It’s time we talk about the debt ceiling and what a debt ceiling default would mean for the United States. I’ve avoided this conversation because I was hopeful we would never end up here, again, after the last round of stupidity. I’ve also avoided discussing the on-going shutdown of the Federal Government, despite some strong implorations from those of you who have written through the contact form asking me to share my thoughts on it. The shutdown will have to be put off for another day because it pales in comparisons to the implications of a debt ceiling breach, which you need to understand. Even if you don’t own a single asset, it holds the potential devastate your life in a way few other events can.

[mainbodyad]Before I can explain to you what the debt ceiling is, why it is important, and what Congress is threatening to do, I need to provide a bit of back explanation about the process for spending money in the Federal Government. For those of you who already know this, it will be old hat, but some folks might need a refresher in high school civics, or live outside the country and not be aware of how the system is designed.

Before We Get Into the Debt Ceiling, You Need to Understand How the Federal Government Spends Money

The United States legislature is split into two parts. When talking about them, together, it is referred to as “Congress”:

- The House of Representatives – Consists of 435 elected representatives voted into office by local districts throughout the country, allocated based on population. Each representative is elected for a term of 2 years, meaning the United States people can, in a real sense, elect to overthrow their government every 24 months if they wish, starting over from scratch, if the political will is there to accomplish it. States with large populations, like California and New York, have many more representatives.

- The Senate – Consists of 100 elected representatives, with each State in the Union receiving 2 Senators, regardless of population. Senators are elected for a term of 6 years, are meant to provide stability and serve as “the cooling saucer” of the Republic. It is the place the founders intended for legislation to go to die, so no radical changes could happen overnight.

These two parts of the legislature, each forming their own body with their own rules and terms, work in the U.S. Capitol building.

The United States Congress works in this building. The House of Representatives has one wing and the Senate has the other wing.

For a bill to become law, both the House and the Senate must pass identical versions of it, and then send it to the President of the United States, who is elected to a term of 4 years. If the President vetoes the bill, it goes back to Congress, where it either dies, or gets a new vote. If the new vote results in 2/3rds of both the House and Senate supporting the bill, the President’s veto is overridden and the bill becomes law. Historically, less than 10% of all Presidential vetoes are successfully overridden by the legislature. This was also by design, as a proposal must be very popular to garner that kind of support.

If the President signs the bill, it becomes a law. Otherwise, it goes back to Congress, which can override him with a 2/3rds majority vote of both the House and the Senate. Historically, less than 10% of vetoed bills are passed into law this way.

If a person or company believes the new law violates his/her/its Constitutional rights, the law goes through a process that I’ve already described, ultimately ending up in the Supreme Court, which has the power to strike it down, in whole or part. The judges are supposed to provide the most stability, taking the long-view. They are nominated by the President, and appointed by the Senate, to lifetime terms. They will only vacate their bench if they die, are removed by the legislature through the impeachment process, or resign. Their primary job is to hear cases in which legal and constitutional disputes are raised, and make binding decisions.

If a law is unconstitutional, it will end up in front of the United States Supreme Court, which has the power to strike it down in whole or part. Their job is to protect the Constitution from overreaching governmental power and resolve constitutional conflicts between lower courts.

The founders knew that Congress would be prone to overspend, so it gave the House of Representatives a special power. It said that all laws requiring money have to start in the House, then go over to the Senate. This way, the legislature couldn’t bankrupt the country without the people’s consent as they can throw everyone out every two years. They also knew that the House would be prone to short-term thinking, so they gave the Senate the power to appoint, upon the President’s nomination, ambassadors and judges, as well as approve sovereign treaties with other nations.

The Process After Congress Authorizes the Spending of Money

Imagine that the House of Representatives passes a bill authorizing the spending of money. It then goes to the Senate. It passes there, and gets sent to the President. He signs it. It becomes law. The money is now legally authorized and the United States is on the hook for it.

The United States Treasury Department is sort of like the cash manager in the background who has to make sure all of the funds are ready and available to be used. It works with the IRS to have people’s taxes deposited into an account it can access. When Congress spends more cash than the government brings in through taxes and other sources, the amount of the shortfall (called “the deficit”) is raised by the Treasury going to investors and issuing I.O.U.’s in the form of bills, bonds, and notes. This even includes your humble savings bonds! Just as when you use a credit card to cover a deficit in your own life, the amount gets added to your overall debt figures. When you begin running surpluses, again, you pay off that debt. Meanwhile, you pay interest.

United States Treasury Department in Washington, D.C. has to make sure the cash is where it needs to be when Congress authorizes spending.

Investors often feel very safe with these bonds because the 14th Amendment of the Constitution states, “The validity of the public debt of the United States, authorized by law, including debts incurred for payment of pensions and bounties for services in suppressing insurrection or rebellion, shall not be questioned.” That means the entire taxing power of the United States Government is behind those bonds and that the government does not have the constitutional authority to default.

When a bond is issued, the Treasury takes the cash from the investor, adds it to the cash raised from taxes, and makes sure it is sent to the places that Congress authorized in its laws. If $100 million goes to this national park, or $10 billion goes to weapons systems from the military, the Treasury gets the money into the accounts of the Department of the Interior, overseeing the park service, or the Department of Defense, overseeing the branches of the military, who then use their own internal accountants to allocate as they are authorized to by law.

Of course, the Treasury Department has to keep track of all of this debt because it needs to make sure the interest payments are sent to investors. Whenever it issues a new bond, it adds the figure to the national debt so Congress and the President know how much needs to be repaid or refinanced in the future. (There is actually another department that tracks all of this, but I’m keeping it simple so you get the basics.)

What Interest Rate Does the Treasury Department Set on the Treasury Bonds It Issues?

What interest rate does the Treasury Department pay? It’s set by auction. Although the Federal Reserve can attempt to manipulate this in the short-run to help ease the pain of recessions or depressions, or suppress inflation when it gets out of control, over the long-term, the interest rate on the Treasury bonds is set by the price investors are willing to bid when they place orders to buy bonds. That means if a lot of investors are demanding bonds, the interest rate is set lower. If fewer investors want the bonds, the Treasury has to raise the interest rate to attract more money. You can see the current Treasury bond rates updated daily.

(Side story: For more than 200 years, up until a decade or two ago, in fact, the entire United States Treasury bond process was handled by a handful of “authorized dealers” on Wall Street, which aggregated orders from countless individuals, brokerage houses, and other financial institutions, then wrote their overall order on a slip of paper and dropped the bid for Treasury bonds into a little wooden box. The Treasury officials then opened the box, added up the results of the auction, issued the bonds, and took the cash from the dealers to move to the government’s account. The dealers would divvy up the bonds it had been issued to the various investors on whose behalf it had been bidding, and make a nice little profit on this activity, though it was mostly about the prestige as it made it easier to be taken seriously in the investment banking industry. It was so old-school, it was beautiful. Back before electronic deposits were possible, all of this movement was facilitated, in part, by the use of $100,000 bills that the Federal Reserve system would move between its member banks as capital was transferred in the system. Today, this bill would have an inflation-adjusted value equal to around $1,745,351. Now, back to the regularly scheduled program and discussion of the debt ceiling.)

