Both the World and Capital Markets Feel Strangely Similar to 2006

For the past two or three weeks, I’ve found myself experiencing a strong sense of déjà vu. So many aspects of the world, and capital markets, today feel similar to the period following when Aaron and I graduated college; the time during which we built our early economic foundation. To give you just a brief sense of what I mean, consider we finished school in 2005. Thus, 2006 was our first full-year post-bachelor degree as independent, educated adults.

Housing is Almost the Same – Absolutely and Relatively – In Both Pricing and Financing Costs

- The median price of buying a home in January 2006 was $247,700, which on an inflation-adjusted basis is equivalent to $408,193 today. That puts it in the same ballpark as the median home price of around $405,300 as of the most recently available figures from 12/31/2025 as per the Federal Reserve Bank of St. Louis (with inflation adjustments performed separate via the Bureau of Labor Statistics).

- 30-year fixed-rate mortgages on January 5th, 2006 were 6.21% versus the most recent data from the day-before-yesterday of 6.38% as per the same source.

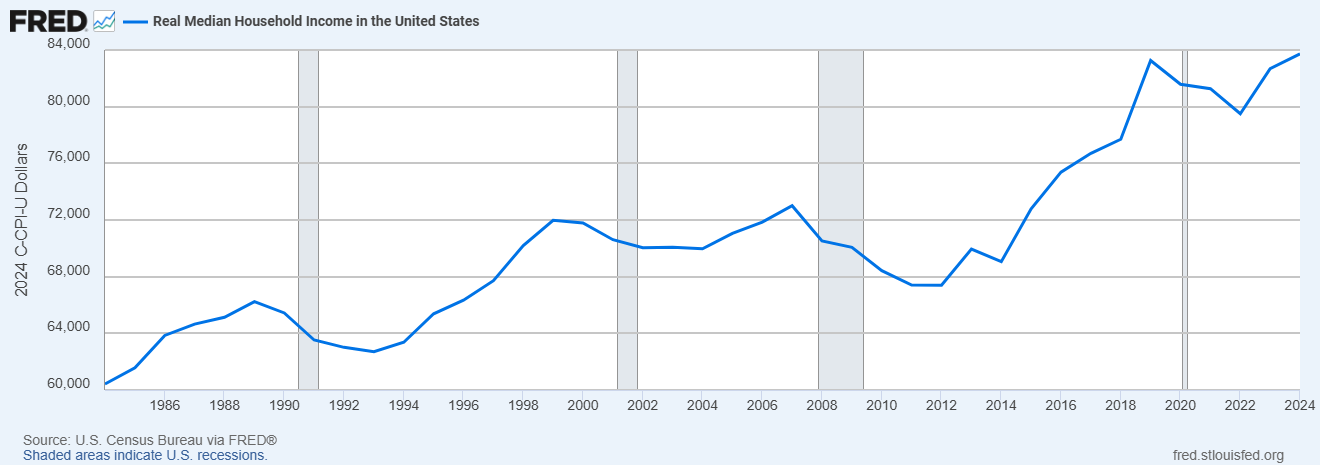

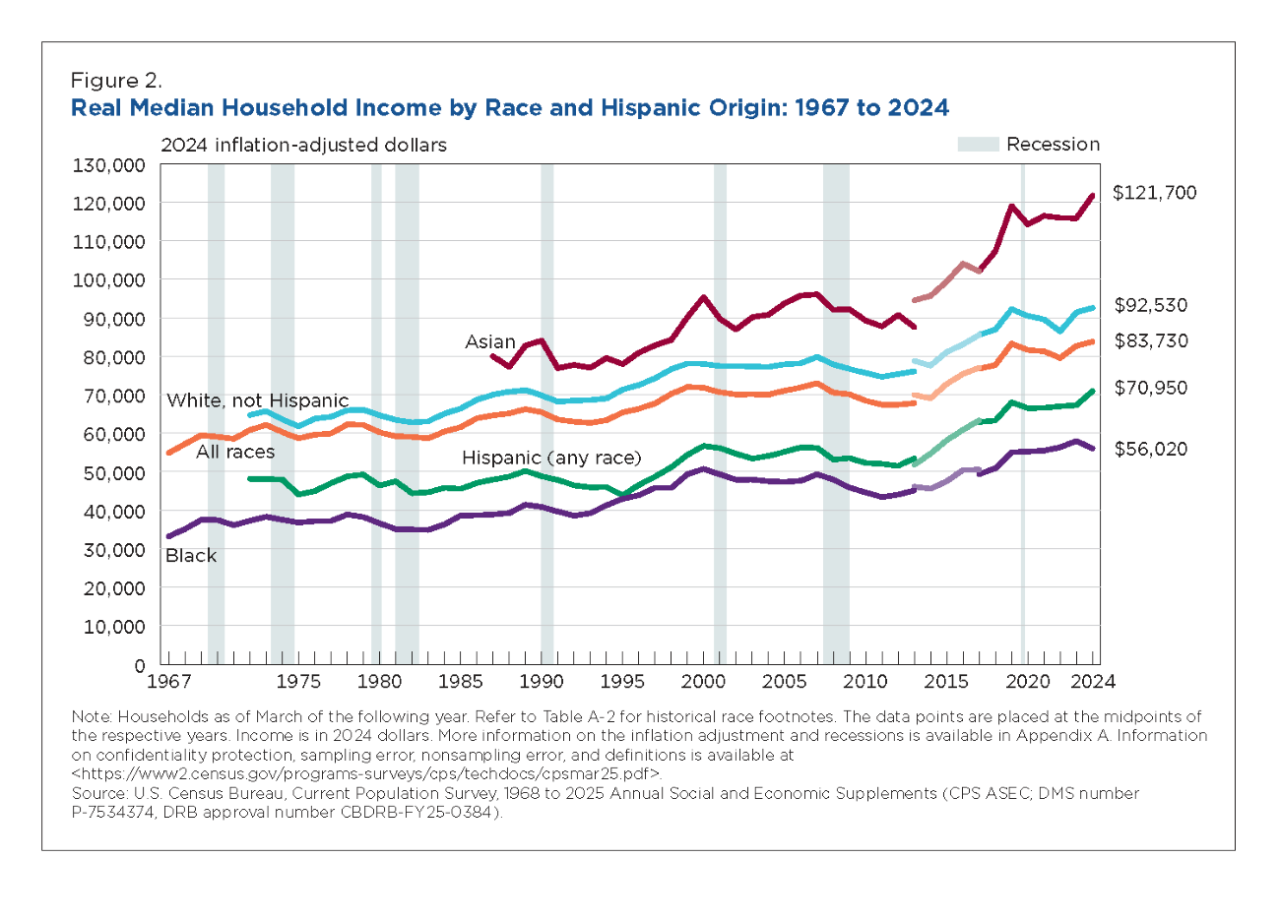

- Real median household income (that is, adjusted for inflation / cost of living changes) in 2006 ended at $71,850 versus $83,730 in 2024 (which is a year lagging due to reporting timing differences; the actual figure is higher than even that today), once again as per what is likely the best data source in the world.

We Were At War in the Middle East Causing Energy Prices to Spike

- The U.S. was boots deep in its ground war in Iraq and Afghanistan. Israel launched an offensive into the Gaza strip after Hezbollah fighters attacked, captured, and killed Israeli soldiers. Gasoline began January 2006 at $2.304 per gallon, which is $3.86 today. By July, it had spiked to $2.948 per gallon, which is equivalent to $4.73 today. You can see the data at the U.S. Energy Information Administration for yourself.

Employment Markets Were Tight

- In 2006, unemployment ran about 4.6%, whereas today it is doing better at about 4.0% to 4.2%.

Markets Had Some Strange Similarities

- There turned out to be some really attractive opportunities as the uncertainty unfolded in more conservative businesses.

- Silver and gold had spiked dramatically, going on a run that ultimately would continue for several years before then experiencing a lost decade in inflation-adjusted terms. (Interestingly, gold only recently exceeded its former inflation adjusted peak from back in the early 1980s. It had been great for trading, but horrific for those who just accumulated and held it rather than owning wonderful businesses. The opportunity cost was staggering.)

There Are Other Things, Too …

It doesn’t stop there.

There were fears in the public health sphere about declines in vaccination; e.g., hundreds of people contracted polio in India panicking global officials. Meanwhile, experts were terrified of a particularly bad strain of tuberculosis that resisted treatment which had appeared overseas. The technology landscape had some major stories in the news …

Amazon Web Services launched, Google was taking over everything, Facebook opened up to the general public.

Taylor Swift was making a name for herself breaking into the Billboard Top 100, where she still sits today.

