The Federal Reserve 2013 data detailing changes in household wealth, income, and other statistics is now public and you can go here to download the spreadsheet files and other resources or read the 41-page summary detailing the changes over the past three years since the last survey was released [PDF].

Here is a paraphrased summary of some of the highlights from the report:

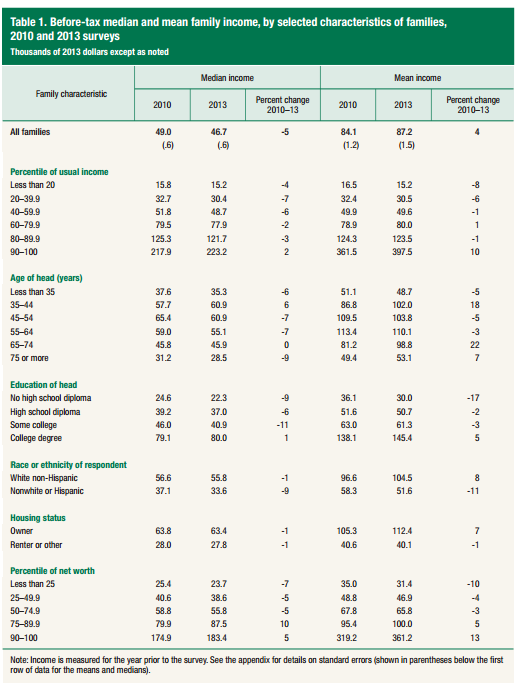

[mainbodyad]In the past 3 years, average family income rose by 4% inflation-adjusted but median family income declined 5% in real terms. That’s shocking. Meaning, if you are successful, you became more successful. Your salary is up, your dividends are up, your capital gains are up, your rents are up, more than offsetting the decline in your home value, but if you are an ordinary family, you have less purchasing power than you did as the bottom gets drug down by structural changes in the economy and the aftermath of the real estate bubble. We really are living through the equivalent of the Industrial Revolution. The hardest hit families were at the bottom, who are getting beat up pretty badly.

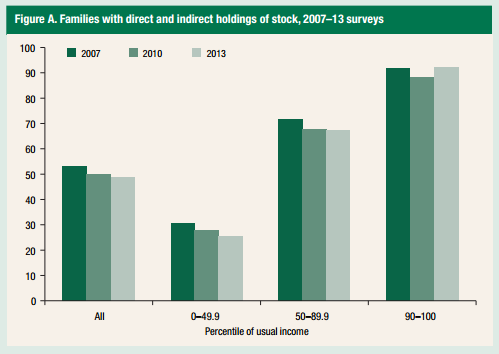

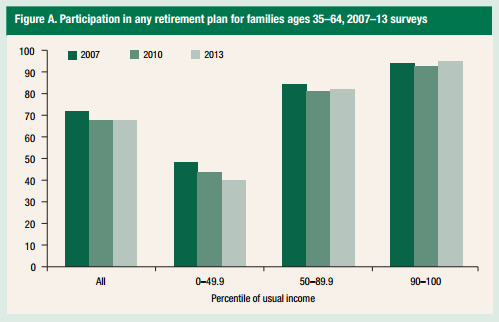

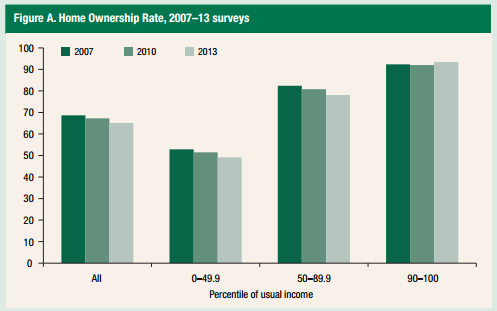

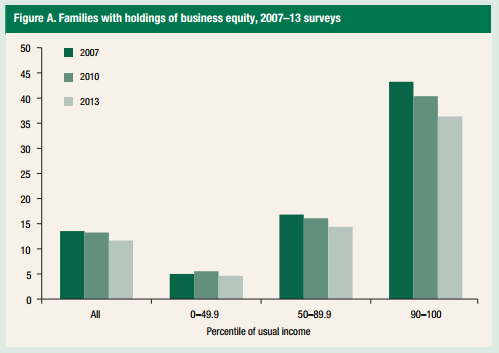

Ownership rates for businesses and homes fell substantially. Retirement plan participation fell. The bottom half of income cashed out of their holdings in a lot of cases, missing out on the subsequent gains.

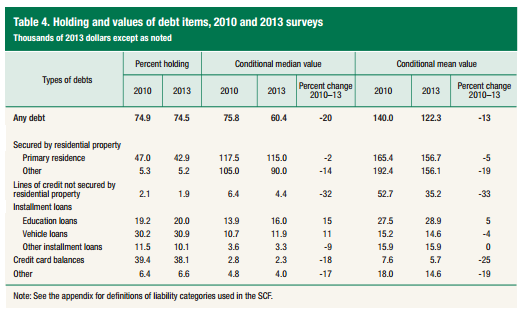

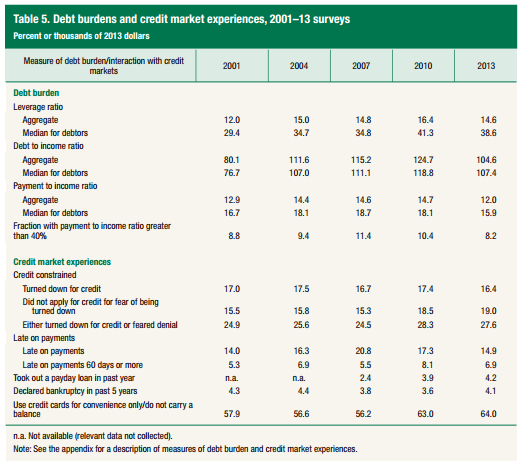

The good news? Debt has declined significantly. For families with debt, median debt declined by a shocking 20%, mean 13%. Debt burdens as measured by leverage ratios, debt-to-income ratios, and payment-to-income ratios also fell across the board. Families with payment-to-income ratios in excess of 40% are at the lowest level since before 2001. Those families carrying credit card debt decreased their median balances by 18% and mean balances by 25%, while the percentage of families opting to pay off their credit cards in full increased. Unfortunately, one debt type has gotten worse – student loan obligations – which are up “substantially” over the past three years.

