How Quincy, Florida Became a Town of Secret Coca-Cola Millionaires

In the 1920s and 1930s, a banker named Pat Munroe in the small town of Quincy, Florida noticed that even during the depths of the Great Depression, otherwise impoverished people would spend their last nickel to buy a glass of Coca-Cola. With good returns on capital, and a once-in-a-century valuation so low that the business was trading for less than the cash in the bank, “Mr. Pat”, as he was called, encouraged everyone he knew to buy an ownership stake in the firm. He would even underwrite bank loans, backed by Coca-Cola stock, for his responsible depositors to encourage people to acquire equity.

Coca-Cola had gone public at $40 per share but a conflict with the sugar industry and its bottlers resulted in a 50% crash shortly thereafter, when it reached $19 per share. Focusing on the bottom-line profits, and the power of the brand, Pat Munroe kept buying. And he kept telling everyone else to buy, too.

Coca-Cola had gone public at $40 per share but a conflict with the sugar industry and its bottlers resulted in a 50% crash shortly thereafter, when it reached $19 per share. Focusing on the bottom-line profits, and the power of the brand, Pat Munroe kept buying. And he kept telling everyone else to buy, too.

That one observation, and Mr. Pat’s business skills in convincing others to buy assets that produced cash irrespective of short-term market fluctuations, not only changed lives, it saved the farm town during the Great Depression as the local economy was supported by Coca-Cola dividends. It has also supported the town in “every recession since”, according to the man who now runs the trust department in the bank that was once headed by Munroe.

When crops fail, it was the Coca-Cola cash that kept people employed. When the national economy collapsed, it was the Coca-Cola cash that allowed people to stay in their homes. When times were good, and Coke was cheap, more shares were purchased.

Quincy became the richest town per capita in the entire United States at the time. At least 67 appropriately dubbed “Coca-Cola millionaires” amassed significant fortunes before passing those fortunes on to their children and grandchildren, in some cases through outright gifts and in other cases through the use of trust funds. The bank where it all started has Coca-Cola on display and, as of four years ago, a staggering 65% of the trust assets under management are still invested in Coke stock. (Coke has had a nice run since then as profits increased and the world recovered from the crash in 2009, so I’d imagine it is even greater today, all else being equal.)

A single share with dividends reinvested is worth $10,000,000 in 2013. It would be gushing $270,000 in pre-tax cash dividends to the owner by sending a check for $67,500 or so in March, June, September, and November of each year.

One share. One. Had great-grandma and great-grandpa picked up a round lot of 100 shares for $1,900 to $4,000 depending on the purchase price, they’d be sitting on a billion dollars, excluding the effects of estate taxes. (To see those kinds of returns, take a look at the old Sun Trust Bank annual reports. The bank received $100,000 in Coca-Cola shares during the IPO for its part of the underwriting deal and kept the stock in the vault for generations. It grew into billions upon billions of dollars, gushing out tens of millions of dollars a year in dividends that supported the bank’s balance sheet.)

Quincy, Florida, and Pat Munroe, are one of my favorite case studies. It was a group of people who decided to ignore the stock market entirely and focus on the one metric that matters: The profit generated by the business, and to a lesser extent, the percentage of that profit that was received each year in the form of dividends.

As long as profits and dividends went up each year, and there was no change in the competitive position of the underlying business, shares were bought when they were attractive relative to other opportunities. They were never sold (what other asset had the same characteristics? How do you replace perfection?).

This is what people mean when they say it only takes one good idea in life to get rich. And once you are rich, you never have to do it, again. There are few things that can reward you as much as ownership of a great asset can. (The only others being a happy marriage and good health.)

Quincy, Florida is made up of secret Coca-Cola millionaires living in an otherwise small town.

Image Licensed from Wikimedia by Ebyabe

Not all businesses have the same characteristics. I wouldn’t be able to sleep at night if my entire net worth were invested in banks or, even, for that matter, a strong technology company that was subject to quick disruptions in market share. The skill, and experience, necessary to tell the difference is one of the reasons some families end up wiped out and others keep getting richer, even through major crashes. It is a lot more difficult to take down a firm like Coca-Cola, Clorox, Hershey, General Mills, or Nestle than it is to wipeout a Microsoft or Citigroup. That does not mean I wouldn’t invest in businesses like the latter two. It just means I am aware of the risk profile and the need for heightened vigilance.

