if you woke up tomorrow and saw Alcoa at $0.50, would you put it in the Top 5 because it offered better risk-adjusted returns than Exxon? Or, because of its pitiful super long-term returns that would seem to imply an inevitable exit point, as well as the possibility of bankruptcy in an economic environment of historic difficulty, is it automatically excluded?

Joshua Kennon

August 27, 2015

Replying to FratMan

1. Yes (it was excluded because its business model is not that of an oil major; I wanted to keep it focused on one area given how long it already was and the different things that go into more specialized enterprises in the field). I also almost didn't include Conoco and Phillips 66 but I figured it hasn't been that long since they broke apart and you can effectively manually reassemble them buy purchasing them together as if they were a single stock.

2. Risk-adjusted returns are all I care about but if it is even close, quality always wins. Part of that risk adjustment is portfolio level, rather than issue-specific, so overall construction does play a role; seeing how different things change the risk profile of the pool of capital in totality. If I look at something and I think it's going to generate a good chance of [x] but a firm like Coca-Cola might bring in 85% of [x], I'm probably going to go with Coke because the odds are very, very good in the long-run, I'm going to have a better experience. Sometimes, I find nothing at all. The biggest investment I've been making prior to the ExxonMobil and, before that, Diageo positions: Cash. I love cash right now. It's wonderfully appealing to me. I want more. (I'm actually working on a post about portfolio cash levels for About.com that I hope hits the servers this evening. Update: It's published and you can read it here.)

Effectively, very little junk makes it into the portfolio because I often find myself asking, "If the stock market closed for the next 5 years, we went into a horrible recession, we had to live with the performance of the businesses as we hold them now, and we could make no changes - no deposits, no withdrawals - would I sleep well at night with what we currently have on the balance sheet?" If the answer is, "No", changes are made. In theory, there is a set of circumstances, a price, and terms, at which Alcoa could get added. It isn't particularly likely because of the standards I set. Aaron and I made some money trading in shares of an automobile manufacturer within recent years, for example. I wouldn't have wanted to own them forever, but I was comfortable the value far exceeded what we paid and there was little to no risk of bankruptcy. I made my parents a good chunk of change in a discount retailer that isn't particularly special because it was clear the thing was dumbly priced. Those things happen. I'm not selling the Hershey to fund them, though; at least not short of some life-altering set of circumstances. Even then, once you have these wonderful deferred tax benefits and such, I'd be more likely to try to come up with fresh funds and tap existing or future cash flows from the operating assets to pay for it.

If a wonderful asset came along at a great price and I could horizontally risk shift, which we've discussed, I'd do it. Let's say that ExxonMobil went to $120 tomorrow while crude still looked like it was going to be at $40 for whatever reason and Hershey were, again for whatever reason, at $68; a wonderful price that would have me doing cartwheels. Exxon isn't cheap at that point, on a present basis, anyway. Hershey would be. I'm going to shave off a touch of that Exxon position given that it's in a tax shelter, I can better balance the economic risks and growth profile, and I'll be happier with more Hershey. I don't really say that often because someone who doesn't know what they are doing won't treat it as a risk management strategy or, alternatively, a rebalancing opportunity but rather, try to time the market. It goes from being about intelligently adjusting the overall exposures and risks in the capital pool to, "Exxon went up and he sold it to buy Hershey, which went down" and gets dumbed down from there. I know it's not my responsibility to keep fools from being foolish but I'd prefer not to contribute to their misunderstanding by sidestepping the topic altogether. It's also, again, complicated by the fact I would prefer to find a way to come up with new money. Aaron doesn't like selling things. I have to justify any moves (and heaven knows I hardly do anything, anyway) so getting us to part with a business can be difficult unless there is some compelling reason.

I'm not sure if any of that made sense. Maybe someone else has discussed their thoughts already as I haven't had a chance to go back and pay attention to all of the comments over the past few days given how busy it's been around here.