Ordinarily, the Treasury gets very good rates on its money. The lower the interest rate is pays, the better for taxpayers because it’s less cash that gets added to the national debt. How can the Treasury borrow so cheaply? It is because Treasury bills, bonds, and notes are considered the safest fixed income asset in the world due to the fact the United States controls $217,623,159,381,449 of the world’s $707,726,307,170,996 in assets (the latest figures available are from 2005; if you are interested in seeing the breakdown yourself, go to The World Bank – The Changing Wealth of Nations resource and download the Wealth of Nations (XLS 655KB) excel spreadsheet in the right hand column. It is so specific, it even gets into estimated natural gas, coal, and timber reserves), despite having only 5% of the global population. We hold a vastly disproportionate amount of wealth, most of which was created due to human capital as our economic system and free society rewards innovation. It’s not that we’re perfect – it’s just that many other places on the planet actively suppress and destroy their own human capital. How, after all, can a country expect to compete with us when they stone rape victims or imprison free thinkers? When they indoctrinate rather than educate? It’s not hard to win against someone who is willingly destroying their own best chance at progress.

If everything falls apart, the taxing power behind the Treasury is enormous, so it is highly likely that investors will be repaid, especially given the Constitutional assurance that the debt must be honored.

Nearly Every Asset Is Tied, Directly or Indirectly, To Treasury Bond Yields

This means that nearly every asset in the world, and certainly every asset in the United States, is tied either directly or indirectly to the Treasury bond rate. It sets the opportunity cost. It is the rate at which you could park your money, do nothing, and earn x% on your money. If Treasury bond rates increase, then stocks and old bonds will decrease so they offer higher earnings yields and interest yields to compete with the new, more lucrative Treasury bonds. If Treasury bond rates decrease, then stocks and old bonds will increase because they are now more attractive than Treasury bonds, so rational investors move their money. It’s basic mathematics.

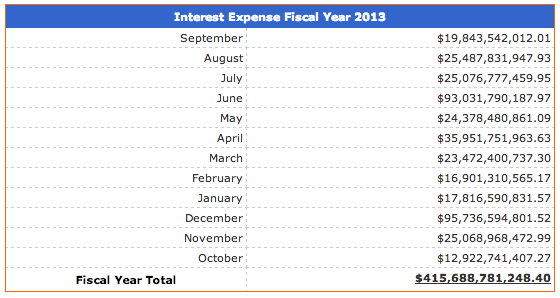

Even with low rates, though, more debt means more interest. In the past 12 months, the Treasury has had to pay $415,688,781,248.40 in interest to its bond investors. That is $415+ billion that could have been used for education, infrastructure, defense, health care, tax breaks, anti-poverty programs, scientific research projects, and any number of other things.

Many of you out there are probably thinking, “Uh … we are living at the lowest interest rates in history, so what happens when all of that debt needs to be refinanced? Even if the budget were balanced, when rates inevitably increase, doesn’t that mean there are going to have to be massive tax increases or huge cuts to entitlement programs unless the population increases significantly to offset the much higher interest expense?”

Ding, ding, ding! Congratulations! You’re exactly right. The people in Washington know this so they are taking a diversified approach. One involves making immigration much easier, to bring in far more foreigners and make them citizens.

Another involves working to actively lengthen the outstanding maturity of Treasury bills, bonds, and notes so those low rates are locked in for a very long time. Sadly, that won’t save us. It would buy a little bit of time, but not nearly enough. The weighted average maturity of U.S. Treasury debt over the past 30+ years has been around 58 months. That means, were interest rates to skyrocket, the costs would begin showing up in the national budget over 4-5 years as the old bonds came up for refinancing and investors demanded much higher rates to part with their money. In fact, the Treasury keeps detailed maturity profiles in nice, informative, colorful charts to keep tabs on its cash flow needs.

What Does All Of This Have To Do With The Debt Ceiling?

Glad you asked. When a bill becomes law, and the money is authorized to be spent, the Treasury Department has to come up with the money by issuing bills, bonds, and notes and combining it with tax revenue. That much you already know. However, Congress, as insane as it sounds, decided to add a second procedure, where it had to pass a law authorizing the Treasury to pay the bills that it already legally owed! This second step where it gives the Treasury the authority to pay bills the U.S. has already incurred and the Treasury has been ordered to pay, is called “raising the debt ceiling”.

Do you see the problem?

The Treasury Department is issuing bonds to raise cash for spending that Congress already approved and to pay interest on Treasury bonds that are already outstanding and in the hands of investors.

In a functioning democratic republic, this should not be a problem because Congress would be rational. And it wasn’t until back in 2009, when a group of Democrats used the debt ceiling as a negotiating tactic. It was a dangerous precedent. Now, a faction of the Republican Party, which holds a majority of the seats within the House of Representatives, convinced the leadership of the House, which controls the flow of legislation, to threaten to refuse to extend the debt ceiling if the Senate and the President don’t agree to their demands on future spending legislation.

It’s the political equivalent of saying you think your child shouldn’t be playing with guns so if the other parent doesn’t restrict access to firearms, you’re going to blow the kid’s brains out in retaliation. It is insanity. Everybody loses. There is no salvaging it. The “cure” is worse than the disease.

What Might Happen If The Debt Ceiling Is Breached?

If any group in Congress is ever successful at causing a default (meaning the Treasury isn’t able to pay its bills when they are due), and investors lose faith in the ability or willingness of the Federal Government to honor its obligations, there is a very good chance that:

- The deficit will skyrocket

- The national debt will explode

- Widespread panic and unemployment will result

- The economy would go off a cliff

That may seem a bit odd, at first, if you don’t understand economics. How could refusing to pay the bills that are owed increase the debt? It’s not like a student loan, where you have penalties. What gives?

Let me walk you through the process.

When You Are a Bad Risk, Your Interest Rate Increases Because People Demand More Compensation Before They’ll Lend You Cash

Imagine what would happen if millions of investors, covering trillions of aggregate maturities, suddenly found out that the safest asset on the planet defaulted. The interest that was supposed to be deposited into their brokerage accounts, bank accounts, or accrued on their fixed income securities was suddenly not there. Even if you don’t think you own Treasury bills, bonds, and notes, you do. It represents the cash reserves of nearly every major corporation in the S&P 500 as well as most major mutual funds. It makes up part of your pension plan that sends you checks every month. The Treasury makes sure your Social Security payments get sent (side note: For political reasons, I have a sneaking suspicion that were a debt ceiling default to happen, the Treasury would prioritize its cash outflows and honor Social Security payments above all others to avoid political unrest. Payroll taxes alone should be sufficient to cover current benefits. If it doesn’t, it would accelerate the economic collapse as most Social Security money is spent quickly by retirees on things like food, shelter, and medical expenses, going right back into the economy. The problem? This isn’t legal. The Treasury has no authority to decide that it can honor certain bills and not others. And even if it were allowed, the Treasury Department doesn’t have the technology to handle it as it pays each bill due on a first-come, first-serve basis. Meanwhile, credit rating agency Moody’s, on the other hand, insists it will happen based on what appears to be blind faith).