The median income for the top 10% of society – literally, 10 out of every 100 families – is now $223,200 per year. Those in the next highest group (the top 10% to 20% of society) had a median income of $121,700. It’s crazy, but if you think about what this means, we now live in a country where roughly 1 in 5 families is earning six-figures a year or more.

Meanwhile, the bottom 20% – the other 1 in 5 families – is earning a median income of $15,200. I still don’t even know how that is possible. I can’t wrap my head around it.

The data doesn’t show what is easily identifiable from other sources – that a lot of this is due to the near total collapse of marriage among the poor and assortative mating among the successful. To put it into perspective, single moms account for 25% of U.S. households, single dads an additional 6% on top of that; an exponential rise since 1960. When you lose the economies of scale of two adults under a single roof, splitting your income and assets across different properties with double fixed expenses, utilities, etc., it’s like getting caught in an undercurrent. You cannot evaluate this data in isolation without looking at what is causing it. It’s not politically correct to say, there are always exceptions (including two U.S. Presidents in the past few decades) but if you choose to have children out of wedlock and remain unmarried, your odds of living, and staying, in poverty are exponentially increased. It’s almost a sure-fire ticket to poor town. Wedding rings are the new status symbol, far more valuable than a Bentley. Solve the marriage crisis and a lot – not all, but a very good chunk – of the poverty resolves itself.

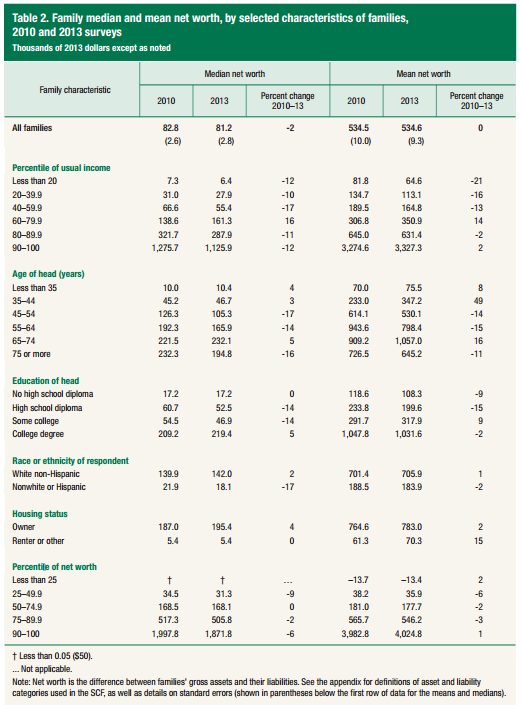

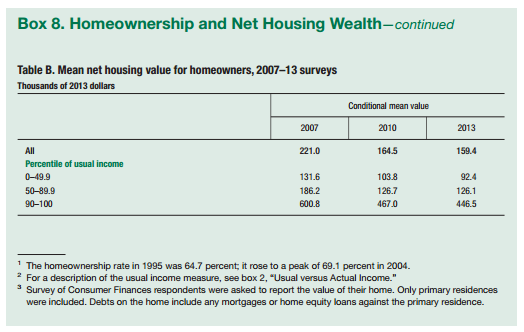

The median net worth of all families fell 2% to $81,200. The mean net worth remains the same at $534,600. Housing is to blame. People continued to fill in the hole created by the declining market value of their homes.

The numbers are just sickening to me. Almost everyone I know is earning way more money, with much higher net worths than they had three years ago. It feels like I live in a different universe. How can net worth be down for so many people since 2010? We literally just lived through one of the best possible environments for growing wealthy in the past 100 years. You could have been a complete idiot, had a low-paying job, and if you were even modestly frugal and had even a tiny bit of knowledge about valuations, seen that great companies were being given away for free. Real estate properties were being foreclosed. The only things that weren’t cheap were bonds and even they did well because they went into their own bubble driven by record low interest rates. This is just … unreal.

The decline in wages is one thing – cycles happen – but even if your income declines, your net worth should generally be going up with each passing year, adjusted for cyclical valuations in asset prices. If you earn $50,000 one year, $48,000 the next, and $46,000 the year after, you should still be richer at the end of year three than you were at the end of year one. After all, you brought in $144,000 during those 36 months. Some of it should have made it to the bottom line. If it’s not, and there isn’t a damn good reason (e.g., sudden medical crisis), you are running your estate very poorly.

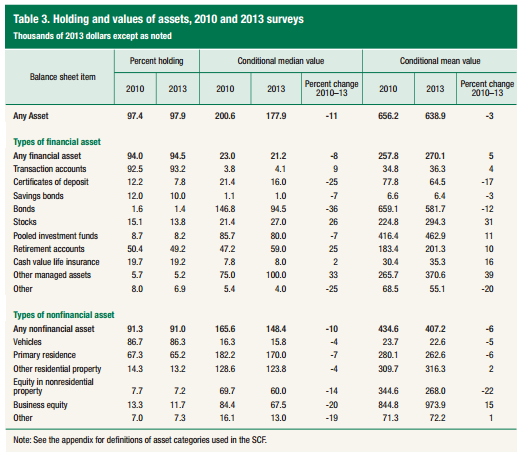

Here is the financial asset breakdown for families …

The families in the top 10% of income are far more likely than the typical American family to own shares of stock as an investment.

They are far more likely to participate in and fund a 401(k) or other retirement plan.

They are far more likely to own their own home, eschewing renting from someone else.

Really, again, a lot of it comes down to home values … bubbles are nasty, nasty things.

The top 10% are far more likely to hold ownership in a private operating business.

