Imagine that you have a new neighbor. We’ll call him Rod Smith. One day, he shows you his portfolio. He has a little over $1,000,000 in common stocks. “I have this great idea!”, he tells you, excitedly. “I decided to buy a list of companies I like and pick up around 421 shares of each. That’s my investing strategy. What do you think?”

You look at him kind of funny as you process what he just said. “You’re … just going to buy 421 shares of everything? Or roughly that? That’s your genius plan?”

“Yep!” He says, very proud of himself. “This is bound to work!”

“My God, man. Isn’t that asinine? By definition, it means if one company has a $100 stock price, and another a $10 stock price, you’ll invest 10x as much in the one with the higher share price, even though it’s entirely cosmetic. After all, the first company may just not like splitting its stock very much. It could be smaller and less profitable than the latter. ”

Rod thinks for a moment. “Well, yeah. But I’ll make a little modifications so stock splits don’t have that distorting effect. But other than that, you’re right. The higher the stock price, on average, the more money I’ll invest in the company.”

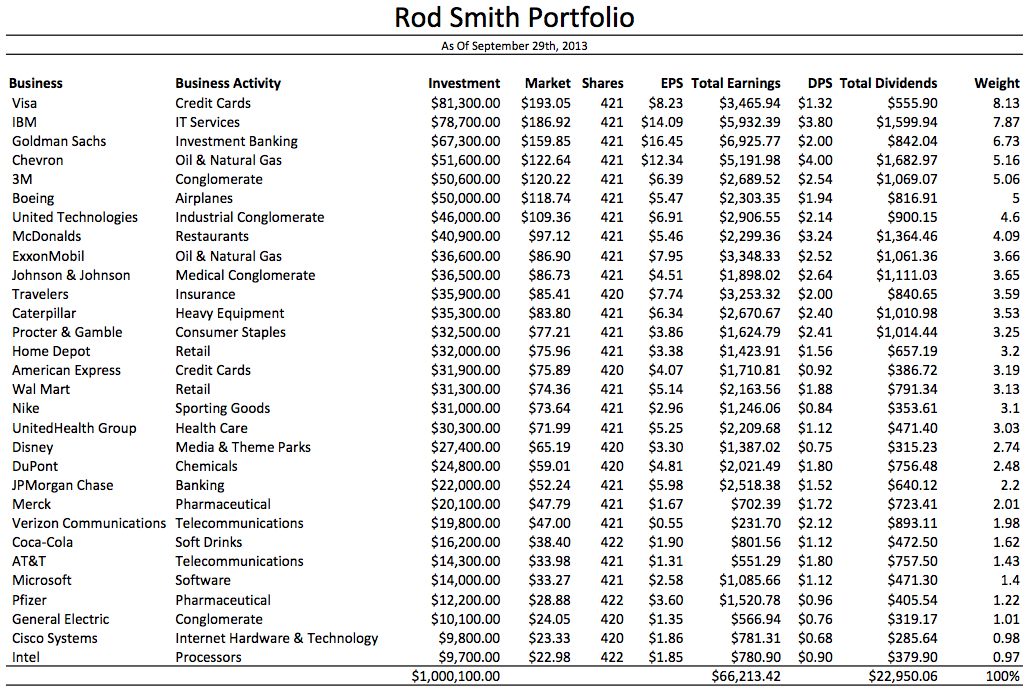

You kind of sigh. Rod’s a nice guy so you take the paper to look over his list of investments despite this batty way of thinking. You’re impressed. His list of stocks is a good one. It’s made up of quite a few wonderful businesses, and a handful of okay ones. His share of the net earnings is $66,213.42 per year, of which $22,950.06 is paid out as cash dividends. That’s very attractive compared to U.S. Treasury bond yields. By all accounts, if the past century or two can be trusted, at his present cost basis, and current earnings level, he could expect about an 8% to 10% nominal return, assuming inflation runs 3% to 4% per annum, on average. Sure, it will be a bumpy ride – up 20% this year, down 30% the next – but that’s the nature of equity investing.

Over the years, Rod does fairly well because he very rarely buys or sells anything. It’s the same system his father and grandfather used. He pays no management fee on his portfolio. He sits on his backside and watches his money compound, year after year, while collecting cash in the mail. Sure, there is some judgment involved. He may decide he doesn’t like one of the companies and sell it, adding another in its place. He’s disciplined, though, so it isn’t common. He does screw up from time to time. He still gets upset about the fact that his dad and grandpa kicked IBM off his list of stocks years ago, and then, later, after it had recovered, Rod added it back to his list. Had it never been removed in the first place, his portfolio would be worth more than twice its current value. But, whatever. He’s done well enough. Life is good.

In fact, despite being perfectly average, not doing much, and having this crazy methodology, Rod beats a significant majority of amateur and professional investors. They are constantly hyper trading, driving up commissions. They are constantly paying high fees or other costs. They never get to take advantage of the leverage effect of deferred taxes. Rod, on the other hand, does nothing and collects his share of the business results. You still think his idea of roughly 421 shares in each business is stupid and arbitrary, but his other behavior, and the list of companies he owns, makes up for it.