[mainbodyad]Panic will ensue. Frightened investors, particularly retirees, will sell off their Treasury bonds, driving the price down and the interest rates through the roof. When the crisis does pass, the Treasury will be unable to borrow at low rates as investors won’t trust them, anymore. (To illustrate: A Treasury bond paying $5 in interest selling for $100 will yield 5%, but if investors panic and drive it down to $50, it’s now yielding 10%. That means if the Treasury wants to refinance at maturity or raise new money in the future, it will be competing with its own, old bonds, and have to issue them at 10%.)

Even worse, this will likely ripple through the banking system. Insurance companies would go bankrupt as their risk-adjusted capital ratios would crumble. ATMs would likely run out of money. Banks would probably have to close for extended periods of time. Workers would not get their paychecks. The secondary cash equivalents markets, such as commercial paper, would begin drying up overnight. And, unfortunately, given that the entire global monetary system is built on Treasury bills, bonds, and notes, the effects, globally, would be swift. It wouldn’t take long for it to show up in London, Tokyo, Paris, Berlin, Beijing, Bern, Ottawa, and everywhere else.

So at the very same time the Treasury faced rapidly escalating interest rates on the debt, the economy would be collapsing and generating less tax receipts. It would be brutal.

Most profoundly, I doubt any of the other major global economies would trust the U.S. dollar again, meaning they would setup other reserve currencies, taking away a significant competitive advantage we have.

Given the Damage It Would Cause, Why Would a Person Support Not Raising the Debt Ceiling?

So we know the consequences of allowing a debt ceiling default, insofar as it can be projected. It would radically increase the deficit, add to the national debt, result in widespread unemployment, hurt the United States competitively for generations, and bankrupt millions of families who don’t even realize how tied their fortunes are to the Treasury bond (car dealers, construction workers, electricians, restaurants, theme park operators, etc.).

How, then, can anyone advocate for allowing it to actually happen? There are only two reasons:

- They are literally too dumb or ignorant to know how the financial system works

- They have a death wish for the United States and want to see it fail

That’s it. There is no other rational explanation for what amounts to economic suicide, which is precisely what it is. (It seems necessary to clarify that most members of Congress who have in the past, or are in the present, engaging in this bad behavior do not, in fact, advocate for actual default. They are posturing to attempt to win political points with no plans of carrying through on their threats as they understand the devastation it would cause. Politicians vote against raising it all the time as a symbolic measure, knowing full well it has the votes to pass. Even Obama himself did this during his time in the Senate! Unfortunately, there is a significant minority of Americans who do not realize this. They actually believe going into default would be a good thing for the country. Last month, a Wall Street Journal poll indicated that 44 out of 100 Americans opposed raising the debt ceiling!)

Emergency Measures Would Have To Be Taken to Prevent the Debt Ceiling from Being Breached

Under no condition can the United States Government be permitted to default. There is some serious discussion about whether the Treasury could simply ignore Congress and the law given the constitutional requirement to honor the debt. There is also a much easier, and less aggressive, work-around that the Obama administration reportedly rejected, but I think would return to the table almost instantly if a real default were on the horizon, which involves minting a couple of trillion-dollar platinum coins and having the mint, using the expanded monetary base which wouldn’t require Congressional authorities, deposit it directly with the Treasury, which could then use the money to get through the crisis.

It Might Be Okay If Investors Thought the Default Was Temporary and Political, Not Financial

The upshot? Warren Buffett has a very good point: If the default lasts for a very short amount of time, and people in the market believe it is entirely due to stupidity that will be rectified shortly, they may remain rational and prevent the whole thing from melting down by pretending like it’s all okay until it actually is all okay.

In other words: We don’t have a clue given the present variables on the table. The only thing that is for certain is it’s a stupid, non-necessary risk taken entirely for political reasons that the American people should consider inexcusable.

That’s what makes it so terrifying to people who understand economics. We can guess all day, just as we could as to the exact implications of hurling a steel basketball into a jet turbine during flight, but the actual results are not knowable until they happen. At which point it’s too late.

Reader Comments (60)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Michael

October 7, 2013

In my estimation the problem we have, which the Republicans are seeking to rectify, is we are spending more than we are taking in. When this is the case we must make cuts to right the ship - this is what the Republicans are trying to communicate to the Democrats. We cannot continue spending more than we bring in unless we are going to print money (which is what we are doing now). This is personal finance 101 - I would doubt many of these members of Congress are doing this personally (spending more than they are making) even though they are doing it with the finances of our country.

Just as ludicrous as defaulting on our debt payments is approving a national credit card with no limit. By the way your 2 reasons why Republicans would do this (they are ignorant of how the financial system works or they want the country to fail) are straw men attacks at best and ad hominem attacks at worst. These representatives are highly educated and supported by brilliant economists who know the dynamics far better than you or I. To question their loyalty to the country and it's success is sad.

BubbaD1

October 7, 2013

Replying to Michael

Joshua didn't specifically say those two reasons were to blame solely on the Republican Party.

Joshua Kennon

October 7, 2013

Replying to Michael

And I agree with that. I want to see the United States government balance its budget. But it's not true that the American people as a whole do. The citizens of the United States - we - overthrow our government every 24 months and re-elect the House of Representatives, where all spending bills start must originate as per the Constitution. Congress continues to spend more than is brought in on the tax receipt side. And the people keep re-electing them.

We can say that Americans want change, but actions speak louder than words. Americans that keep putting the same people back into the same positions of power over and over and over and over and over again to repeat the same behavior. They don't. They talk about it, but they aren't willing to accept the sacrifices necessary to make it happen and both parties are just as guilty.

The problem I have with the threat to refuse to raise the debt ceiling is two-fold:

1. It is blatantly unconstitutional for the United States Congress to attempt to prevent the Treasury Department from honoring the debts that have been incurred already through lawful legislation. It's right there, in black and white, crystal clear in Amendment XIV. "The validity of the public debt of the United States, authorized by law, including debts incurred for payment of pensions and bounties for services in suppressing insurrection or rebellion, shall not be questioned."

The bills that the Treasury must pay was already authorized by law. Issuing the bonds to cover it is simple the paperwork mechanism necessary to come up with the cash as the legal obligation for the debt already exists.

Perhaps it's exhaustion over the extend of the NSA spying scandal, but I'm tired of Congress acting like their isn't a damned Constitution and they can do whatever they want. They can't. It supersedes even their authority and can only be changed by the amendment process.

A government shutdown, no matter how painful or unpopular, is at least constitutional. It's a legitimate exercise of the power of the purse strings held by the House. A refusal to raise the debt ceiling is not as the entire notion of the debt ceiling is redundant once expenditures have been legalized.

2. The proposed solution would likely lead to a radical increase in the cost of the national debt, resulting in bigger deficits and more debt. As I said elsewhere in another comment response, it's like saying, "I need to lose weight, so I'm going to eat this double layer chocolate cake if you don't take me to the gym right now!" It's fiscal insanity.