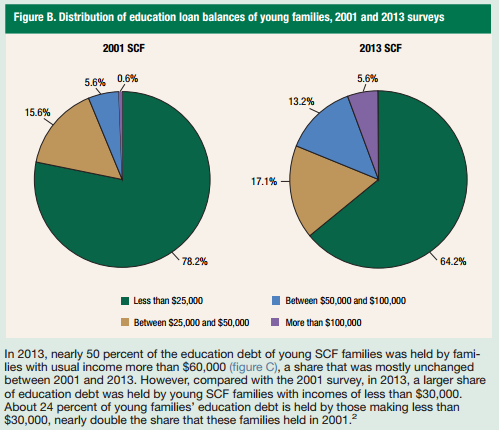

Here is a look at how education debt has changed over the past dozen or so years …

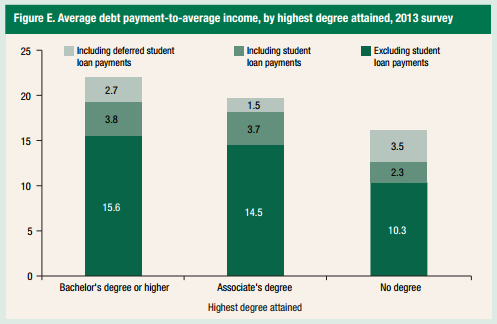

The amount of income devoted to debt repayment among recent college graduates is just horrifying …

Look at the debt ratios …

The payment to income ratio for the median household is 15.9%, which is much lower than it was in 2010. It looks scary, but it’s not quite as bad as it seems because a huge chunk of that is for mortgage debt, which is cheaper than renting on an opportunity cost basis if the valuation of the house was rational in the first place as measured by median household income to property value ratios. I still think it’s better for most people to live 100% debt free, though. If I were a guy working at a factory to support my family, I wouldn’t even have a mortgage on my house. I’d pay cash for used cars and be as frugal as possible to come up with any spare penny I could to buy commercial real estate or something to generate cash flow. Debt itself is often less than desirable, anyway, but it is especially toxic when used to fund non-cash generating assets. Just say no. Your life will be much better if you avoid the addiction, which is exactly what it becomes for most people. (I’m always amazed at people who say, “How can you survive without debt?” It’s a mathematically foolish argument. If you can’t afford $100, then you can’t afford $100 + interest. In some situations, you might end up paying 2 or 3 times the purchase price!) Do you realize how much easier life is when you aren’t paying rent on other peoples’ savings (which is all interest expense is – you’re literally renting the savings of other folks)? That’s all surplus purchasing power that now belongs to you and your family. It may require some painful times to get started but it snowballs into something really wonderful.

On the upshot, I suppose, if you are 35 years or younger, and have a net worth of more than $10,400, you are richer than half of all families in your age group. If you are 65-74, you need $232,100. For all families, again, it’s $81,200.

[mainbodyad]

Reader Comments (38)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

al

September 6, 2014

You say: "a huge chunk of that is for mortgage debt, which is cheaper than renting on an opportunity cost basis if the valuation of the house was rational in the first place as measured by median household income to property value ratios". My wife and I live in the bay area in California, where that ratio is just perpetually high (median property/median income is now hovering around 9.0). How should one think about it in such an environment?

AL

September 6, 2014

Replying to al

I don't do tenants or toilets so forget the rental for me--I do buy shares and shares in a few mutual funds that buy the greatest companies in the world. I just ran a hypothetical for someone using my purchase price in 1973 for the house I live in with a fund I own and buy monthly. Going back to my purchase price in the spring of '73 of $47,500 and assuming I invested all of that in the fund--the value as of 07/31/2014 was in excess of $5.8 million with all expenses and costs--that is a clean figure.

My house here in your nation's capital a few blocks from the METRO could be sold in a week for $800,000.

Now of course one has to live somewhere--one does leverage with a house--but one also has a myriad of expenses over 41 years--if you can buy, as Joshua has pointed out for years, good high quality companies that pay dividends that is an excellent way to generate wealth.

As I said above--I don't do tenants or toilets--but many have and many have had great financial success. Different strokes for different folks.

Grant Gentry

September 6, 2014

Replying to AL

Hey AL,

What do you think the likelihood is of your current house being worth $13.4 million in 40 years?? assuming same appreciation rates as last 40yrs that's where it would be. Your example of investing in stocks in '73 rather than real estate is amazing, going forward this probably be even more pronounced. Real estate prices in some areas on the coasts are beyond bubbles.

AL

September 6, 2014

Replying to Grant Gentry

Grant

Well, if you keep sending $ here and concentrating the power of the people here maybe prices will continue to move higher. We are pretty much recession proof as the pwer of the state continues to grow. It is goofy, but it is what it is.

Grant Gentry

September 6, 2014

Replying to AL

I suppose it's possible, by then America will be a 100% full fledged oligarchy. I'm going to stick with stocks. Have a great weekend

Joshua Kennon

September 7, 2014

Replying to al

The short answer? There is no good answer. Not in your situation.

In a handful of places like New York and San Francisco, the landlocked nature of the metropolis combined with a lot of outside, foreign owners, high-quality businesses, and mobile workers (people who relocate specifically to be near the city itself, the job opportunities, the universities, the cultural establishments), creates a significant distortion in the supply/demand equation so traditional valuation metrics decouple from market prices. This means there is an inherently speculative component to all real estate operations that isn't present elsewhere.

Assuming you live in San Francisco because of the job opportunities, meaning you are able to earn significantly above average income, the higher cost of living may still be worth the trade-off. If housing is 2x but income is 3x, it's still better to deal with the expense and stay in the area (even if they were at parity, if you just loved the place, it might still be a good lifestyle trade-off to stay in the area, acknowledging that you are choosing to spend money to be in a place you adore, which you value more than the cash and wealth it could later produce).

This means you are stuck in a city that, at the moment, is in a near ideal real estate environment. The economy for the demographics of San Francisco is knocking it out of the park, interest rates are at record lows, there hasn't been a major earthquake in decades, and there is only so much land. It's not like Kansas where you can keep building into the plains. That means any future appreciation is going to have to come from additional demand on the already constrained supply. How likely do you think that is to happen? That's the important question. Do you think it will be sufficient offset the inevitable rise in interest rates, which will, by necessity, result in far lower property values? It could be. It could not be. You have to think of it like any other asset you would value.

What about rent control? A significant reason behind the property value rise in San Francisco over the past 20 years was the implementation of rent control. Just like New York, rent control is one of those things that foolish, but well-meaning, politicians do because they failed basic economics. It always leads to a supply/demand distortion that ultimately causes prices to skyrocket out of control. Rent control effectively ends up being an all-out war on the poor and middle class. If the city ever comes to its senses and reverses its rent control policies, you'd eventually see a significant decline in real estate values relative to where they would have been as a more rational equilibrium were reached.

For me, if we were talking about personal, non-commercial, residential real estate in the form of a primary residence, I couldn't allow myself to take on leverage to buy an asset that I know is substantially overpriced relative to intrinsic value and that might be subject to considerable political risk. The median property is somewhere around $900,000 to $1,000,000. Even if I were paying half of that down, a rise to 1980 level interest rates or a regional recession could easily destroy all of those savings. I'd consider being fine with that if I planned on staying in the home for the rest of my life, giving myself time to ride it out, but only if I really knew I could remain there forever (job loss not affecting my family's ability to pay the mortgage) with no chance of foreclosure.