Edit: My money is on the Labor Board ruling being destroyed somehow, someway, even if the powers that be have to spend billions to get it done. Despite the cries to the contrary, if it is allowed to remain, the franchise model is dead.

dave (nestle)

August 28, 2015

Replying to Joshua Kennon

"Cash, I love cash right now"

Me too, and I hope it loves me back.

Sean

August 31, 2015

Replying to FratMan

I think you missed the post where he said something along the lines of at no price and on no terms would I ever purchase Alcoa.

Joshua Kennon

September 1, 2015

Replying to Sean

In case I wasn't clear in the past (and if so, I apologize): I don't think the average investor has any business buying Alcoa at any price or on any terms. There's too much they might miss or too much that might go wrong. If I were to ever take a position, there is no way (at present returns on capital) it would ever be considered a permanent holding or something I'd want to own for long periods of time, but rather, a niche part of the portfolio exploiting price inefficiencies. In other words, it would be a trade - something I rarely discuss on this site or elsewhere as there is too much danger for the inexperienced to think they have a chance at doing some of the things we do - not an investment as usually defined.

For a firm like Alcoa to make it into the portfolio, it might be hard to appreciate the sort of disconnect from intrinsic value that would need to be present; you need to calibrate my personality and philosophy. I'm talking 1874, 1933, or 1973 - the ability to buy it for less than cash in the bank with almost no chance of bankruptcy and the enterprise itself being given to me for free. There'd have to be something very, very special going on that is outside of the bounds of ordinary capital market experience. If it's trading at something like 7x earnings when the stock market as a whole is at 15x earnings, I'm still not interested. You're going to do better over 25+ years owning Colgate-Palmolive at 20x earnings, instead.

Stated another way, I'm not interested in Alcoa on any price or terms as a permanent investment. If you told me I could have it at 3x earnings but I had to hold it for 100 years, I'd say, "No thank you". But if it were trading at such a valuation on cyclically-adjusted profit per share, there was little chance of dilution, I thought it was going to survive, and I was convinced an economic turnaround was on the horizon, I might use the common stock as a sort of leveraged speculative bet in leu of a call option as it would give a bigger margin of safety and allow me to not worry about the sudden-death risk of an expiration date.

Promptly forget that I said any of this. Pretend like Alcoa doesn't exist. You probably shouldn't buy it under any circumstances and I doubt very much I, myself, ever will, either. If it happens, I'll be as surprised as you.

Todd

September 1, 2015

Replying to Joshua Kennon

Joshua please don't talk about stocks to trade keep the blog centered on long term investing. My son who is a senior in high school came home today and told me that the smart kids get to be in a advance class on investing in stocks it is 8 weeks long. One of his friends is going to be in it and he told my son they pick stock and see how well the do in the 8 week course. I told him what a joke they are setting those kids up to be traders not long term investors. My son already own stock K,PEP, Kraft, UN, KO. and he in not smart enough to be in the class. What Bull Crap. He probly know more than the teacher. I hate it when all the smart kid get the breaks.

lnt90

August 27, 2015

Excellent post as always!!

The one other thing I would mention as well is the reinvestment effect is startling with the oil stocks like Chevron. Because they chronically sell for VERY low multiples (8 to 11) this means your dividends are buying shares at a low price and you get a amplified compounding effect. Royal Dutch Shell is an excellent example as well, though ExxonMobil is one of my top 5 companies easily to buy and never sell EVER just because the quality of it is impeccable. (KO, GE ,PG & JNJ would be the other 4)

Mike

August 28, 2015

On the topic of preferring to acquire new holdings with fresh cash rather than selling your least favorite good business at the time, I had a question I was hoping you could help me think through. You often mention cash generators and their importance in an investment program when it comes to taking advantage of down market opportunities as well simply making it easier to stay the course of dollar cost averaging.