P.S. I never mentioned the Republican party in the section referencing the two most common reasons a person would advocate for actual default (not posturing like part of the Republican caucus in the House is at the moment). You can re-read it. It's not there. You assumed I felt that way, which I don't. The people about whom I was thinking in my own life advocating that the Congress go through with this action aren't, in fact, Republicans at all. Most of them are independent.

However, I do believe that you are giving far too much reverence to the authority of the office of Congress, Republican or otherwise, and to their general intelligence. Some members are quite brilliant. There are a few I admire greatly. Some are not. I use a certain professional service that is also used by a member of the United States House of Representatives that I won't name out of self interest. This person is an absolute idiot. They believe that demons are attempting to take over the country and that things like focusing on stem cell research are a way for Satan to turn the nation away from God under the guise of saving babies and healing disease. And that dinosaurs didn't exist (they were planted in the ground to deceive us all). You'll see this person on CPSAN all the time and their handlers do a good job of controlling the message so it's hardly ever in the news unless you look closely, but they are nuts. Absolutely nuts. Their grasp of economic knowledge is less than a randomly selected, retired member of the general public. I would suggest, respectfully, that you're letting the halo of the office mantel of authority cloud your assessment of their skill set.

Chris

October 15, 2013

Replying to Joshua Kennon

It doesn't matter which side you choose. There's no accountability. The congressman will do what they want for their term (or more if re-elected), and then will go work on K Street as a lobbyist and make a lot more money manipulating bills to benefit whichever lobbying group they work for.

JD Arney

October 7, 2013

Replying to Michael

Our government and its spending has pretty much zero relation to personal finance. I can't mint money to pay my AmEx bill, I don't have a standing army, AmEx won't take an IOU from me, and there's probably dozens of other reasons why it's not at all the same thing. This is the biggest straw man of all in these discussions. Our government has been in debt for about 99% of its existence. The debt to GDP ratio is probably too high right now - an improved economy would take care of that. Job creation and economic improvement should be the #1 priorities of Congress right now for that reason, but a faction of the Republican party (not the entire thing) would rather blow it all up and see what happens.

Lord Squidworth

October 8, 2013

Replying to JD Arney

"but a faction of the Republican party (not the entire thing) would rather blow it all up and see what happens."

at the same time their attempts at doing so create a drag on job creation and economic improvement.

Anon

October 8, 2013

Replying to Michael

People! This is very, very simple.

The demographics in this country are shifting (and said demographics want more entitlements--> more debt), such that the chances of Republicans getting elected will be less each year (and less Republicans means less moderating of Democratic giveaways).

Republicans are heading towards extinction because our nation is gradually producing more leeches than hard-working citizens and because Republicans have been running candidates with the wrong faces/personalities and wrong colors/races.

Republicans have no choice but to threaten Armageddon (which is their right), since they have less support than Democrats (if you're familiar with children and parenting, this isn't rocket science). Republicans are trying to save the nation from itself.

Scott McCarthy

October 8, 2013

Replying to Anon

You do realize that Republicans actually won the majority of federal elections in 2012, right...?

TheLonelyHumanist

October 10, 2013

Replying to Scott McCarthy

Funny how they did that with a minority of the popular vote... How do you do that? It helps if you know where all the black neighborhoods are: https://maps.google.com/maps/ms?msid=206285371130967586335.0004ce10c515dee004949&msa=0

Scott McCarthy

October 10, 2013

Replying to TheLonelyHumanist

And if this country was a democracy, the popular vote would matter; but this is a republic. Turns out winning state legislature elections in census years is important - who knew?

But don't pretend the gerrymandering is any more egregious in Red states than Blue ones.

TheLonelyHumanist

October 10, 2013

Replying to Scott McCarthy

Then how is pointing out that Republicans won more elections an argument against Anon's comment? Your countering your own argument.

Scott McCarthy

October 10, 2013

Replying to TheLonelyHumanist

Anon said that the odds of Republicans being elected was rapidly declining due to demographic shifts (because immigrants coming here from economically disadvantaged countries is new I guess...?). I pointed out that empirical evidence suggests the GOP continues to win a majority of elections, anyway. In a republic, it's the number of seats that you control that matters - the aggregate votes is irrelevant.

Lord Squidworth

October 8, 2013

Replying to Michael

These representatives are highly educated and supported by brilliant

economists who know the dynamics far better than you or I. To question

their loyalty to the country and it's success is sad.

Funny thing is... Most of my economics teachers had the exact opposite to say about politicians in general. Even with the "brilliant economists" they are supported by, many of whom were leaders in causing the messes we face today.

Richard Garand

October 7, 2013

The last part is interesting - when the credit rating on US debt was cut a couple of years ago, investors got scared and bought more US debt. I don't think we can entirely rule out a repeat of that if there is a default.

Joshua Kennon

October 7, 2013

Replying to Richard Garand

It could happen but I would be shocked to see the same action in Treasury bonds repeated, though, because when they were driven up to negative rates, investors were essentially buying insurance against collapse as the biggest financial institutions in the world imploded. A small negative rate on the fixed income securities was economically similar to buying a catastrophe policy to cover your family farm.

If the Treasury bonds themselves weren't paying interest, the entire motivation that resulted in them being driven up the last time would cease to exist. What would fill the void? I haven't a clue. I have a sneaking suspicion you'd see a run to sovereign debts or other high grade fixed income securities issued in or by Canada and Switzerland, among other nations. Of course, that's only a guess. It would be unprecedented. I suppose, at least, we could grab the popcorn as a real-world soap opera played out on the global stage.

Richard Garand

October 8, 2013

Replying to Joshua Kennon

I think the negative rate you mentioned is the key. You buy something bad when everything else is worse and given the wide-ranging effects that could be the case. It's also possible that investors would turn to other issuers with much smaller markets and saturate those, maybe leading to double-digit negative interest rates. Outside of those markets I'm sure there would be a lot of extremely cheap assets available to pick up.

bodegha

October 7, 2013

Joshua, I'm just an average person- so this may be simplistic. But how many times have we raised the limit, only to come to this position again? Calamity is what the smart people tell us will happen, yet they are the ones who have us $17 trillion in debt (there is a number of even smarter people who say the real debt is $83 trillion). Something you would never advocate your readers to do. You would call us idiots for maxing out our BOA card, and then ask to raise our limit. They are 'Chicken Littles' running around telling us the sky is falling. Didn't they say that about sequestration? And we just had to bail out the banks, or the world would end? So they're the ones with all the economic brains (or their consultants/advisors do), and we're the average ones? Your explanation is appreciated, and understood, but honestly- we've heard this one before.

Joshua Kennon

October 7, 2013

Replying to bodegha

And that's the danger - that the average person hears the warnings from people who know what this means and stop believing them so some day, the brinkmanship goes too far. The reason the bad stuff hasn't happened is because those of us who understand, and write about, economics start screaming. It won't always work.

I fully agree the debt situation is now concerning. I fully agree that we need to balance the budget. My problem is, refusing to pay the nation's already incurred bills is not only unconstitutional under Article IX, if would likely result in significantly more national debt as the interest rate expense jacked through the roof.