Alternatively, if I had a few million bucks in the bank, found a property I liked, and was willing to take the losses in a worst case scenario, I might just write a check for a property and decide it was worth it to my family. There are some things more important than money and if you find the perfect house, in the perfect location, and you pay too much for it, it's not the end of the world.

Absent those very specific, limited circumstances, I'd rent because it would allow me to sleep better at night. It's one thing to take on 5-1 leverage to buy a McDonald's franchise in San Francisco, a different thing entirely to buy a condo.

That's just me. That is what I, personally, could live with were I in those circumstances, you may be different. But part of this is, I know myself. If tomorrow, San Francisco sees property values double again, I wouldn't spend a single second upset that I had missed out the chance to make a lot of money from owning because I couldn't justify the holding based on the numbers. Therefore, it wouldn't have been a legitimate profit to me in the sense that it came from my skill. For a lot of people, seeing that subsequent rise they "missed", in their mind, would cause them a tremendous amount of misery. I'm not wired that way. I do what I can with the information I have at the time, then move on to the next thing.

But, yeah. If moving somewhere else wasn't possible for career or personal reasons, I'd be a renter in San Francisco under present market conditions because my inner investor wouldn't be satisfied with the risk/reward calculation of owning non-cash generating real estate. I think it's deranged. I feel the same way about New York at the moment, too, both renting and buying. If I were to move back to the New York area, there's no way I'd buy a property in the city at the moment unless it were the place I wanted to spend the rest of my life, regardless of the financial consequences. I'd end up buying a house in some place like Princeton or Short Hills, New Jersey.

al

September 10, 2014

Replying to Joshua Kennon

Yes, my wife & I are "stuck" here because our family and the software industry is here. But thank you so much for sharing how you'd think about this : you had even brought up things that we hadn't even considered.

SFrentier

September 13, 2014

Replying to Joshua Kennon

Josh, you said, "I couldn't allow myself to take on leverage to buy an asset that I know is substantially overpriced relative to intrinsic value..."

How do you value 'intrinsic value'? Why is a million dollar condo in SF (about the median) subject to more risk than a $150k condo in a fly over state?

In realpolitik terms, I think the expensive condo in a place like SF has more future security, not less. Unless you live here, I think it's hard to grasp. You mentioned some well know features of the Bay Area (landlocked, tech, desirability, etc.) but I think that the psychology of why people want to live here is even more germaine: wealthy and successful people want to be with others of their ilk, work in similar growth/success industries, etc. And wealthy outside investors follow too. Additionally, anyone who already brought here in the past has an asset base to leverage. The Bay Area has been "over priced" for over 30 years! Many who brought before the Great Recession are in good shape and can stay put or upsize.

I agree it's hard for new transplants and young people to get a footing here real estate wise. But if they want to stay here long term, I think it's imperative that they stretch and push hard to get into the best property that they can. It may mean living in a condo as opposed to an SFH. Getting a smaller place. Or choosing a less expensive community farther away. But that purchase can be your ticket to wealth. How many people that brought here 10 years ago regret the decision? Answer- not many.

I think it's difficult for people outside of the area to fathom that the median price of a home here is 4-5x the rest of the country, and that this must deflate at some point. My question, given the above, is why?

One more point. I disagree that eliminating rent control will kill prices in SF. Silicon Valley doesn't have RC and rents and housing are sky high there as well. Eliminating RC would probably temper the insane rent increases that we get in SF. To the tune of (literally) > 50% increase in 3 years! (My 2 BR places in the fashionable Mission district were renting for $2200 in 2010. Recently? $3600!) Owning non rent controlled properties in a rent controlled city is like printing money. I consider it a primary competitive advantage.

Feel free to respond.

Joshua Kennon

September 13, 2014

Replying to SFrentier

It's a little past two o'clock in the morning, so without getting too technical, here goes. I'm really tired so if I am less than clear, or sound too direct, or get a bit confusing, I apologize in advance. It's not intentional, I'm trying to keep my eyes open as I sit here with the MacBook and finish a few things.

The intrinsic value of an owner occupied residential real estate property is ultimately worth the discounted net present value of all rental payments that would have been saved were he unable to own a property and were forced to rent. (In fact, Congress in the United States has tried multiple times, the last time coming close in the 1920's if I recall correctly, to taxing citizens who owned their own house on the money they saved in rental payments as a form of income. Somewhere, in one of the file cabinets or bookshelves, I have collections of economic essays from the time period when these proposals were being pushed hard.)

This requires you, the investor, to look at the rental rates of a given community and determine if they are rational. How do you do that? It is determined by several variables in the intrinsic value calculation: 1.) Replacement or construction value which is itself influenced by, 2.) the risk-free interest rate, which influences the cost of debt and the opportunity cost of equity, 3.) the projection for supply/demand relationship, 4.) the ratio between median household income and median rental rates, which provides a rough gauge as to the sustainability of rental rates as things tend to fall apart once housing begins to cross 30% or so of normal family budgets, and 5.) the economic demographic projections for the area in which the housing market exists, including the major employers, industry projections, etc. (e.g., Detroit housing was inevitably tied to the sustainability of automobile manufacturing profits).

In an ordinary, free market environment, all of these things work together to create equilibrium so the best possible outcome happens in terms of allocating resources efficiently. Retirees who are no longer contributing goods and services to the economy are forced to move out, into cheaper housing elsewhere, younger families who are now earning more are able to more into larger properties to accommodate growing families, and you get this season-of-life recycling factor that generally keeps things more affordable than they otherwise would be.

Sometimes, you get a distorting effect such as rent control (more on that later) or living in a coastal city during a time when the currency falls in value and foreign investors begin buying up properties, distorting the supply/demand variable more than would exist based on the local situation. The point is, all of these things are constantly exerting themselves upon one another to set the free market price. Interest rates are among the biggest considerations because families shop for payments rather than property value; e.g., they look at how many dollars they can spend each month and then bid on housing until they have maxed out that allocation. If mortgage rates were 18% overnight, as they routinely were in the early 1980's, the value of most housing would fall by at least 50% instantly simply to accommodate this change. If mortgage rates went to 1%, property values would rise substantially, again, more than offsetting the median-home-value/rental-value-to-income ratios.