For example, an investor relying on their labor income to dollar cost average without large capital reserves may find that the time he could take advantage of the market the most is the same period of time where his labor income could be jeopardized (say....recessions and job loss) and the whole plan could be placed on hold. The requirements of following a dollar cost averaging plan seem to be at greatest risk when relying on one's own labor. Of course, this calculation will depend on the security one feels they have with their job or business and its risk relationship to economic downturns. Essentially, it appears that having a secure cash generator massively helps in staying the course of an investment program. It would be interesting to see the results of dollar cost averaging when investment does not occur in the harshest down periods.

Having said this, my question has to do with overall investment strategy. Say an individual has just inherited 500,000 to place in investment operations and has the tolerance withstand vicissitudes of the stock market as well as the competence to buy and oversee relatively simple kinds of real estate. And, say that at the current asset values one could achieve an 8% yield on the real estate and a 2.5% yield on an index fund.

1. Do you think that an approach which acquires a higher yielding asset as the initial cash generator, which then reinvests everything into an index fund (40k/year) would outperform simply acquiring the 500k index fund within that first year and letting it compound on itself(dividends reinvested in both approaches) over a 40 year period? (I need to find some good data on lump sum investing results)

As I'm reading this, I realize it's kind of convoluted, but I feel like the higher yielding cash generator option would be a more effective choice depending on the individuals' opportunity cost. Of course, there are many risks that need to be accounted for depending on what that cash generator is. I realize now that I prefer the higher yielding cash generator approach because it allows me to redirect the cash flow in case anything interesting comes up. And hence, the risk would also be not following through with the plan to dollar cost average into the index. I just think the cash generator approach offers much more utility (backup liquidity) and optionality, but it has its risks (behavioral and diversification) as well.

As a side note, I think some of the studies you have done on oil companies (chevron and one other a while back) demonstrated the power of high yield reinvestment. Of course, one has to be careful making any kind of recommendations since high yields can be a mirage. That's why you go outside financial assets to get the yield where your skill and time pay, in essence, for that yield to be true. In other words, the general efficiency of financial markets (passive investments, no opportunity cost differential) bake in the higher risk for that false yield whereas you can often find true higher yielding assets outside of financial markets where the time component required to manage the active investment allows for arbitrage of sorts by those with lower opportunity costs. p.s., forgive me if my economics are dodgy...

Thanks for any insight in advance. I'll be looking out for your portfolio cash article as well.

Kapitalust

August 28, 2015

Replying to Mike

Our "poor man's" version is to hold a substantial amount of liquid cash that is not meant for investment and direct the cash flow from labor activity to business ownership. We first built up a really large cash holdings for a couple years, then proceeded to start buying fractional ownership in businesses.

That initial cash pile sits there, earning ~2% interest, and gives us the satisfaction of knowing that even if both of us lost our jobs in an unlikely scenario and our labor cash flow dried up, it wouldn't even matter. We'd have living expenses covered for 1-2 years (depending on how extremely we wanted to cut down our lifestyle).

Eventually, there will be some significant cash generator (like you speak of) to create cash flow exclusively for investment opportunities, and the holy grail is to create a virtuous loop of investments creating cash flow to re-invest, ad infinitum.

For now, until we build the substantial cash generator - which will take years - the substantial cash holdings do a fine "poor man's" job of staying the course no matter the conditions in the markets.

dave (nestle)

August 28, 2015

Replying to Kapitalust

I agree with the cash hoard of actual years worth of living expenses. It always shocked me that most books or "experts" recommend only 3 to six month's (or 9 months if you are lucky), as the ultimate savior "in case of". Now maybe I have an extreme opinion, but covering yourself for 3 to 5 years seems way more foolproof. (no matter how hard the accumulation of the cash is, if you need it, I'm sure you would be happy that you had it)

#patienceanddiscipline

Adam @ AdamChudy.com

August 28, 2015

Replying to dave (nestle)

Agreed but if you tell someone with no savings to aim for 3-5 years that's just hopeless. Getting people to 6 months, which should cover a car or basic home repair, small medical bill, or temporarily job loss, is a huge step up from where 90% of people are.