It's like saying, "I want to lose weight, and if you don't help me diet, I'm going to eat this entire double-layer chocolate cake!" It's lunacy.

Anon

October 8, 2013

Replying to Joshua Kennon

Our government's open secret plan is to eat 2-4+ double-layer chocolate cakes every day for as long as it's possible, and when that heart attack comes through and we die, get reincarnated and start from scratch, and start up eating 0.25 double-layer chocolate cakes every day, with the goal of getting back up to 2-4+, and give the 'ole Ponzi scheme another try. Rinse and repeat.

Why? The cake store lets us run a tab so long as we pay $0.01 in interest a year per cake and the whole town pays us $1.00 every time we buy a cake. Why not?

mwm

October 13, 2013

Replying to Joshua Kennon

JK, its funny I never hear the President claiming unconstitutionally. How could he since, as you pointed out, he voted against raising it as a senator. He also campaigned as president critical of raising the debt ceiling even to the point of calling it "unpatriotic". Also, go listen to Harry Reid rail against raising the debt ceiling in 2006 on youtube. The reality is the President could stop fiscal Armageddon if he desires to, albeit, with moving off his position.

BubbaD1

October 7, 2013

Ay, Joshua - If you have time this week, I need an unbiased update on how the Affordable Care Act is beginning to play out. So many sides and opinions, and personally, such limited brain power on my behalf.

Joshua Kennon

October 8, 2013

Replying to BubbaD1

With enrollment just starting, I don't think there is enough evidence, yet, to determine the full impact on various constituencies with any certainty. Given its influence on not only the national budget (e.g., if businesses are required to cover employees, will this result in far lower eligibility for government programs like Medicaid, lowering costs? Things like that are an open question), but pharmaceutical companies, medical supply groups, I'll be watching it. I'm sure I'll write about it quite a bit over the next year as more actual, real hard data comes in and can be analyzed.

Frederick

October 7, 2013

I'd start planning for another US credit rating cut. Last time they even got close to the debt ceiling (in 2011), the US credit rating was downgraded. What followed in 2011 was a quick decline in stock prices, which recovered within a few months. Turns out it was a golden buying opportunity, and Berkshire loaded up on stocks during that time. Be prepared with cash for another opportunity.

Joshua Kennon

October 7, 2013

Replying to Frederick

I think that is a distinct possibility.

m r

October 8, 2013

The problem here is that money from multinational corporations bought our politicians seats. The politicians do not represent the people. They are corporate robots. I've been saying again and again until you get the money out of the elections you're gonna have problems.

Matt

October 8, 2013

Excellent post, it's infuriating when people take our government's cheap financing for granted. Borrowing rates won't be this low if we screw things up, which is a real possibility given our nonfunctional government. Though I have a question on where you got the figure that the US owns 50% of the global wealth (you've said this a few times on other posts too). From the stats I've seen, the US share of the global wealth is a lot lower at between 25-35% depending on whether it's calculated using nominal exchange rates or PPP. Still tremendously high, but not nearly as skewed as 50%.

Joshua Kennon

October 8, 2013

Replying to Matt

Ah, thanks for catching that, it is my day-job influencing my numbers. Even seeing it, in my head I read it as "equity market capitalization wealth", as I immediately default to the global value of publicly held common stocks as a proxy of the economic development of a country. Over the past 25 years or so, the U.S. bounces around between 30% and 50% of global equity values (I think we're at something like $18 or $20 trillion at the moment but I haven't checked for a couple of months; our percentage is doomed to keep getting relatively smaller as nations like China experience growth, which is a good thing as we can still get absolutely richer). It was me being lazy.

The best estimate for global assets in 2005-USD estimates is $707,726,307,170,996, of which the United States owns $217,623,159,381,449, or 30.75%, which is exactly in the heart of the range you provided.

I'll re-write the above and put in the global asset levels. I think it's not only more accurate, it's a significant improvement. I appreciate you pointing that out to me.

(If you are asking this question, I'm going to assume you'll find this a lot of fun. Go to the World Bank - The Changing Wealth of Nations resource and click the "Wealth of Nations (XLS 655KB)" download on the right hand side. It will open an excel spreadsheet that breaks down the asset levels for each country, as closely as can be estimated, down to specifics like coal reserves. It's a data dream. Given the complexity, there is quite a bit of lag between regular updates, but it's still a wonderful thing to study from time to time.)

Matt

October 9, 2013

Replying to Joshua Kennon

Ah interesting dataset. It has different numbers than the Credit Suise 2012 global wealth report http://economics.uwo.ca/news/Davies_CreditSuisse_Oct12.pdf. It seems that the World Bank data aggregates most types of wealth into the "Intangible Capital" category. I would assume that the drastically higher number for US wealth ($217B, compared to the Credit Suisse $62B in Household Wealth) is due to the fact that labor income is capitalized into the wealth equation (they say that Total Wealth is the present value of sustainable consumption, which makes it seem that this number was meant to include labor rather than just the return to the (non-labor) capital stock). Interesting numbers nonetheless, as they both closely approximate the U.S. share of wealth at around 28~30%.

lokgp

October 8, 2013

Thanks for the great info, Joshua.

I am guessing this is like a family with lots of debt, but they have this sort of unlimited option to roll over their credit card debt with more debt, roll over your monthly mortgage with a greater debt to get the cash to pay for this month mortgage. The creditors, banks are happy with lending to family. But there is a problem. Mum and dad does not agree on whether they should borrow anymore money. Dad says we should, coz we got to get that cash and pay the housekeeper, the electric bills, the heater gas, the car loan, pay the cook, the gardener, the doctor etc. Mum simply disagree and thinks that we had more than enough debt, and enough is enough. We have to tighten our belts, the cooks has to go, and the gardener has to go. And dad should work his ass to keep the garden clean himself, and mum will chip in and do the cooking herself. And cash.... is running short, all the cash they have has been taken out of the ATMs. And after paying for food and some bills, money dries out on 17 October 2013. Dad says, "Honey, you are crazy! Let's borrow so more. Its not like they are not lending us any, and the interest is cheap!"

Mum insist. Bills will still come through, and they have to be paid, else, no one will trust the family again, and they will have to pay penalties and higher interest rates to roll over those credit card debt next time. The bankers are looking at this family in dismay, thinking, these guys are intentionally trying to default on their old loans. "Stop dickering around!" says the Chinese banks.

Mum says, " No, no, we will not get the loan. We will not default, the debts will be repaid." And dad asks, "How? How are you going to get the cash?"

Mum says." Easy, we have these gold coins. Your trumpet collection, your pens, my jewels. We can easily sell them to get cash, and use that money to pay for the ensuing bills." Dad,"Ok, great idea. We won't be defaulting, and we can arrange to pay the urgent ones first. I see, I see. We need to pay the Chinese credit card first, its due anyway, and when you allow us to get more loans again, we'll get to roll over it at current rates. I guess we can stop paying Uncle Ben his monthly pcoket money for now. He will have to figure it out. And delay that garderner's pay for now. He and his kids, they are not the only ones in problem, we got our own problems too, right? The banks and credit card are more important to be paid first." " But honey, when, and for how long can we continue selling our quick cash assets?" "Ermm..... I think after my jewels, we can sell our car, our summer house, that superbike, the TVs. And in the mean time, let's raise prices at our grocery stores. Its time we charge them folks more now. If we close our stores, em' folks will have no place to get those daily goodies anyway. Yeah, I think we can charge more."