The rules of intrinsic value dictate that the price is the single most important determinant of the return the investor earns relative to ultimate cash flows. It doesn't matter if that asset is a stock (which is our primary focus it seems like around here), bond, real estate, copyright, or patent. That means the future desirability of a city is not the only things that matters. If I can get a $150,000 condo in a desirable Midwestern suburb at 2x median home values, 30% under construction replacement price, and a growing economic sector, it's a safer bet than a $950,000 condo in San Francisco with far worse metrics.

In other words, San Francisco as a city is almost certainly a better bet, just like Coca-Cola is almost certainly a better bet than Acme Random Drinks, Inc., is but that is secondary to the price one pays for an asset. Coca-Cola at 100x earnings is sub-par, despite being a safer long-term bet on a business-level, than Acme at 3x earnings, despite being a worse long-term bet on a business level. The same holds true for real estate.

The fact prices have been high for 30 years is not an economic justification for them remaining high forever. They might stay high for the next 50 years. They might increase further. They might collapse tomorrow. The point is, most rational, financially sophisticated economists who look at the numbers are going to conclude that the current price of property in San Francisco is above intrinsic value, meaning there is an inherently speculative component built into it, whereas properties in places like, say, Austin, Texas are not.

Billionaire Sam Zell built his entire real estate empire on this simple distinction. While others, like Donald Trump, were chasing high value properties in cities such as New York, Zell said screw it and went after apartment complexes across the country in Podunk nowhere, focusing solely on intrinsic value metrics. It's why he built more wealth, faster, and safer, than the rest of his competitors.

The thing that makes it challenging is that those who are financially sophisticated are dealing with 97%+ of the population who mistakes luck or variable timing difference or bubbles with being smart (the opposite is also true - you could have gotten a great deal and then seen a temporary market drop for five or more years despite none of it being your fault). If a smart person refuses to buy a property, and property prices double, the fools of the world go, "See?! You were wrong!", just like they did when stocks rose to a stupid 70x or 100x earnings following Jeremy Siegel's famous op-ed piece warning folks that equity valuations had become completely detached from underlying intrinsic value, which is all that matters.

I'm not sure how to respond to that because this is one of those things that virtually every well-known economic specialist in the country agrees upon as the numbers are straight forward: Rent control has the net effect of reducing the available housing supply and quality, thus resulting in net rental rates that are above what they would be in an ordinary market. In the absence of rent control, rental rates would eventually lower themselves to their equilibrium level, though that level is still subject to other variables (e.g., it's theoretically possible that another factor would be more than enough to offset the end of rent control so rental rates rose further but they would still be lower than they otherwise would have been).

Saying you don't agree with it is like saying you don't think gravity exists or that the world is only a few thousand years old. It's as close to settled in economic theory as you can get, so I'm not sure what I could say to convince you otherwise. I .... really am not sure what to do with that, kind of like if you wrote and said, "I don't agree that 2+2=4". ... okay? I guess? Maybe? Give me a peer reviewed model that refutes practically every other economist in history who has studied it and I'll consider your position? That's the best I can do.

I hope that clears up some of your questions. Again, I'm not re-reading this, proofreading it, or double checking it, so forgive any superficial errors. It's time for me to get some sleep =)

SFrentier

September 13, 2014

Replying to Joshua Kennon

Thanks for your response Josh. A few points, for I think we are coming from very different perspectives. It would be nice if they could find a common ground:

1- you are basically giving me a generic text book reading of intrinsic value, with little or no consideration of the actual market/product (in this case SF RE.) it's not a market you have intimate familiarity with, so I understand that. Just like I know little about collegiate varsity jacket business. But I'm sure you agree that besides business and economic theory, intimately understanding the myriad particulars and dynamics of your marketplace is what separates a successful business from a failure. Ole Joe with a high school diploma and 20 years industry experience (assuming he is bright and motivated) will probably run rings around Mr. green eared MBA grad trying to run the same business.

2- you should know that people (especially successful ones) largely decouple rent rate from home ownership. Where they choose to live has so many implications on their status, proximity to family, who they associate with, schools, amenities, lifestyle, culture, etc., etc. Plus they want to own their own home, not save a few bucks renting. This is deeply ingrained in our psyche. So expensive RE essentially is a competition among those with means to afford it. There are so many neighborhoods all over America (and globally) where home values are way over the rental to expense rate. This is proven over many years in all markets, not just costal. Of course you can be a multi millionaire and live like a king in a great area of Kansas City, and I'm sure there are plenty of those. BUT, there are way more multi millionaires living in places like SF, Manhattan, Hong Kong, London, etc., etc., etc. Most successful and well off people want to live where they want to live, and (pardon my french) don't give a flying fuck about discounted net present value of all rental payments that would have been saved. But in addition to that, they have repeatedly made a lot of money in RE in these mentioned markets.

3- As for myself, an active RE investor in the SF market, I do not buy at retail to just park my money (like many wealthy outsiders do who made their money elsewhere.) I ferret out the areas about to gentrify, get in early, wait for a good deal going in, develop the property and add value, optimize tenant situations (a profit center in its own right due to nutty rent control here.) I have only made a few acquisitions, and they have taken about 2 years to get to highest and best use, but they have all been major home runs. I can afford to loose substantial equity as well as rental income and still be ahead, if and when SF goes the way of Detroit. But I shouldn't have to. Detroit's demise was 30 +years in the making- late 70's OPEC oil embargo, smaller Japanese cars, lazy US auto makers (care to buy a Ford Pinto, or Chevy Nova?), etc. RE Investors had plenty of time to pull back or out of Detroit over the last 30 years.

4- you're right about Sam Zell and his successful value buying, although he also quickly 'traded up' to Equity Office in all sorts of prime locations. But, most buy and hold investors that make bank in RE are doing it in prime markets. If you're buying a lot of cheap doors in the mid west, it's going to take a lot of them (and a small army to manage them) before you're seeing the big bucks. The bottom line is that wealth is created in RE through equity appreciation, not cash flow. Cash flow pays the bills (and must be managed), but appreciation will make you rich.

5- about rent control. Of course I know the theory and fully agree. I think we're saying the same thing here, as I already took into account the outstanding variables you mentioned that would (still) push on SF rents. And I also stated that the crazy 50% in 3 years increases would probably subdue...may only 20% in 3 years, which is still awesome, of course 🙂 Again I'm speaking from very specific SF market knowledge, but taking the theory into account. (FYI, no city would ever just drop RC; it would only be phased out, so the effects would slow back into the market.)

