I Can’t Seem to Stop Myself from Buying Nestlé

I spent the past few days updating some of my own internal case studies, spreadsheets, and other documents, as well as wrapping up a few things that needed to be crossed off the agenda for the private businesses. I ended up putting together a collection of visual references covering some of the long-term holdings I keep for my household, among them Nestlé SA following my post on Monday. After looking at it, I realized I was being a complete fool by not buying more so I placed a second order on Tuesday and threw more shares into the portfolio.

Few times in a lifetime will one find a business like this. Few times in a lifetime can one say with relative certainty that it is at least trading at or below fair value, which appears to be the case at the moment. Given that I neither care about market fluctuations, nor the currency variability between the U.S. Dollar and the Swiss Franc, nor the fact the dividend is paid only once per year, my reluctance to buy more makes no sense. If the stock market collapses tomorrow, I’m willing to bet that I’ll still be happy over the next 25+ years at the prices I paid this week. Nestlé may not make sense for everyone, but for my particular situation, I should be locking more in the proverbial vault.

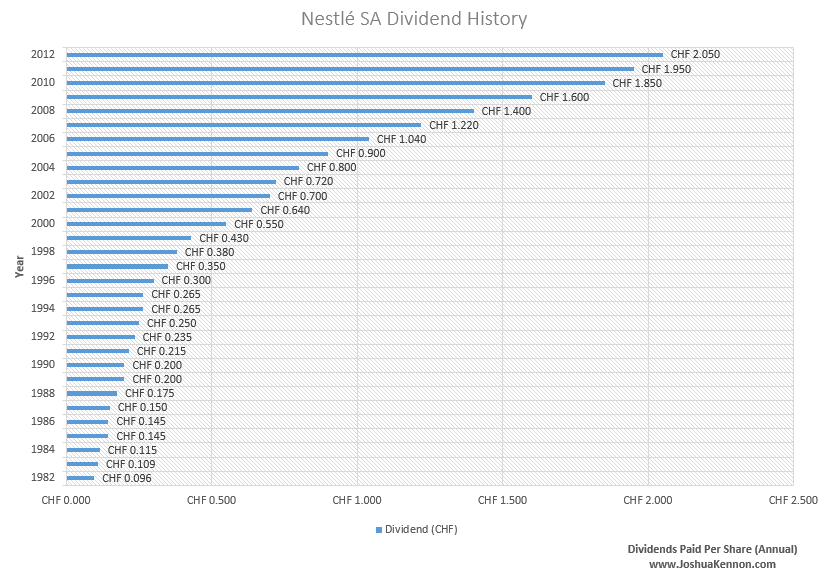

The ability of the firm to generate surplus returns on capital employed is just staggering. It shows up in the earnings and dividend record. One metric will illustrate this: When I was born, a single share of Nestlé paid its owners an annual cash dividend of CHF 0.096. As profits grew, so too did the money mailed out from those profits in the form of cash dividends to owners. For the next 30 years, the average compounding rate for the dividend was a bit more than 10.7% per annum, thanks to the food and beverage company’s ability to raise prices, launch new products, buy back its own shares, and fund acquisitions. This meant by the end of the period, your most recent dividend had reached CHF 2.05. Over the entire 30 year period, your annual payouts had grown by 2,135% without reinvesting a single one of those dividend checks (had you done so, your income would have been even more impressive and compounded at a much faster rate).

While you waited for this magical compounding machine to grow, you received cumulative cash of CHF 19.445 for every share you owned. That is money you could have spent, given away, invested elsewhere, or put into savings. As long as you never got rid of your ownership stake, as time passed, you were sent more and more money, the checks growing at a rate far in excess of inflation.

Look at it visually. This chart encompasses multiple wars, several recessions, the 1987 crash, the dot-com bubble, the savings & loan crisis, the Asian currency crisis, the September 11th terrorist attacks, the real estate bubble, the greatest economic collapse since the Great Depression, countless changes in the tax code, wildly different interest rate environments, and five U.S. Presidents serving nine terms. How can you care what the stock price does in a given year as long as your initial purchase price was attractive? All you have to do is sit down, be quiet, and collect your checks. That’s a wonderful first world problem to have.