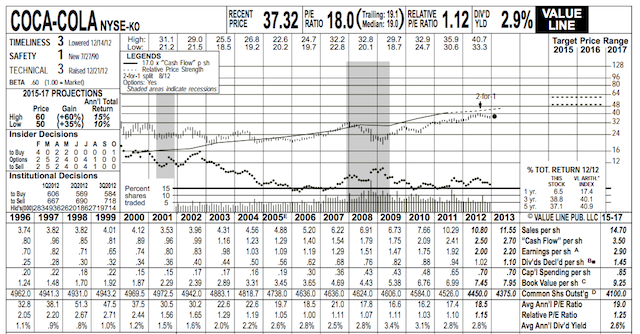

You also cannot pay any price you want. The price you pay for an asset matters. Look at the earnings of Coca-Cola over the past 17 years.

In 1998 the price-to-earnings ratio for Coke, which was already the global leader in soft drinks and massive in scale, averaged 51.3. That means “investors” – and I use that term lightly – were willing to accept a 1.95% earnings yield before dividend taxes, no less at a time when they could have earned at least 5.5% to 6.0% on long-term Treasury bonds. That means the risk-free Treasury was paying almost 300% more than owning a piece of Coke was. (To learn more about this concept, read about adjusted earnings yield vs. Treasury bond yields.)

Rationality eventually returned, and the stock went sideways for more than a decade, instead of quickly crashing, until the underlying profits caught up with the share price. Profits grew from 70¢ per share in 1996 to $2.00 per share last year. At the same time, the stock price barely budged. That is because people are only willing to pay 18x earnings today. While still somewhat expensive, it is a far better deal than 51x earnings.

If you could ever get a business like Coke at 10x earnings in a current interest rate environment – which was almost possible in the 2009 meltdown – a long-term investor might do very well by purchasing as much as he can reasonably afford. It is extremely difficult to foresee a situation in which 50+ years from now, a large investment in a Coke-like business isn’t worth exponentially more than the price paid for those shares. There will be many 30% to 50%+ drops during that time period – it is inevitable – but the basic compounding of the underlying profit machine does not appear at risk given present known factors.

I’ve never been able to build a large direct position in Coca-Cola because of the timeframe of my life. Looking at the valuation chart, in 1996, I was in junior high. Up until recently, the shares were nowhere near reasonable, so only those who had bought in prior to the speculative spike could sit back and enjoy the cash their company threw off regularly. My exposure came almost entirely through the Berkshire Hathaway shares I’ve collected since I was young. These days, each Berkshire Hathaway Class B shares represents roughly 0.16 shares of Coca-Cola, which come along for the ride, due to the 400 million shares that the conglomerate owns. That means for every round lot 100 shares of Berkshire a person has, he or she also has indirect ownership of 16 shares of Coke. Even as recently as eighteen months ago, it was cheaper to buy Coca-Cola through Berkshire Hathaway.

Editorial Image Credit: vengerof / Shutterstock.com

Editorial Image Credit: vengerof / Shutterstock.com

Reader Comments (25)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Jason Spacek

February 4, 2013

ONE share? Holy moly!

Great article, Josh.

TicoHombre

February 4, 2013

Awesome, Awesome, Awesome post! Thanks!

jss027

February 4, 2013

Joshua,

Speaking of passing fortunes along to children and grandchildren. I have

created a personal goal of constructing a forever portfolio that will pay out

dividends to my family for generations to come.