The political environment had gone from neo-liberal progressive to more insular and regressive both at the Federal and state levels. The White House faced levels of disapproval that had been almost unthinkable in the past.

Schools in the Western World were moving back to phonics after certain areas had migrated away from it due to ideological capture.

It’s just very, very strange … the generalized sense of anxiety combined with seeing opportunities that get me very excited for the next ten years crossing my desk. Even the fear is so misplaced. The typical person is way too concerned about some of the news headlines while ignoring other things that are much more important. For example, it was a bit astonishing watching software companies start a sell-off recently after a single memo ran a thought experiment asking what would happen if A.I. (which really means large language models and is anything but) destroyed a good portion of white collar work within the next 24 months. The problem? No one placing trades, or writing in the media, seemed to stop for a moment to realize that even if people were able and willing to adapt to it so quickly, and if it were reliable without much supervision (it’s not – I cannot emphasize how terrible it is at complex financial analysis), there are half-a-dozen separate bottlenecks that make it physically impossible for it to happen on that timescale. (I mean it … physically impossible, as in the tangible real world. Hard drive sales are basically booked for the next year or two. RAM is experiencing substantial shortages. GPUs are impossible to come by. The energy grid cannot cope with that level of scale-up so rapidly. It. Could. Not. Happen. Even if we threw trillions more dollars at it as a society, it falls into that category that Warren Buffett once noted: “You cannot have a baby in one month by getting nine women pregnant.” Some things take time. The people living in this world have drunk the proverbial Kool-Aid.)

Fortunately, at work, I had been letting cash build up for a few quarters in most accounts. It’s time to start deploying money in a notable way. My staff has nearly every portfolio at the firm lined up in rotation for us to rapidly go through and begin rebalancing in the near future. I feel, strongly, that this is easily one of the top two or three moments in my career when an investor can buy an attractive amount of private income at conservative valuations with a good probability of future increases outpacing inflation. There are so many intelligent things to do right now even assuming, as I think one must, higher energy inputs acting as a drag for the next 36 to 60 months as the infrastructure will take time to rebuild causing artificially tight supply to persist beyond the end of conflict.

Even outside capital markets, where I spend my day-to-day … there are so many areas that are scalable; that don’t have barriers to entry they did when I was in my early twenties in 2006. The tools that a person can access today versus what was possible in 2006? My goodness. It’s so much easier now. The things I did in 2005, 2006, 2007 set me up for today. They built a foundation. There are so many people who will come out of this period and look back on it a decade or two from now as being the key to everything they’ve accomplished.

It’s strange seeing cycles repeat themselves. Ben Graham, directly and indirectly, used to write about the importance of assuming what has happened before will likely happen, again …