Hmmm..... so, yes. The US can choose not to raise the debt ceiling, depending on how much quick assets they can sell to raise cash. And how much more taxes can be quickly raised to get those pure profit revenues. Its been done before in Sim City, it can be done here as well. But like in SimCity, you get riots later. Tightening the belt is really hard to do. And most American families are doing that right now anyway. But, raising the debt ceiling to continue get more debt and roll over its loan and get some cash is too convenient and too easy. If you can do it, why not? Contrary, the Asian Financial crisis problem is they find it impossible to borrow money to rollover their old debt, and in came the IMF to supply additional temporoary cash. And IMF plays a hard ball getting fiscal discipline back. So, it does look the US just want to try to feel how tightening their belts feels like. But it is really compelling to just rollover the debt and take on more debt. But if, let say the US default, the whole is going to have a hard time. And the US is going to have a way worse time. The currency gets devalued, and all those corporate retained earnings, become worth 20 cents on the dollar. And when the IMF comes in with their stick and cane, its going to be way way worse later. Surely, ensuring a default makes the most sense for the US, and hopefully, buy sometime to figure out how to cut off deficit and get into surplus. But like all credit card addicts know, it is really hard getting out of a ditch. Really hard.

Lord Squidworth

October 8, 2013

Replying to lokgp

People need to stop comparing government spending to family spending.

Anon

October 8, 2013

Replying to Lord Squidworth

False.

How else can you make sense of a figure like $17,000,000,000,000?

Lord Squidworth

October 8, 2013

Replying to Anon

See it for what it is, not use some grade school baloney?

That doesn't prove anything.

For starters, a household cannot print more of it's own currency.

Anon

October 8, 2013

Replying to Lord Squidworth

???

lokgp

October 9, 2013

Replying to Lord Squidworth

That's a nice illustration, Anon! I am guessing the United States intent to keep the expenses at the same current amount, or perhaps at a rate that is increasing slower than the inflation. And try to bring in more income. We all know that when credit card debt piles up, the interest portion is a big pain, and it makes it so hard to reduce the debt. So, in comes the printing machine to inflate the debt, to reduce the amount of debt in real terms. But I just can't imagine US denying themselves more debt in such crazy manner at the risk of a running out of cash to spend. It won't happen. No drug addict ever deny themselves money to buy more drugs. They always end up running out of people to borrow from. Well, let's just hope the US get to inflate the debt away and increase revenue in real terms at the same time, and try to keep expenses constant through more money saving technology of some sort, or even cheap labour.

Scott McCarthy

October 8, 2013

I have a Devil's advocate position that I can't solve. Maybe someone here can help me process it:

If the US were on the brink of breaching the debt ceiling, wouldn't the ECB (acting both in its' own financial and political best-interests) be eager to do the same forex swap arrangement that the Federal Reserve did for the ECB a couple of years ago? Swaps aren't loans, but only financial nerds (like most of us here, probably) could tell the difference - the effect would be the same. I'm not saying they'd support it indefinitely, but at least for a week or two, probably.

And even setting that aside, wouldn't empirical evidence suggest that Treasuries don't follow the normal models of financial theory? I mean, what other time in human history has there been an example of a security being rated as "more risky" and subsequently having its' yield drop (both in real and nominal terms)? After the downgrade, Treasuries acted more like a derivative (an increase in volatility causing an increase in price) than a sovereign bond.

I mean obviously breaching the debt ceiling should be avoided at all costs (and Boehner has said he'd not consider screwing around with it), but I'm not entirely sure I buy in to all of the doomsday projections (though most are likely valid).

James

October 8, 2013

I actually think the process is quite ingenious. It is meant exactly for times like this and for minority coalitions to extract something they otherwise couldn't get. The debt limit has been used as a negotiating tool countless times.

Obama himself voted against a debt limit increase and actually said increasing the debt limit "was unpatriotic". I do not think Obama is in your words "literally too dumb or ignorant to know how the financial system works" or "has a death wish for the United States and wants to see it fail".

Obama himself even negotiated with the house blue dog democrats in 2010 for a debt limit increase if obama agreed to the "PAYGO" provision. I don't recall a whole lot of articles on here or the web telling everyone how "crazy" those blue dog democrats are. In 2009 Democratic Senators joined with Republican Senators and threatened to vote against the debt limit if a bipartisan committee was not created to come up with entitlement cuts.

Let's face it....the reason why it's the law is to be used as a negotiating tool...period.

And yes, we may actually miss the deadline this time and the difference? Every time "a faction" threatened to not increase the debt limit there was a NEGOTIATION and something was given.

The fact that Reid and Obama are not doing what has been done countless times makes me think they are either "literally too dumb or ignorant to know how the financial system works" or "has a death wish for the United States and wants to see it fail".

Joshua Kennon

October 8, 2013

Replying to James

"Countless" times? The debt ceiling hasn't been used as a negotiation tactic in modern memory. This idiotic game of brinkmanship was started by the Democrats in 2009 and they've now traded volleys for four years, with the controlling party swapping back and forth, thinking it's an acceptable way to behave. It's a sign of how dysfunctional the system has become. Did you happen to see Justice Kennedy's comments the other day lamenting how all of the big social, legal, and political issues that should be handled by Congress are now ending up at the Supreme Court because they can't even manage their own affairs anymore? This is but one more symptom.

To be fair, I limited my statement to to someone who was advocating for a default to "actually" happen. I don't think people like Boehner and the upper members of the Republican party fall into that category, nor do I think the Blue Dog Democrats fell into that category.

I'm talking about people like some of my acquaintances and extended family, who honest-to-God are hoping, praying even, for a default. Not a negotiation tactic. Not a strategy move. They want the default to happen. Depending on their political orientation, their hatred for either Democrats, or Republicans, or just the current system in general have so clouded their judgement, they want some form of cosmic justice, not realizing they'd be harming themselves far more. I think a big part of our demographic underestimates the growing percentage these people make up of the general public.

They walk around saying, "We need to refuse to raise the debt ceiling! We've got to get spending under control." They have no idea what the debt ceiling is, how it works, or why it exists.

James

October 8, 2013

Replying to Joshua Kennon

My apologies...should have said numerous instead of countless. And to make my position clear I do not think we should default, period. One of the main reasons why I like this blog is because it does force me to go do some extra research even after I comment.

Since Senate Democrats did not pass a budget for numerous years during Obama's first term you have a lot of congressmen/women that can legitimately say they didn't vote for the spending. And you have split government in the Senate/House. I love split government but I think things function better when one party controls the presidency and one controls Congress/Senate. You probably wouldn't get things like Obamacare or the Iraq War.

The way around all this in the future is to pass a balanced budget amendment but that'll probably never happen so the next step is the get back to the regular budget process and put back in the Gephardt Rule.