DP @ Someday Extraordinary

August 28, 2015

This article is awesome! At the moment, I'm staying away from the oil majors, for exactly some of the reasons you state. I'm not going to try to predict oil's moves. However, I think some value is to be had on the outskirts of the industry like a McDermott (MDR), who is an engineering and construction company who builds for the majors. The majors won't stop pumping oil - ever- so an MDR won't run out of business. However, it can mistakenly trade with the industry due to association as it has this year - well, that and they are working on a turnaround. Once investors realize they are still making money in this environment, it should play out nicely.

I recently wrote on my page about cycles and how the economic cycle tends to lag the market cycle. This is why I like the top down approach. As you mention, the investment in the big oil companies depends entirely on where they are in the cycle.

Again, great article! Keep it up!

-DP

stegner

August 28, 2015

Hi guys, I'm not much keen on trying to catch the falling knife presently, but this article has piqued my interest in the Oil Majors, who I know nothing about. Can anybody recommend some good foundational texts to get me familiar with the industry dynamics of the majors? I recently put Oil 101 by Morgan Downey on my to read list, is this a good place to start? I'm especially interested in the qualitative dynamics surrounding the majors, but quantitative stuff (i.e.: how to interpret the financials) is also welcome.

Any guidance would be most appreciated.

stegner

August 28, 2015

Replying to stegner

Ps. Thank you as always Joshua, too. The more financial stuff I read, the more I appreciate your viewpoint.

Adam @ AdamChudy.com

August 28, 2015

As someone who works in the oil industry, my salary, net worth, and home (I live in Houston) are closely tied to the industry. Everybody here knows when the prices go bust, you batten down the hatches, don't sell, and wait for prices to come back when the system has worked out the glut.

I've heard a lot of people describe investing in commodity businesses, but this may be the best laid out explanation yet.

dave (nestle)

August 29, 2015

Replying to Adam @ AdamChudy.com

Looking to buy a Texas ranch, anyone jumping in front of trains over there yet? (just kidding, I feel bad)

Yeah, I take a simplistic approach to energy stocks myself. I am not a perfect analyzer of all the aspects of big oil. I make judgments and personal forecasts and add shares when I deem appropriate. I don't even play games with capital tax losses with these stocks. Just hold and add. Maybe sell some when I sense overvalue and/or commodity price hype. I do hate seeing red though, but now it makes me stronger and calmer. (proper reserves and liquidity, built up over a couple decades, keep me grounded)

Adam @ AdamChudy.com

August 29, 2015

Replying to dave (nestle)

I do the same, though a lot my shares come via work. I've deployed a good bit of capital in this downturn, largely in to the majors. I probably have some insight in to the better smaller players that could outperform, but the risk is that prices stay low and they don't have the balance sheets for multi-year sub-$50 oil prices. I'll happily keep adding to my Conoco, Chevron, Shell, BP and Exxon stakes.

ImperatorMachinarum

August 31, 2015

I read the article and most of the comments. Very informative. Thanks for all the contributions.

I too try to keep investing simple. I'm especially a value investor. I try to buy strong companies at compelling values. I'm extra careful to avoid a falling knife.

I'm convinced oil and gas in general are not falling knives in the longer term. They're not going out of business. Some North American companies might go out of business due to the current price war. But the majors and the stronger smaller companies will survive and thrive. Suffice it to say, I believe North American capital liquidity, labor elasticity, technology, and supply chain optimization will allow us to outlast undemocratic nations with sovereign funds that depend on 1 commodity.

I own AWK, CBI, DNOW, DOW, DVN, NOV, RDS-A, RDS-B, TRN, and XOM. I bought all at value, some years ago, some last week. That's standing me on good stead overall, even if some of these individually are down near 40%. Fortunately some are up 100%.

I'm well diversified beyond energy, heeding warnings about staying solvent during market irrationality. I keep reinvesting dividends. I'm patiently waiting for oil prices to normalize, achieving my goal of comparatively beating the S&P500.

If oil dips to $30 or stabilizes, whichever comes 1st, I'll buy more stocks in the sector. I really believe value opportunities like this don't come often. So I'm doing my best to buy low. Fingers crossed.