It was an ordinary occurrence nearly every year on that chart to watch your shares of Nestlé rise or fall by 30% or more as buyers and sellers negotiated among themselves for what they were willing to pay for a piece of the company at any given moment. To the long-term owner, it meant nothing unless you wanted to take the opportunity to buy or sell more ownership. Profits kept rising, and the dividends rose alongside those earnings.

Once you had your hands on this ownership stake, you didn’t have to do anymore work beyond examining the annual report each year to determine if the business was still one you wanted to own; that you still believed had excellent economics; that you still thought would be earning more money in the future, while earning a fair return on capital in the present. You were free to go about your life without giving much thought to the firm as there were talented full-time managers running the place.

During those 30 years, you would have almost never seen this chart anywhere on television, in newspapers, discussed on the radio, or printed outside of the company’s own financial reports. The news focuses on what is happening at the moment – it almost never looks out and asks the question, “How does this matter to a long-term owner?”.

Even today, look up analyst coverage and news stories on the enterprise. Everyone’s talking about the next quarter, or year. Yet, everyone acknowledges that for the next generation the firm is probably a fantastic holding. Investment portfolios aren’t managed that way, anymore. People just want to know whether shares will be up or down relative to the S&P 500 this time next year. I don’t have a clue whether Nestlé will beat the index in the coming four quarters, but, again, I am willing to play what I see as highly favorable probabilities that it should make me a very nice return in the coming quarter-of-a-century.

I want more Nestlé. I will have more Nestlé. My current analysis may indicate a hypothesis that it could compound at only 7% to 12% long-term, but few things in life are that stable in terms of the internal profits and losses (again, the stock market won’t be that calm – the price of Nestlé shares is likely to fluctuate wildly, just like all other equities and there are always risk with any stockholding – while presently unthinkable, a company like Nestlé can go bankrupt, causing meaningful losses. That’s the nature of the world and the price an investor must pay for the potential returns generated by equities.). I have enough, other, high returning cash generators that I can indulge my desire to plant a few oak trees that, while they may grow more slowly, might very well pay off in a major way during my own retirement as well as when my future children and grandchildren inherit at least part of the estate.

I have to fund the pensions in a few months, as well as make some tax payments for the companies, but I think I’ll be able to keep constantly nibbling at the stock, picking up shares here and there as cash is generated by the other assets. I should be buying, not talking; writing checks, not posts on my blog.

Reader Comments (15)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Stanley

July 25, 2013

"Given that I neither care about market fluctuations, nor the currency

variability between the U.S. Dollar and the Swiss Franc, nor the fact

the dividend is paid only once per year, my reluctance to buy more makes

no sense."

The market fluctuation, I understand. The dividend being paid once annually, I understand. But why don't the fact that the exchange rate may change bother you?

Joshua Kennon

July 25, 2013

Replying to Stanley

A few reasons.

1. The intrinsic value of a multi-national of this size and scope often has its own internal counterbalances and hedges to currency risk. A firm like Nestlé surpasses a single nation - it generates its sales and profits in dozens of currencies and hundreds of countries. Even though the parent company figures are reported, and the dividends paid, in Swiss Francs (CHF), the underlying wealth is actually coming into the corporate coffers in U.S. dollars, Euros, pounds sterling, Swiss Francs, Hong Kong dollars, Yen, pesos, etc. This means that any fluctuation large enough to influence the relationship of the parent company's share price and dividend to the U.S. investor is also likely to influence the underlying earning power of the enterprise, acting as a sort of natural hedge.

Think of it this way: If the Swiss Franc collapses compared to the U.S. dollar, one would expect the share price and dividend to have less value to the U.S. investor. However, it would also mean all of Nestlé's sales and profits in the U.S. are now worth far more Swiss Francs, offsetting some of the situation, especially over time as the dynamics worked themselves out and management reacted to the shift. The opposite is also true.

This would be a very different story if I were looking at buying into a firm located in another country and that generated all of its sales and profits from that country. For example, a Swiss investor buying shares of Dr. Pepper Snapple Group, which generates most of its wealth in the United States and is reliant upon the United States currency, should be very aware of what the USD to CHF relationship is.