I have a concern that I would

appreciate your thoughts on. You often

recommend investors to utilize tax advantaged accounts (like IRAs, roths, etc.)

to accumulate their portfolio. However,

I understand these types of accounts force position sells through the “required

minimum distribution” once you meet a certain age. I’ve also read that there is not a RMD for

the first owner of a Roth, but the RMD will kick in for the first generation

beneficiary. Additionally, I understand

using dividends as your RMD would be taxed at the earnings income level, rather than the

current 15 or 20% via a taxable (non-retirement) account. Ideally, my goal would be to never sell and

live off of the dividends. I’m thinking

that if I didn’t have to sell, the power of compounding and dividend growth

after 40+ years would become exponential and far exceed the tax hits I am

taking today by not investing my surplus in Roths or IRAs; not to mention my

total control over the account and to not be forced to sell of a great asset. So I am leaning towards taking the tax hits

now and saving/investing all of my surplus dollars (in excess of my 401k min to receive the match) in taxable accounts to

maintain this control and set up the family for generations. I would like your thoughts on this long term

strategy. A few givens...my wife and I both work, combined we're in the 28% tax bracket, ages are 36 and 35, own (cashflow w mortgages) a few of residential rentals.

Would you mind sharing your thoughts?

Thanks

Joshua Kennon

February 5, 2013

Replying to jss027

Did you send this in as a mail bag submission? If so, I have it on the "in progress" responses. If not, there is a mail bag coming up in the next couple of weeks that addresses this exact question.

jss027

February 5, 2013

Replying to Joshua Kennon

Yes that was mine...excellent. I'm looking forward to reading your thoughts. I appreciate all the valuable information you share.

Peter_Jan

June 1, 2013

Joshua,

I may be a technology optimist, but can't you imagine a future where people can 3D print their own beverages?

In fact, one of the reasons Warren Buffet became the richest man in the world is because he essentially betted against technology (intensive progress) in an age of globalization (extensive progress). He was right for his lifetime.

With the resource demand effect increasing and automation making the wage gap smaller, globalization is no longer as much of a benefit to developed nations as before (Ben Bernanke alluded to this a few years ago). The marginal returns may well be in technology for the coming decades.

What's your view on all of this? Do you dismiss the notion of a 'singularity' (predicted as early as 2029 by some) and do you agree that your world view is essentially long on globalization, short on technology? If not, why not?

Joshua Kennon

June 1, 2013

Replying to Peter_Jan

Excellent question. I needed 2700+ words to respond as the comments section was not remotely sufficient to address the issues you raise. The new post with my thoughts is here.

Yan

June 19, 2013

That's a great story and well written. However, it is a story and I would caution anyone who thinks this is a good investment approach. Survivorship bias is incidious and we're all susceptible to it, unfortunately many have lost their shirts by failing to recognise its effect on their thinking.

For most people concentrating their assets into one company is a bad strategy. It's closer to gambling than investing. Sure some win, but most don't...

How many other towns of well meaning people were there that invested in companies that seemed just as sure footed as coca cola and lost everything? It's easy to now consider Pat et al. as geniuses with great insight but it's just as likely they were just lucky. Any number of events *could* have destroyed cola and left them all in deep shite!

Joshua Kennon

May 11, 2016

Replying to Yan

While I don't have any disagreement with the importance of watching out for survivorship bias, that's not the interesting mathematical phenomenon behind this story. These were not people risking their farms in any meaningful sense to buy shares of Coke, holding it as their sole asset. Seeing that Coke was not only an incredible business with returns on capital that were absurd but that it was run by a man who was notorious for keeping the place completely debt-free - how, precisely, does a profitable business go bust when it doesn't owe anyone, anything, and it's still making money even in the midst of the worst economic collapse in 600 years? - they bought it and, as time passed, its compounding rate was so superior to the other assets they held, it came to dominate their net worth. This has to do with the the way diversification and compounding interact. Even had Coke gone bankrupt, its payouts were large enough in the years prior that, like Eastman Kodak, the compounding return would have ultimately still been satisfactory.