I really don't mind the negotiating tactic though and hope Obama throws a bone to the Repubs because he is the President of the US and not the democrats. If he doesn't, then the Repubs should vote for a clean debt limit increase.

Joshua Kennon

October 8, 2013

Replying to James

I couldn't agree more with much of that. I can't imagine how frustrating it would be for a true fiscal conservative in Congress these past few years.

Have you had a chance to examine the "Debt Brake" constitutional amendment Switzerland passed a decade ago? I think it's the best chance we have here in the United States as it permits deficit spending during recessions by requiring offsetting surpluses during expansion.

The Philadelphia Federal Reserve bank had an interesting paper on balanced budget amendments in its 1st quarter 2013 business review (you can read it here if you're interested.) It ended up concluding what I have from my own reading: The Swiss model (and German model, as well) is probably superior to the balanced budget amendments that have been supported in the past that would allow for a supermajority override, plus there needs to be some significant penalty for elected officials for violating the provisions.

If you ever get a chance to study it, I'd appreciate your thoughts. I'm trying to find the flaws, but there just don't appear to be that many. Even if it weren't perfect, it would be a vast improvement over the mess we have now.

James

October 8, 2013

Replying to Joshua Kennon

Wow, never heard of it. I find that really interesting and will read that. Thanks.

bodegha

October 8, 2013

Replying to Joshua Kennon

Our system we have now is fine, its the people in charge that are the mess. It pains me to say we have a lawless President, who is a serious liar and you cannot deal with him. I trust the American people to right the ship at some point. And Joshua, I believe in satan but I never heard of the dinosaur theory...so please don't dump me into that nut bag.

Joshua Kennon

October 8, 2013

Replying to bodegha

I think you're fine as long as you aren't denying your children life saving operations or convinced a tea kettle bought at a garage sale is going to bring demons into your home because the former owner played Pokemon games (really, I've heard this).

Did you see Justice Scalia's interview two days ago in NY Mag? He has a conversation about Satan with the interviewer. It's an enjoyable read.

m r

October 9, 2013

Replying to Joshua Kennon

he enjoys seinfeld, poker and prefers to have people object to his opinions so i think hes alright. i think it's good that he believes what he believes to help keep him in check.

and if i believed in the devil, that's exactly how i would go about manipulating things. same goes for anyone with power. you can't be taken down if nobody realizes you exist. people love to mob against anything that gets too big because it's so simple for them

Anon

October 8, 2013

Replying to bodegha

Personally, I love Chicago but I will never again vote for Chicago politicians and their Chicago politics. Never again.

James

October 10, 2013

Replying to Joshua Kennon

I've read it and I think it's great. I can't really think of a drawback. Sadly, I don't see anything like that happening. I think I've been pretty consistent on here the past few years saying that nothing substantial will get done until the interest rates on our debt gets to unsustainable levels.

Did you see the 60 minutes piece on disability payments? What I didn't realize was that after 2 years on disability you get Medicare. Just wait until all these newly "disabled" get on medicare at the age of 35-45. Who thought it was a good idea for the taxpayer to pay the disability claimants' lawyer fees? I can't believe we can't fix fraudulent things like that by a unanimous vote in Congress. The amount of money that is being wasted in things like this and now add a new obamacare entitlement is just mindboggling and sad.

We need a communicator and leader like Reagan to tackle this problem and treat it like the cold war.

James

October 18, 2013

Replying to Joshua Kennon

JK - Did you see the final deal included a passage written by McConnell to have the debt limit bill in February a "disapproval" vote? Meaning a vote yes is to disapprove of the increase. If the bill passed, the president could veto and the only way to overturn is with a 2/3 majority override. Very creative.

Anon

October 8, 2013

Replying to James

http://en.wikipedia.org/wiki/United_States_debt_ceiling

Interesting reading.

James

October 8, 2013

Thanks Anon; that was a good read. I am optimistic that this all gets resolved before a default actually occurs. If it does, then I really do think the economy will have a chance to get up off the canvas and start punching back. I really do wish Obama and Boehner would have the courage to come together, ignore the party extremes, and come up with a deal that they BOTH dislike.

Anon

October 8, 2013

Replying to James

Unfortunately, the failure of the supercommittee and the ushering in of sequestration leads me to conclude there will be fatalities.

Obama and the Democrats have to either bend in unison with the Republicans, or be consistent and drop the sanctions on Iran before their government makes any concessions or negotiations go forward, since they've come to the negotiating table. Of course, the latter would be ridiculous.

m r

October 9, 2013

I love being cheap and finding exploits/deals too, but are you subconsciously doing all these things like monitoring your energy usage, enjoying the "little things", buying shares in stocks you think are depression proof like nestle and creating these meals to help insulate yourself from the shock of a coming disaster?

Don't get me wrong it's a fantastic to show people how they can live within their means and i like the buy for keeps style of investment, but it's kind of a battle of diminishing returns to a point.

The one thing I would like about another depression is that stupid, superflous skills become severely less profitable compared to actual work. There would be a lot less squeezing of the middle class because everyone would basically be on their own to survive.

http://www.usatoday.com/story/money/personalfinance/2013/10/07/position-your-portfolio-for-default/2935395/

What do you think of this story? What would the world's reserve currency become if the dollar were to lose its status?

Theist

October 9, 2013

I

always Admired your insight to Financial, Economical and even some of the more

personal articles about Philanthropy & appreciating the fine delicacies of

life, but reading these two ill composed lines of: “It’s not that we’re perfect

– it’s just that many other places on the planet actively suppress and destroy

their own human capital. How, after all, can a country expect to compete with

us when they stone rape victims or imprison free thinkers? When they

indoctrinate rather than educate? It’s not hard to win against someone who is

willingly destroying their own best chance at progress” which reflected you as

judgmental stereotyping condescending person.. you turned a perfectly reasoning

train of thoughts into a full on war against “indoctrinating religions “even

though I can give you many examples of such “indoctrination” that prospered and

surpluses in wealth, so I find little correlation to the two and would hardly

take it as the defining factor. i would appreciate a more open minded approach

to this topic, and would like to point out that no functioning government or culture still stones their

people! yet when it comes to religion you find this punishment not to be

exclusive to one religion but all three dominant theist religions on our earth.

Joshua Kennon

October 9, 2013

Replying to Theist

This is a fascinating response because it demonstrates how powerful internal bias can be when you aren't guarding against it. I want you to step back for a moment and re-read your comment. Then, go back above and re-read the section that you reference.

I didn't mention religion anywhere. I talked about the basic economic model that it is much more difficult for a nation to compete globally when it suppresses its human capital; something that has been not only proven and discussed for decades, but has been expanded upon in very lengthy tomes by some of the world's greatest Nobel-prize winning economists.

Yet, reading that passage, because you haven't yet trained your internal thought process to use mental models in a checklist style as a protection against bias, and you aren't (presumably) familiar with the direct role human capital plays in various economic models of national output, you immediately assumed that the reference to a very real, long-settled truth from academia was an attack on theism.

That is worth studying. You should try to find the reason because it could result in much greater clarity in other areas of life, which will give you a competitive advantage.