I respect your perspectives and realize they differ from mine, but it would be interesting to see if we can find common ground too! Cheers,

RogerMKE

September 6, 2014

"If I were a guy working at a factory to support my family, I wouldn’t even have a mortgage on my house."

The problem is that you have to live somewhere, so you're either making your own mortgage payment, or you're making someone else's. Few factory workers can simply pay cash for a house.

I think a more optimal strategy is to buy a small rental property, living in one unit while the other unit(s) makes the mortgage payment. For example, here in Milwaukee you can buy a nice 3-BR duplex in a decent blue-collar neighborhood for $150K. Assuming 10% down, your payment including taxes and insurance would be about $1,100 month. You can rent the other unit for $850.

That means our factory worker is living in his own home for $250 a month out of pocket (less than the property taxes on a free and clear home), all while accruing the tax benefits of home ownership, seeing his mortgage paid down by $100 a month, and hedging against inflation. Further, if he decides to move he could keep the property and turn a tidy profit each month.

With a 4% cost of capital, applying a little leverage to a low-risk investment can be quite compelling.

david

September 6, 2014

Replying to RogerMKE

I had the same initial thought, but I just assumed he would rent somewhere cheaply and invest, rather than purchase a home at this point.

Your example is actually one I have seen elsewhere that makes a lot of sense for someone who wants to invest, but is in sort of a difficult position income wise. With an fha loan, you can get the down payment lower than your 10%. Although, I wouldn't consider 9:1 leverage "a little".

Also, of considerable importance, is the structure of such a mortgage on a duplex or fourplex that you are going to live in/invest in. In certain states, purchase money mortgages are considered non-recourse and if, God forbid, you had to foreclose, they could not seek a deficiency judgement due to the purchase money aspect, and that you lived in it. Investing in a duplex/fourplex that you live in is one of the few ways to acquire rental real estate in a non-recourse way (state-dependent). Just a thought...and I'm not a lawyer.

More info if you're interested - http://www.forbes.com/sites/jayadkisson/2012/06/24/foreclosure-deficiency-judgments-and-the-perils-of-anti-deficient-statutes/

Joshua

September 7, 2014

Replying to RogerMKE

This isn't a bad strategy. If you qualify for FHA or VA funding then you only 5k or less for a downpayment. That's very doable in 1-2 years on a working class salary. Of course you're paying PMI with an FHA loan, so that makes your cost of capital a little higher.

Joshua Kennon

September 7, 2014

Replying to RogerMKE

That would definitely be worthy of consideration. The person I envisioned was in the middle of his career, by which point I'd have repaid the mortgage even if the cost of capital were low as the incremental profitability gain would have less utility to me than the peace of mind of knowing that even if we went into a Great Depression, no one could take my duplex from me. Another option I've seen work for several business owners is building a small apartment above or adjacent to their shop during the early years, allowing them to live very cheaply, freeing up more money for growth. You used to see it a lot more often - the baker who lived above the bakery - but it has fallen out of favor in the past 50 years.

Personally, I'd still probably opt for an all-cash deal if I were poor and starting out as I'd want money for businesses, where I could expand the capital very quickly without the risk of leverage.

A real world example of what I'm thinking: A family member of mine decided as a side hobby to begin buying rental properties and was able to get a house valued at $60,000, listed at $30,000 in foreclosure, for $15,000 by making a direct offer to the banker to write a check on the spot. (Value investing is not just for stocks.) It's modest, but in a decent neighborhood. It is basically something equivalent to a listing like this one in one of my family's original hometowns. I'd live in it and have no housing payment, then when my fortune had grown a bit, I'd turn it into a rental property. The particular property this person bought will rent for $500 to $600 per month based on all the other houses around it. Even with several thousand dollars in planned upgrades, they will be able to collect somewhere between a 30% and 36% cap rate on an all-equity deal.

During the years I lived at near no-cost in the house myself, every waking hour would be devoted to creating, acquiring, or managing for a fee a collection of cash generating assets, all debt-free and isolated from one another in case things went south. My first major milestone would be to get to where my passive income exceeded what I could earn at the factory, none of which was ever spent by my family, but rather reinvested. That way, if I ever lost my job, I could switch over to it as the income source while searching for another one. Following such a system, it would be almost impossible not to end up a millionaire over a couple of decades.

Paul

September 7, 2014

Replying to Joshua Kennon

Hi Joshua, long time reader, first time caller. Could you clarify the last paragraph? Specifically the following:

- creating, acquiring, or managing for a fee a collection of cash generating assets

- debt-free (I'm assuming this means something like buying a rental property for cash?)

- isolated from one another

Thanks!

david

September 7, 2014

Replying to Paul

Hey Paul, not Joshua, but I think you might find the comments section in these 2 articles very useful. Both gems.

https://www.joshuakennon.com/unemployment-is-only-4-8-if-you-are-a-college-graduate/ ( His point 9. in the comments )

https://www.joshuakennon.com/mail-bag-how-would-you-convert-a-pile-of-money-into-passive-income/

david

September 7, 2014

Replying to Paul

Also, I forgot to mention this article below, which is great, especially the part about thinking of your capital as building scaffolding. Getting to that first 500,000 really is the greatest challenge in my mind in becoming wealthy.

https://www.joshuakennon.com/mail-bag-starting-to-earn-income/

In the beginning of your wealth journey, you can work a lot harder than your money, so it basically pays to be clever and go where you can have an edge rather than simply providing capital and levering up.

_____________________

The comment from joshua below really brings home the importance of the scaffolding aspect in the beginning.

"I don't know of very many people that think that way. Invariably, they say, "I want to sell ice cream because my town doesn't have an ice cream parlor." That may be true, but a lot of the return from a store like that comes from the total capital invested. If you don't have the cash, you would have to rely too heavily on the leverage component of ROE and would be subject to wipeout in an economic downturn whereas someone who had a lot of extra cash could easily make money with an ice cream parlor.

My risks were always greatly reduced because I looked at the ROE components *relative to my own personal opportunity costs and resources at the time*. That is absolutely vital, I think."

source: https://www.joshuakennon.com/a-mental-exercise-what-id-do-if-i-lost-everything/

Good Luck

-david

preston nelson

September 8, 2014

Replying to Paul

I think David has you covered on your answer. One thing I'll throw in that I don't think is covered is that in many states this management of properties -for others- requires a real estate type license.