Instead, as it became a larger and larger percentage of the town's portfolio, and seeing that the operating earnings were still intact, many of these families wisely held onto it, in many cases taking advantage of something known as the stepped-up basis loophole that allows families with appreciated securities to effectively have all of their unrealized capital gains forgiven under certain circumstances. This gave these families a way to accomplish a massive generational transfer of wealth that would have dwarfed any concentration risk given that the concentration risk could have been mitigated through 1.) the redeployment of the significant cash flows from Coke's historically generous dividend, 2.) the systematic writing of fully-covered calls against existing positions, and 3.) the ability to hedge against absolute catastrophe through the purchase of far-out-of-the-money puts to lock in a sale price that guaranteed a certain standard of living, all three of which would have been run-of-the-mill for any wealthy family concerned about the potentiality of Coke going bust.

Again, I don't disagree with you, it's just that the premise is flawed. There were not many companies that "seemed just as sure footed as coca cola". It was the world's largest beverage company and had no debt. It was run by a controlling shareholder who had his entire life wrapped up in it and cared about little but driving competitors out of business. The margin of safety was so large that it was certainly less risky to have, say, 50% of your net worth in Coca-Cola than have a single farm or be employed by a single employer upon whom you rely for 100% of your household income. These were not poor folks swinging for the fences. Not even close.

Coke is still a goldmine today for a long-term owner. It controls 3.5% of the beverages consumed in the world each day, including tap water. It's balance sheet should survive another 1-in-600-year Depression with aplomb. The dividends should remain flowing under even the most difficult circumstances. In fact, out of 30,000 publicly traded business, I can only think of a handful - less than 10 - in which I would absolutely, positively sleep well at night with 100% of my net worth in them, knowing I could ignore the market fluctuations and live off the income along. Coca-Cola is among them. Nestle is another. Johnson & Johnson, too. Treating it like "just another stock" is like treating the Brooklyn Bridge like "just another bridge". The redundancies are obscene. There is an inherent element of safety that, while not foolproof in an uncertain world, certainly makes them relatively less risky than almost all other holdings and this was plainly evident in the 1930s, too. Fortune magazine ran a story talking about how Coke was one of the biggest, most profitable, most stable blue chips of all time. It wasn't some start-up or something. An order of perspective is necessary to understand the context in which these residents were making their allocation decision.

Joshua Kennon

July 17, 2013

I just published my response to your question.

Dhirubhai Mehta

June 24, 2014

An "inspired" article. Author ought to have acknowledged you. http://www.livemint.com/Money/p5LUjZQRvRdMyGODpWxX5K/Pat-Monroe-Coke-and-the-culture-of-equity.html

Mr Wood Barry

June 5, 2015

Hello Dear Sir/Madam.

I am Mr. Wood Barry, a private money lender. I give out loans with an interest rate of 3% per annual and within the amount of $1000.00 to $500,000,000.00 as the loan offer. 100% Project Funding with secured and unsecured loans are available. We are guaranteed in giving out financial services to our numerous clients all over the world. With our flexible lending packages, loans can be processed and funds transferred to the borrower within the shortest time possible. We operate under clear and understandable terms and we offer loans of all kinds to interested clients, firms, companies, and all kinds of business organizations, private individuals and real estate investors. Just complete the form below and get back to us as we expect your swift and immediate response. EMAIL : [email protected]

Attention!!!

Do you have a bad credit?

Do you need money to pay bills?

Do you need to start up a new business?

Do you have unfinished project at hand due to bad financing?

Do you need money to invest in some area of specialization which will profit you? and you don't know what to do.

We offer the following loans below,

personal loans[secure and unsecured]

business loans[secure and unsecured]

combination loans

students loans

consolidation loans and so many others.

1. Full Names:............................

2. Contact Address:.......................

3. Loan Amount Needed:....................

4. Duration of the Loan...................

5. Direct Telephone Number:.................

Email [email protected]

Best Regards,

Mr Wood Barry

007

July 10, 2015

One word. Tesla!

shlomo

July 10, 2015

The question is, will we have a future similar to the 1900s-2000s in America? I think that's less likely than some assume, and if so can we expect such returns?

Joshua Kennon

July 10, 2015

Replying to shlomo

It's more profitable, enjoys higher efficiencies and economies of scale, has better competitive advantages (including an entrenched distribution system which would cost a competitor more than $100 billion to replicate by most estimates) and has expanded into other liquids such as juice, coffee, tea, and water to the point it now represents 3.5% of all beverages consumed, including tap water, on planet Earth each day.