To demonstrate what I mean, consider that the communist parties in Cuba and Russia, responsible for much of the ultimate economic ruin of the respective nations, especially in the former case to the point Castro himself said it had been an utter failure, suppressed their human capital by imprisoning and executing a significant portion of those societies' thinkers, artists, authors, reporters, and professors. The economic damage was significant. A Steve Jobs couldn't have created Apple under those conditions, nor could a Henry Ford have launched the Model T. These are, perhaps, the most studied examples of the phenomenon in the modern world. They weren't doing it on religious grounds.

The reunification of East and West Germany provides another example of this long settled economic truth. The reintegration of personal freedoms and free markets resulted in Germany, in a few short decades, going from total destruction to the most prosperous economy in Europe besides Switzerland. There was no significant religious input in this scenario.

In China, during the 20th century, the non-religious Mao regime and what followed committed some of the worst suppression of human capital in history, resulting in economic devastation so great that during my own childhood, it was not Africa that people were concerned about, it was "the starving kids in China". When they finally reversed course, something that still has a long way to go, the economic prosperity exploded. There was a total absence of religion in this particular situation.

Is religion the reason in some nations? Yes, absolutely. And, interestingly, the particular religion doesn't matter. Christianity, my own family's religion, was responsible for human capital suppression during the Puritan era when you had things like the Salem Witch Trials or laws banning certain forms of dress or speech. At the moment, many countries in the middle east are actively suppressing human capital - the other day, the Kuwaiti government is going to attempt to begin administering medical tests to all incoming people to screen for "secret" gays so they can make sure they are turned away at the border. It doesn't take a genius to see that means that the Michelangelo's and Da Vinci's and Turing's of the world would be turned away, and forced to go to some other nation that would then get the dividends from their brainpower. Saudi Arabia's restrictive laws on women are the reason that the Eastern and Western world keeps pumping out lists like this, and get to keep all of the economic wealth and gains in standard of living that resulted from the breakthroughs.

Yet, you immediately disregarded all of those secular examples, jumped to the conclusion that religious belief by itself, inherently, was being attacked, and, what is particularly interesting, is that you jumped to this conclusion despite the fact that my family's foundation makes religious grants one of its five main categories of gifts, which, by definition, if I thought all religious belief were irrational, I wouldn't be bankrolling some of the projects.

The economic models that deal with suppression of human capital don't care why human capital is being suppressed. It doesn't matter. It could be for religious reasons, secular reasons, political reasons, or prejudice indoctrinated at childhood (e.g., one tribe being taught that the tribe over the hill are really sub-human or the demonization of Jewish people during the Second World War inside of Germany). All that matters is that suppression of human capital leads to much lower GDP output. It's a great economic truth. Only in very rare circumstances can it be violated (e.g., a non-industrialized society where a highly lucrative crop or natural resource can be mined more cheaply by slave labor than the value of the lost human capital would generate for society; we saw that in the United States in the 19th century. It is not an exaggeration to say that, without the invention of the cotton gin, which ultimately changed the labor calculation, slavery never could have ended).

The questions I'd be asking myself are:

1. Why did I immediately take this as a religious attack when religious may or may not be present or responsible for the suppression of human capital? Was it a lack of familiarity with the role of human capital in GDP output? Was it that I had been subject to religious persecution in the past and had now defaulted to constantly being on the defense, taking slight where there is none?

2. If I had been familiar with the economic model of human capital and its relationship to GDP output, why did I immediately discard all secular examples of this phenomenon, and assume the author was speaking solely about religion even though religion wasn't mentioned?

3. What other areas in my life could I be committing this cognition error?

Theist/Reply

October 12, 2013

Replying to Joshua Kennon

Joshua,

an insight as astonishing as ever & the thing that has kept me coming back

to your blog for almost a year now. after the first few reads of your response i got to the conclusion that my comment was an emotional one rather than intellectual, you've made some very good points and pointed out few gaps in my economical knowledge which i'll be working on after finishing this reply.

Thank you

for your time and response.

Joshua Kennon

October 9, 2013

Subconsciously? Not a chance. I grew up hearing stories of the Great Depression and am a huge fan of history books and biographies. There will be another crash, and there will be another great bull market. When they come, no one knows, but there are intelligent things to do in almost every scenario. I actively arrange my life, and finances, to survive almost any scenario and periodically do risk evaluations.

But that's not why I do these projects. I like the optimization and efficiency for three reasons:

1. Even presuming we never have another collapse in our lifetime, it still produces significant future wealth for the investor, and his (or her) children and grandchildren.

2. It results in less societal waste. It may not seem like much at the moment, but over a lifetime, it adds up significantly.

3. I'm the type of guy that likes spending 100 hours perfecting the infrastructure of a municipality in Sim City. I like systems-building. It has its own, intrinsic, emotional reward that is significant. I'd do it even absent the other things. It's the adult version of playing in a sandbox or running model trains.

Geoff Fairfield

October 10, 2013

To cover any budget shortfall, why doesn't the Treasury just sell a tiny fraction of the $3.59 trillion of securities that the Federal Reserve bought during QE?

Scott McCarthy

October 14, 2013

Replying to Geoff Fairfield

The Federal Reserve is independent of the Treasury. The Treasury does not have the legal authority to dictate what the Fed does or does not do. While the Fed pays any profits on its open market operations to the Treasury, if there are no profits, then the Treasury doesn't get any money from the Fed (aside from making withdrawals from its' own account).

Jonathan

October 16, 2013

Aren't the President and the Treasury obligated under the 14th Amendment as well? In other words, if Congress does not increase the debt limit, shouldn't the Executive pay the $415+ billion of interest payments with the $2+ trillion of tax receipts it collects "every" year?

Odai

October 29, 2013

I originally wrote off the whole debt ceiling thing as partisan politics and Republicans being crazy. But as I've thought about it, assuming their intention was to educate the populace on the degree to which our economy relies on a precarious government, I have to admit that Republicans in Congress have actually done a great service for our country - they've gotten us to discuss the subject, which may eventually snowball into policy improvements.

Clint

January 13, 2015

Just curious, but under the PATRIOT act (which I also don't support) wouldn't knowingly breaking the constitution in this manner, also known as knowingly committing an act of treason, land the whole house of representatives a no trial, one way trip to a military prison?

Just a thought.

Nancy Cage

January 21, 2016

Good Day Everyone.

Am here to share my testimony what a Good trusted man did for me. My name is Nancy Cage am from Michigan USA and I'm a mother of 3 kids and i lost my husband last year June 2nd and things where very hard for me and my children so when I was online to seek for a loan and i fall in the hands of scam, i was scam over $10,000.00 dollars, all my Husband access where taken away from us by his brothers, all hope was lost and i and my kids where sleeping in the street on till one faithful day when i met this friend of my who introduced me to this honest company who helped me get a loan in next 24 hours without any Daley, i will forever be grateful to Mr William Magnus , you can contact him via email: [email protected] he did not know am doing this for him,but i just have to do it because a lot of people are out there who are in need off a loan. Contact with him ASAP