SFrentier

September 13, 2014

Replying to RogerMKE

That's a fantastic strategy. I smile every time I meet a blue collar worker, police officer or fire fighter that has built equity in RE through that method. They usually get 30 year fixed loans, and in CA they are always (or almost always) non recourse. Never heard of a homeowner loan here being recourse, if it's from a standard bank. I think it's state law. YMMV in other states.

Andrew

September 6, 2014

I strongly believe there's a double standard in the legal system regarding marriage.

The legal system seems to hate men. I'm a man, so I will not be getting married anytime soon (or ever). Even though I love women and am a one-women type of guy. I'm pretty sure A LOT of guys feel this way now, hence the lowering marriage rates (IMO anyway).

Brendan

September 7, 2014

Replying to Andrew

Implicit in this statement is that every woman will drag her husband through the legal system...which is not the case.

Andrew

September 8, 2014

Replying to Brendan

It's simple risk assessment. Marriage failure rates are quite high.

It's not women themselves, many people are sue happy now a days. The legal system just seems to give the advantage to women. It's mostly just the numbers of it all and the significant impact failure would have.

Maybe I'm naive and missing something, maybe I'm not giving the advantages enough thought, but this is just how I personally feel about it. It feels (as of right now) like the risk outweigh the benefits.

Mr.owenr

September 6, 2014

I like to read these blog posts and wonder what I'm doing so wrong, since I earn just over 10k a year as an associate at Walmart. They make me question where my thinking has led me astray.

Joshua

September 7, 2014

Replying to Mr.owenr

Dig into the blog. You'll find hundreds of sources of inspiration as well as practical advice on how to maximize your time and money.

Mr.owenr

September 13, 2014

Replying to Joshua

Yes I enjoy this blog. It talks about how all forms of capital can be exchanged one for another. I also believe I read where Joshua made $100,000 a year when in college. This means that in his college days Joshua had roughly ten times more capital (intellectual capital, skill capital, etc) then I currently possess. (I am assuming that when he tried to get financial capital he did so as best he could.) I may not always like where Joshua's conclusions take me, but I enjoy learning from his wisdom nonetheless. It is because of this blog that I've started reading Security Analysis 6th edition, and I am hopeful that the knowledge capital to be gained will translate into financial capital at some point in the future.

david

September 7, 2014

Replying to Mr.owenr

You can only go up from here. The first essential, it to think of your free time as opportunity time. Not time to waste. Wealth is created in what most people consider to be their free time to piddle away doing whatever activity they like. Fine, but don't get angry when you're poor at 65. You'll notice Joshua seems to play a lot of video games, but he sure as hell worked his butt off in the beginning - or atleast balanced it out with big spurts of work - Most people fail because they forget the "work" part.

Then, start investing in yourself (learn an in demand skill, etc.) as you can probably get a higher return on your human capital starting from where you are, than trying to make it through investments initially.

Good luck

Mr.owenr

September 14, 2014

Replying to david

Thanks, this seems like a step in the right direction.

Joshua Kennon

September 7, 2014

Amen, amen, amen. I should have clarified that my objection is largely to recourse debt. If you could isolate debt in a specific entity that couldn't get back to you, and you thought the risk/reward payoff was worth it, I would consider leverage acceptable in certain circumstances as long as the loss of equity in the project wouldn't set you back too far. I don't mean things like now-defunct hedge fund Long Term Capital's capital allocation policies, obviously, but I'd be far more likely to take on liabilities if I could keep them contained in the event of an emergency and they were still modest relative to equity.

Part of this, though, is the nature of debt. It's not the best form of leverage. If I were really going to shoot for the fences and take on the possibility of huge losses, you'd get a lot more bang for the buck using something like derivatives. Were I to ever lose my mind and bet it all on red or black, I'd do it in a way that gave a 50-1 or 100-1 payoff, not a 2-1 or 3-1 payoff.

Matt

September 7, 2014

Replying to Joshua Kennon

Could you explain why debt isn't the best form of leverage?

(My guess is that it has to do with people's aversion for long-tail events and hence their willingness to overpay for insurance against them, which would result in better risk-adjusted returns for the sellers of derivatives. Is this your general thought?)

Joshua Kennon

September 7, 2014

Replying to Matt

If we are talking about speculation or the desire to gain a lot of scale very quickly, debt generally isn't toward the top of the list in terms of ideal leverage from the perspective of you, the person who wants to make a lot of money.

Imagine you were the guy who started Comfort Inn. If you had tried to build out your hotels one-by-one yourself, you would probably still be a regional player not many people knew. If, instead, you franchised (a form of leverage by using other peoples' money in exchange for a cut of the profit while you take a royalty), you can scale the parent company very quickly without the bankruptcy risk. If a specific hotel gets in trouble, the franchisee might go bankrupt, and you'd be out the royalties for a given period of time, but you aren't the one on the line. Even better, nearly every penny coming into the treasury is free cash flow as you don't have a lot of reinvestment needs. You're not the one who owns the building. It's a lot easier to get very rich very quickly with a system like this than it would be to borrow money and try to build it yourself. The franchise contract is a superior form of leverage.

Imagine you had $1,000,000 in a brokerage account. You decide you want to buy 100,000 shares of GE at $26.10, so you borrow $1,610,000 on margin, bringing your account asset value to $2,610,000. If you're right, and the stock doubles, you make a profit of $3,610,000 + any dividends received - any interest paid - any taxes owed. That's a great return, even though you exposed yourself to a very real possibility of losing every single penny - a single bad year in an otherwise ordinary stock market would have wiped you clean off the board, so it's a stupid way to behave.

If, instead, you bought January 2016 call options on GE shares, paying $0.55 per share for the right to buy 200,000 shares. Your cost is $110,000. At the end of that 16 month period, if you haven't used your option, they expire worthless. You park the other $890,000 in a money market account at your local bank, which will pay you 1.00% based on that balance. At the end of the period, you'll have just shy of $902,000 in the money market account before taxes, generating a return of $12,000 pre-tax.

If GE shares double under this second scenario, at the end of the period, you would have

If we are talking about speculation or the desire to gain a lot of scale very quickly, debt generally isn't toward the top of the list in terms of ideal leverage from the perspective of you, the person who wants to make a lot of money.