Likewise, if one were buying a firm in a country with non-stable economic policies, I would be concerned, but I think the Swiss Franc is a perfectly good long-term currency. In 2001, 85% of the voters approved an initiative that limited government spending increases to revenue increases. They're far more responsible than we are.

2. If I were looking for utility from my shares at some point, and the exchange rate were not favorable, I could always go to Switzerland and spend the money there. The world is so much more connected now, it's not like I'd have to translate the funds back to dollars and spend it in the U.S. If the situation were sufficient to justify, why not go all out and buy a house?. If, God willing, I'm still around half a century from now, I'd have no problem, present known factors considered, having a place halfway around the globe where my grandkids could spend the summers. People sometimes seem to act like this is some huge undertaking or some exotic dream - it's really not. It's a piece of land with a building on it. I'm surprised more Americans don't do it in the first place.

3. Over long periods of time, the currency relationship between two countries like the U.S. and Switzerland, though wildly volatile in the short-term, is fairly stable. If you go back and own a basket of blue chip stocks diversified across several countries for a 10 to 20 year time span, most of the vicissitudes end up with the odd effect of ending you up in nearly the exact same place you would have been had the portfolio been fully hedged the entire time. Of course, with a non-hedging strategy, you end up with, again, some insane volatility, but I don't care. Whether my shares look like they are up or down 50% tomorrow wouldn't influence my estimation of intrinsic value so I know what I'm getting.

I have no intention of living on or spending the cash generated by the shares for at least a few decades, radically reducing my need to concern myself with the short-term volatility.

Stanley

July 26, 2013

Replying to Joshua Kennon

I see, thank you for taking the time to explain it so clearly!

Gilvus

July 25, 2013

According to your dividend chart, the annual dividend grew more-or-less exponentially from 1982-2010 (11.14% CAGR) but from 2010-2012 grew linearly at a reduced rate (5.27% CAGR).

What gives? I checked the CPI numbers and annual inflation for the more recent period is only 34 basis points lower than 1982-2010 (2.61% vs. 2.95%, respectively).

Joshua Kennon

July 25, 2013

Replying to Gilvus

They're Swiss. They get conservative in the years in, around, and following a recession or major global period of slow growth, which isn't just limited to the U.S.. Look at 1984-1987 and 1989-1991.

In this case, part of the culprit is management's goal to hit the new target payout ratio, which is to be lowered to 55% of earnings. That means the dividend still continued to grow faster than inflation, but was throttled back a bit during the adjustment as the firm eased into the new payout structure, instead of doing it all at once. My suspicion is they will use it as a way to stockpile, or "cookie jar" earnings during good times so they can keep up the stellar dividend record when things get bad, affording to stretch the payout percentage back up to where it was. If the world slows down, they can still afford higher dividend hikes for several years as they have time to adjust, keeping up their credibility with the investment community.

They've made such good choices in the past (e.g., stepping in to buy Kraft's pizza business at a fair price, buying up large blocks of stock when the market was tanking while other corporations were too scared to act) that I don't mind. They've earned the benefit of the doubt. Who knows? They may want to pile up cash to be ready in case we enter another crash, buying up competitors. Until they give me a reason to doubt their commit to earning stellar returns on capital, I don't worry about it.

Gilvus

July 26, 2013

Replying to Joshua Kennon

I like how you use their nationality as an explanation for their conservatism :p But if their culture (national identity, even) revolves around this behavior pattern I guess it's not unreasonable to stereotype them.

I remember you replying to another reader's comment a while back, talking about Interactive Brokers. How has your experience with them been? I'm looking at their fees and I'm not sure if this $1 commission is real or not. I haven't delved into the fine print yet.

Joshua Kennon

July 26, 2013

Replying to Gilvus

You definitely have to factor in culture and national practices if you make international investments or you won't be able to compare the accounting records on an apples-to-apples basis (that's why I think domestic investments probably make more sense for most people, and hence my constant harping on a low-cost index fund being the most intelligent solution for almost everyone).