Is Rod Behaving Rationally When It Comes To His Investments?

How do you feel about this? Would you be ready to jump on Rod’s way of thinking? Would you be reaching for your checkbook?

Why or why not?

Would you constantly compare your portfolio against Rod’s? Would you lose sleep if your portfolio was doing a worse than his?

Why or why not?

If you answered, “No” to any of those questions, then here is the next logical inquiry you should answer: Why do you care about the Dow Jones Industrial Average?

Rod’s portfolio is the DJIA as of last Saturday.

Rod is the editorial board of The Wall Street Journal that picks the list of stocks.

That’s the thing. There’s nothing inherently magical about the particular list Rod owns, or the weightings he selected. The S&P 500 is barely any better in its own brand of bonkers thinking – it weights the holdings by the size of the market capitalization of the common stock creating an odd situation where, though there are nominally 500 companies in the portfolio, it is far less diversified than one would think and has a significant overlap with the Dow Jones Industrial Average.

Rather, the real value from Rod’s portfolio comes from the low-activity, long-term behavior, rock-bottom costs, and focus on a mix of businesses that happen to be far more profitable than average.

That’s why I think indexing the most rational strategy for practically everyone who can’t value a business, doesn’t want to think about financial statements, doesn’t enjoy the allocation process, isn’t rich enough to hire a top-notch advisor (who can often provide tax, estate planning, or asset protection strategies that more than makeup for the fee differential on a large enough portfolio), or doesn’t have emotional control. It captures almost all of the good, as long as the underlying index is at least somewhat sound, while protecting against a lot of the foolishness. It’s a fundamentally satisfactory approach that is the golden ticket for a lot of people.

Of course, there is the obvious paradox that indexing would cease to work the moment it was adopted by a significant percentage of investors due to its distortion of the market as the index components were driven up far above their intrinsic value and there would no longer be individuals or institutions making non-index positions to correct, or revert it, back to the mean. Nobody worries about that, though, because it’s highly unlikely indexing will ever come to represent a supermajority of investable assets.

Reader Comments (16)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

scott

October 2, 2013

For me personally I like the idea of index funds, however I have difficulty being inspired to save money to dump into a vortex. Its easier to pass on frivolous spending when I can quantify the Dollar amount as so many shares of bp or ge etc. The potential gains from a hot fund are overcome by an increased saving rate.

jb1907

October 7, 2013

Replying to scott

an index fund isn't a vortex. If you buy at X and the index fund is 10% higher than X, you have made money.

Richard Garand

October 2, 2013

As an index investor I've considered how popular it could become before it starts to lose effectiveness. As long as there is enough liquidity in the market for all index purchases to be met by sellers who are willing to sell at a reasonable price, and sales are met by buyers who are willing to purchase at a reasonable price, index investors should not suffer from any inefficiencies. Of course that requirement varies from day to day and is subject to the same problems that fractional reserve banking has with a sudden surge in demand. And calling a price reasonable implies that you have done a valuation on all stocks in the index, which most index investors have not, but for my purposes a reasonable price is one that allows long-term returns in line with those seen historically.

The paradox is that even if the market was far short of the liquidity required for this, a cap-weighted index would still do its job. Half of non-index investors have to do worse than the index, so for an investor who doesn't want to do the research to be in the upper half the index is still the only good choice. It will always be possible to do better than the index. It will never be guaranteed.

Eric

October 2, 2013

Those are really good companies, and I'd be fairly happy with Rod's account, but it doesn't allow for any smaller "diamonds in the rough" that you have special knowledge about. Rod's investments look like a portfolio designed for a person with no specialized knowledge. For example, I know a lot about banking, and there's a small bank in Virginia that I adore, and have followed for more than 10 years, but Rod's strategy would prohibit me from investing in it. Also electric utilities are missing altogether, and from knowing people in the industry, I see a fabulous future for utilities (other than California utilities which have their arms tied behind their back). Rod will do well, but could do better by focusing on just a few companies/industries he understands.

Andrew

October 3, 2013

Most investors have far less than $1M in capital. There are two other advantages of buying a fund that tracks an index assuming you are investing smaller sums:

1) Diversification - the trading commissions to buy all 30 or 500 stocks of the index would be expensive for smaller sums

2) Rebalancing - As the index changes over time the trading commission again makes it expensive for an individual to rebalance their portfolio to match the index

By pooling capital, the index fund provides these benefits and shares the expenses. All while keeping (poor) decision-making to a minimum.

Scott Holland

October 3, 2013

I have been very happy investing in REITs and BDCs lately.

Evaluating companies that will be of great use within emerging markets as the global middle class rises in the coming years is one of the surest ways to attain financial security.

Consumer staples and basic resources and packaging will be key sectors to examine.

Skyler

October 3, 2013

Joshua,

Lets pretend, for a moment, that index investing really becomes the norm. The new "Everybody's doing it" investment. When Mr Market decides to take a turn for the worst, for whatever reason, and people start selling ETFs in droves, driving down the price to NAV ratio, will index funds be forced to liquidate there holdings on the open market to keep that ratio in check? And, if that is true, would the ETFs be forced to sell ALL underlying holdings, without bias? Would that then create the perfect climate for value investors picking individual securities?