These do not fill me with a lack of optimism about its prospects for long-term owners in the coming century provided a person could 1.) hold for 25 years or more, and 2.) avoid selling during the inevitable stock market crashes that will occur from time to time.

shlomo

July 10, 2015

Communists wrong marx john locke mises libertarianism. Test for bot.

Gabriel Moraes

July 10, 2015

Replying to shlomo

Yeah, Greece didn't work out right. Good riddance

Perhaps marx was just misrepresented... once again, and again, and again, and again...

jon

July 10, 2015

The equivalent today is bitcoin, everyone should own at least $100 worth.

Joshua Kennon

July 10, 2015

Replying to jon

Bitcoin, by its very nature, is not a productive asset making it entirely non-comparable to equities, real estate, farm land, or other holdings that can produce value regardless of whether the asset itself were ever old. In the case of Coca-Cola, for example, the initial purchase price has been paid back thousands of times over by the aggregate cash dividends sent to the owner over the duration of the time period being discussed. That doesn't mean it couldn't become worth exponentially more than its current market value, only that the intrinsic value itself is dependent entirely upon what other people will pay for the asset, making it fall outside of the Benjamin Graham definition of "investment"; there is an inherently speculative component at the core.

Teresa Berger

July 13, 2016

Replying to jon

Im trying to buy some bit coin. Please send more info.

rka19

July 10, 2015

Communists have been saying that ever since Marx. They have so far showed nothing except failure after failure, capitalism has by-and-large swept the world. From China to Britain, It has shown itself to be an extremely adaptive system. Keep dreaming, kiddo.

Rob

July 10, 2015

Replying to rka19

Essentially it's a organization of cooperatives. However, there are still issues as i) it resides in a market system in which you need to make a profit to survive and ii) employees who are not owners have been increasing their numbers more so than employee-owners, thereby creating a two-tier system that will directly affect labor. Are there working alternatives to Capitalism? Yes. Has Capitalism been the most efficient and spurred the most economic growth of any other system? Absolutely. Per Churchill “It has been said that democracy is the worst form of government except all the others that have been tried.'

Jackie Munroe

July 10, 2015

Thanks for sharing the story of my great-great grandfather. When I tell people about the Coca-Cola millionaires, most either don't really believe me or they think it must be hyperbole. Just an aside, Daddy Pat's real name was Mark Welch Munroe, but everyone just called him Mr. Pat.

Patrick Amato

July 11, 2015

Great post and analysis. A good dose of rationale thought will help me and other investors fall for the siren song of speculative ventures

Jenny Kylan

November 23, 2016

What an amazing story. I had no idea about this. I was simply searching Google for what it is like to live in Quincy Florida and this popped up. Makes me wonder why my great grandparents didn't buy some too! Sure would make living a bit easier. 🙂 I actually own 2500 shares of Coke today, purchased 12 years ago. One of the best things I have done. I don't invest in tech that much, I do own some Google and Amazon, but that is it. Best to stay with what works like AT&T that just merged with Directv. That was a nice profit. Berkshire Hathaway Class B is also one to buy, you cannot go wrong with them. Stay away from Nestle, P&G, Clorox, L'Oreal, Bayer, Johnson & Johnson, Reckitt Benckiser and of course Monsanto. Those companies are volatile. Nestle has been stealing water from California for three decades. A state that has the strictest water restrictions ever, they are facing running out of water entirely and Nestle is stealing it, bottling it and selling it for profit. All of the companies murder over half a million animals a year with their bogus and barbaric animal testing and Monsanto now merged with Bayer are causing some species to go extinct, including the Monarch butterfly and bees. Something we must have to live. They are also killing humans with their carcinogenic pesticides and GMOs. Bayer is responsible for the distribution of the aids virus in the 1980s via the Manhattan NY Blood Bank (look it up). Nestle and P&G are also in trouble for killing people who try to stop them from deforestation and animal abuse in third world countries. It's a mess and must be stopped.

Thank you for posting this. I learned a lot tonight. 🙂