An example: Randomly pick a group of Swiss companies and then compare their depreciation policies to the United States. The difference is very substantial. They build these buildings that last longer, and are of higher quality, but then depreciate them down to nothing. If you actually look at the replacement value relative to the carrying value on the books, there are all sorts of assets that just aren't there for the Swiss company because the culture is much more conservative than it is in the United States when it comes to economic projections and business practices.

There is an old study put together by the best performing global mutual fund of the past couple of decades that talked about this (and actually used Nestle as an example, as it so happens). In a document titled What Has Worked In Investing, Tweedy, Browne's managing directors stated:

"For companies domiciled outside the United States, Tweedy, Browne has frequently observed depreciation policies that result in larger depreciation expenses, and lower earnings, than would be the case if the same company prepared its financial statements in accordance with U.S. generally accepted accounting principles. The Swiss company, Nestle, for example, reports as an asset on its balance sheet the estimated current cost to replace its property, plant and equipment. This is a significantly larger figure than the historical cost figure which would be required under U.S. generally accepted accounting

principles (“GAAP”), and results in higher depreciation charges versus U.S. GAAP.

Cash flow analysis and comparison to companies in the same industry will frequently suggest “hidden value” in the form of understated earnings and/or assets that have been written off to amounts which are significantly less than true realizable values."

My own experience has been similar. (The only notable exception to date has been UBS, which I could never get my head around despite working my way through 3-inch thick reports. I don't even think they know what risks are on their books.)

The British prefer a more private-business-like approach to dividend allocation - you can't predict what next year's dividend will be as the profits are tallied and checks sent out based on the current results (often, payments are annual or semi-annual, not quarterly). Meanwhile, here in the U.S., investors often demand four, equal, quarterly payments that never decrease and always go up every year, even if just by a penny; stability is rewarded. Things like that matter because all else equal, I'd expect a British company to cut its dividend before an American firm would. The former tend to treat it like a rational business owner who does what is best at the time, while the latter demand that the dividend be maintained come hell or highwater. That's why General Electric cutting its dividend was such a major event back in the Great Recession.

A great illustration is to compare Unilever PLC's dividend with Procter & Gamble's dividend. There is, perhaps, no starker illustration.

Gilvus

July 26, 2013

Replying to Joshua Kennon

This has been a very informative reply - one that may even deserve its own post! I sometimes wonder if only your regulars browse the comment sections, so maybe your other readers are missing gems buried down here.

Thanks for the reply and the tip on Schwab.

Donald Pato

July 26, 2013

Replying to Joshua Kennon

I hope that I have not missed this in one of your other posts, I've searched and read just about all of your archive; but what is your opinion on Schwab vs. Vanguard?

I have heard good things about Schwab's free checking account from frequent travelers because of the free global ATM perks. I've also heard fantastic things about their customer service. They have physical branches, some very low cost index funds- even some lower than Vanguard, IIRC.

On the other hand, I really like the stability and corporate ethos of Vanguard, but their customer service has not exactly blown me away in my (admittedly limited) dealings with them.

Would you share your thoughts, please?

ZaVodou

July 26, 2013

Hi Joshua,

I think Unilever is doing a good job, too. And as a british(dutch) company you don't have problems with the withholding tax.

What do you think?

Regards

ZaVodou

al

September 3, 2013

Joshua, since you've written multiple times about Nestle. I'm wondering if you had read about this: http://en.wikipedia.org/wiki/Nestl%C3%A9_boycott, what are your thoughts about claims of their unethical marketing in developing countries?

Best, Al

Joshua Kennon

September 4, 2013

Replying to al

I'm aware of it. I have no opinion on a boycott launched seven years before I was born, resulting from a written work published almost a decade before I took my first breath, and for which Nestle won a libel lawsuit in 1976 (and after which, the judge rightly urged Nestle to modify its advertisements).

This is especially true given that nearly all of the managers involved are either dead or retired.