Eric

October 4, 2013

Replying to Skyler

That's kind of what happened in 2008/09. Funds with diversified holdings had to liquidate everything to raise cash for panicked investors, so individual securities became a screaming bargain.

jb1907

October 7, 2013

I will never buy individual stocks. Mutual funds and ETFs are better.

Joshua Kennon

October 7, 2013

Replying to jb1907

I agree, for a vast majority of investors.

A technical point that won't have much practical effect for you but still should be corrected: Since equity mutual funds and ETFs are made up of individual stocks, by definition, they cannot be "better" than individual stocks. It would be like saying a carton of eggs is better than eggs.

It may be more accurate to say, "Mutual funds and ETFs are more suited to the investment problem, as presented, given their tendency to act as a counterforce against irrational investor behavior as pertains to asset turnover, expenses, and diversification."

If you own an S&P 500 index fund, for example, you do own individual stocks, just through a legal entity that handles the buy and sell decisions for you. That is, you can't "own" the S&P 500 because it doesn't exist. It's a theoretical concept. Instead, what you own is Apple (2.81%), Exxon Mobil (2.76%), Johnson & Johnson (1.74%), etc.

That is why, if you are rich enough, you won't own individual index funds. Say you had $10,000,000 and were paying a rock-bottom expense ratio of 0.17% per annum on a great index fund. That's $17,000 in fees and lost money each year that makes no sense for you to pay. It would be better to just construct your own replica of the index fund by buying the underlying shares directly as your costs would be a fraction of that expense ratio, and mostly one-time whereas the expense ratio is every single year. And that's precisely what many people do, albeit this is a problem with which all but a minority of the population will ever contend.

Going back to the illustration in this post, if you had $1,000,000 or so and bought a Dow Jones Industrial Average ETF and Rod has his portfolio, you are both going to own the exact same economic portfolio. There is no difference. None. Zero. That's a very important concept to understand. (Rod is actually in a slightly better place due to his lower expense ratio, which would amount to an extra $167,000 in wealth over 25 years. Again, this only become true when you start dealing with larger figures, which most investors are not, making the index fund a much more attractive choice for them.)

jb1907

October 7, 2013

Replying to Joshua Kennon

True, but the ETF can have better returns than a basket of single stocks since a particular ETF holds all stocks, not just a few. A Mid-Cap index fund can do better than a few stocks since a person has to pick the best stocks. As to your point in regards to diversification. Few people can pick the best stocks that get a better return than the indexes in general.

jb1907

October 7, 2013

Replying to Joshua Kennon

But Rod has to be extremely disciplined to not sell a particular stock if the market goes south. I also wouldn't buy a Dow ETF since it is only 30 stocks. The S&P to me is more broad and offers better diversification. Then you would have to buy 500 stocks.

Joshua Kennon

October 7, 2013

Replying to jb1907

Again, I agree wholeheartedly that index investing is the way to go for the average person for the variety of reasons we've discussed. And they work for all the reasons you've described - harnessing investor irrationality and sub-optimal behavior patterns in a way that avoids a lot of the big mistakes. I write about the details because I want to make absolutely certain people know what they are getting when they buy into one. I think transparency is important.

On a personal side note, I find this line of thought (that Rod would need to be extremely disciplined not to sell a particular stock if the market went south) interesting for two reasons:

1. ) Why would that be a temptation? If the account were a privately constructed index fund, selling the stock would mean he was no longer tracking the index, he'd be actively managing the fund. If he'd committed to indexing, deviating from the index weights should never cross his mind. It would be like a Catholic using the Bible as toilet paper - unthinkable!

2.) Were a temptation to arise, wouldn't the more rational temptation be to buy more not sell, if a company were dropping in price? I'd love to see my stake in Nestle fall by 50% today. I'd be doing cartwheels at the office, provided the underlying long-term earning power of the enterprise remained intact. I'd be thrilled if my Wells Fargo fell from $41 back to $10. It means I could buy more dividends and net earnings for a lower price, which equals more cash I get to collect while reading, playing video games, traveling, working, or cooking. I love getting direct deposits constantly flooding in from my holdings. It's intoxicating. Can you imagine if Royal Dutch Shell were paying an 11% dividend instead of the 5.3% or whatever it is at the moment? Don't you dream of a world where Disney offered a base yield of 3% instead of 1.2%?

Falling stock prices do induce temptation, but selling is not one of them. Not for me, anyway.

Bufu Bobbins

March 25, 2016

Replying to Joshua Kennon

Sorry to necro such an old comment, but RDS.B yielded a bit over 10% in late January 😀

Bufu Bobbins

June 2, 2016

Replying to Joshua Kennon

Sorry for the necro, but RDS was paying 10% in February 😀

chip henry

May 5, 2017

Very interesting post. Thank you for writing it. I have one day's experience into the thought of buying the stocks of a fund vs buying an index tracking fund. If one were expecting an inheritance shortly, of just the amount where the principal stayed invested and the returns were needed for income, using the idea of creating your own 'index' based on, say, 50 of the NASDAQ 100, how would you handle the stock sales that would become the income?