Do I think the current advertisements are deceptive, claiming things like infant milk is the new "gold standard"? Yes. The gold standard is breast milk; a fact about which there is little debate, and which Nestle acknowledges. For those who are unable or unwilling to breast feed, high quality, nutritious infant formula produced in sterile factory environments is the next best option. The problem, of course, is that when dealing with poor, rural consumers in third-world nations, the proponents of breastfeeding say that the marketing creates a desire for them to westernize their children and break the family's budget, or worse, do something incredibly stupid like dilute the infant formula powder 2 or 3x as much as it should be with sewage-filled or contaminated water. So when a child dies because of some incredibly stupid action, Nestle somehow gets the blame.

Part of this is driven by the almost religious-like belief in breast milk. Personally, I prefer for kids to be breast fed, yet this isn't always possible. For example:

1. Many of the countries involved in the scandal are found in Africa, with HIV infection rates that are off the charts. The Centers for Disease Control states that these women absolutely should not breastfeed their infants as they risk passing on the virus to them.

2. Some women are incapable of producing milk. Coming from a huge family on both sides, and being in the Midwest, there are babies being born all the time. Most moms can breastfeed. I know one woman who tried so frequently, and so obsessively as she was an advocate for breast milk, but her body just wouldn't do it. She was bleeding all the time and her doctor finally yelled at her and told her to put the child on infant formula. Though it was normal throughout history, even 100 or 120 years ago, there isn't a snowball's chance in hell that women in wealthy countries are going to hire "wet nurses" given what we now know about biology and disease.

3. According to the Williams Institute at the Law School at UCLA (PDF), there are a whole lot of people in the United States who were raised by same-sex parents, presumably half of whom were male-only couples. Not to be flip about it, but male lactation, while is entirely possible, is not something that happens under normal conditions. That means you have millions of children that, quite literally, need infant formula to survive.

4. People forget how high the infant mortality rate was before Nestle introduced his baby cereal, which was designed to help children survive who weren't strong enough to feed naturally or weren't getting enough nutrition in the conditions that we now think unimaginable today; life really has progressed miraculously in the past two centuries. Though there were other factors at play, I think the evidence shows having sufficient calories for an underdeveloped child certainly improved probabilities for reaching adulthood compared to the alternative.

I think the currents scandal with PepsiCo mis-labeling its Naked Juice as an "All Natural" product when it was not, in fact, all natural, leading to a large financial settlement, much more problematic. Pepsi, a trusted name in food and snacks, lied to its customers.

As far as historical scandals within Nestle itself (which are always going to happen when you're talking about a firm measured in centuries, with subsidiary companies located in countless countries across the planet), I think Nestle's supply relationship with the Nazis, and use of slave labor during the war, was a much greater sin.

P.S. If you are interested in the actual article that started the boycott, and that Nestle won its libel suit against the author for publishing, you can see a PDF scan of it here.

al

September 5, 2013

Replying to Joshua Kennon

Thanks for your detailed response, Joshua. I don't disagree that infant milk is a beneficial development for the world.

From our perspective, the parents are doing something dumb and irrational by diluting the formula with unsanitary water when clearly breast milk is better. However, we're among the privileged to have this information available to us within a few key strokes of our keyboard. If this information isn't readily available while Nestle advertisements are readily available - I wonder if we can just say that the parents are behaving irrationally or whether Nestle does bear at least some of the blame for taking advantage of the situation?

I hadn't heard about the Naked Juice scandal, it looks like Pepsi took a $9M hit on the suit which doesn't look devastating. But I guess that you, as a part owner, are more concerned with how it tarnishes the brand.

Best, Al

Mark

October 13, 2013

Replying to Joshua Kennon

Josh, what broker do you use to buy Swiss or any other foreign stocks? I am thinking of using interactive brokers, but if you have a better idea, please share

Joshua Kennon

December 9, 2013

Replying to Mark

If you buy the ADR/ADS it doesn't matter as they are traded just like U.S. stocks. If you want the foreign shares directly, any brokerage firm with a good global trading desk should work; Interactive Brokers, Charles Schwab & Co., E-Trade, etc. I've heard very good things about Interactive Brokers but I can't speak from firsthand experience. Perhaps I'll open an account someday just to see it for myself.