Imagine you were the guy who started Comfort Inn. If you had tried to build out your hotels one-by-one yourself, you would probably still be a regional player not many people knew. If, instead, you franchised (a form of leverage by using other peoples' money in exchange for a cut of the profit while you take a royalty), you can scale the parent company very quickly without the bankruptcy risk. If a specific hotel gets in trouble, the franchisee might go bankrupt, and you'd be out the royalties for a given period of time, but you aren't the one on the line. Even better, nearly every penny coming into the treasury is free cash flow as you don't have a lot of reinvestment needs. You're not the one who owns the building. It's a lot easier to get very rich very quickly with a system like this than it would be to borrow money and try to build it yourself. The franchise contract is a superior form of leverage.

Imagine you had $1,000,000 in a brokerage account. You decide you want to buy 100,000 shares of GE at $26.10, so you borrow $1,610,000 on margin, bringing your account asset value to $2,610,000. If you're right, and the stock doubles, you make a profit of $3,610,000 + any dividends received - any interest paid - any taxes owed. That's a great return, even though you exposed yourself to a very real possibility of losing every single penny - a single bad year in an otherwise ordinary stock market would have wiped you clean off the board, so it's a stupid way to behave.

If, instead, you bought January 2016 call options on GE shares, paying $0.55 per share for the right to buy 200,000 shares at $30.00 per share, which is above the current market price of $26.10 per share. Your cost for this contractual right is $110,000. At the end of that 16 month period, if you haven't exercised your options, they expire worthless. You park the other $890,000 in a money market account at your local bank, which will pay you 1.00% based on that balance. At the end of the period, you'll have just shy of $902,000 in the money market account before taxes, generating a return of $12,000 pre-tax.

Oversimplifying it a bit before taxes, if GE shares double under this second scenario, you're going to enjoy a $22.20 gross profit on each of those 200,000 shares, for a total pre-tax profit of $4,440,000. In addition, you still have the now $902,000 in your money market account, bringing the total to $5,342,000 before taxes.

The option approach allowed you to use only 11% of your account balance to speculate on a huge move in the stock, with a far higher payout, while protecting the other 89% of your money. It's still a stupid trade - this is about as close to animalistic raw gambling as you can get in the stock market - but the risk/reward/return numbers are much more attractive. One of the reasons is if there were a flash crash or something, your margin debt could be instantly called and your position wiped out, whereas the call options are owned outright. There is no possibility of a margin call. You paid for them in full and even if they sit near worthless, as long as they haven't expired, they could theoretically recover. In this case, someone with a penchant for gambling would be much wiser to structure the deal using the derivatives rather than outright debt.

Imagine you wanted to buy up real estate in your home town. You're going to be much better off setting up a real estate entity, raising money from investors, and taking a percentage cut of either the assets, cash flow, or both. Even if the entity itself uses debt to finance the purchases, you, the person trying to make a lot of money, aren't exposed to the downside of debt as if you had tried to buy it yourself.

There are some times that debt is the best option. If you own a manufacturing plant with good returns on capital and find yourself in a low interest rate environment, it can make a lot of sense to borrow on long-term fixed-rate conditions to purchase machinery, which you then get to depreciate, that will earn exponentially more. Yes, it introduces an element of risk but you can do very well if you are conservative so that even a 90% drop in sales won't force you to the courthouse steps.

Likewise, if you see a piece of real estate property you know can be very valuable - one of those few-times-in-a-lifetime chances to grab something strategically great - buying all of it yourself can be worth the risk if you know what you are doing.

But generally if you want to take advantage of a force multiplier of some sort so that you enjoy higher profits than the underlying operation itself would otherwise generate on a pure equity basis, there is a way for you to structure the terms so that you get a fair but disproportionate percentage of the outcome. I mean, Warren Buffett is famous for not using debt but his investment partnerships, and later insurance companies, were really just leverage accounts in drag from his perspective as the operator. He was able to enjoy outsized returns for every dollar in subsequent gain. I can't recall exactly off the top of my head but I think the stocks within Berkshire Hathaway's insurance conglomerates have only compounded at something like 11% or 12% the past couple of decades, which translates into far higher returns on book value because of this leveraging effect. It's about the structure. Structure is just as important as any other variable and the one people don't seem to pay attention to often enough. A good deal can turn into a bad investment if you get the structure wrong, and a bad investment can be salvageable if you structure it correctly.

Joshua Kennon

September 7, 2014

Replying to Matt

If we are talking about speculation or the desire to gain a lot of scale very quickly, debt generally isn't toward the top of the list in terms of ideal leverage from the perspective of you, the person who wants to make a lot of money.

Imagine you were the guy who started Comfort Inn. If you had tried to build out your hotels one-by-one yourself, you would probably still be a regional player not many people knew. If, instead, you franchised (a form of leverage by using other peoples' money in exchange for a cut of the profit while you take a royalty), you can scale the parent company very quickly without the bankruptcy risk. If a specific hotel gets in trouble, the franchisee might go bankrupt, and you'd be out the royalties for a given period of time, but you aren't the one on the line. Even better, nearly every penny coming into the treasury is free cash flow as you don't have a lot of reinvestment needs. You're not the one who owns the building. It's a lot easier to get very rich very quickly with a system like this than it would be to borrow money and try to build it yourself. The franchise contract is a superior form of leverage.

Imagine you had $1,000,000 in a brokerage account. You decide you want to buy 100,000 shares of GE at $26.10, so you borrow $1,610,000 on margin, bringing your account asset value to $2,610,000. If you're right, and the stock doubles, you make a profit of $3,610,000 + any dividends received - any interest paid - any taxes owed. That's a great return, even though you exposed yourself to a very real possibility of losing every single penny - a single bad year in an otherwise ordinary stock market would have wiped you clean off the board, so it's a stupid way to behave.

If, instead, you bought January 2016 call options on GE shares, paying $0.55 per share for the right to buy 200,000 shares at $30.00 per share, which is above the current market price of $26.10 per share. Your cost for this contractual right is $110,000. At the end of that 16 month period, if you haven't exercised your options, they expire worthless. You park the other $890,000 in a money market account at your local bank, which will pay you 1.00% based on that balance. At the end of the period, you'll have just shy of $902,000 in the money market account before taxes, generating a return of $12,000 pre-tax.

Oversimplifying it a bit before taxes, if GE shares double under this second scenario, you're going to enjoy a $22.20 gross profit on each of those 200,000 shares, for a total pre-tax profit of $4,440,000. (Your only expense was $0.55 per share, or $110,000 in total.) In addition, you still have the now $902,000 in your money market account, bringing the total to $5,342,000 before taxes.

The option approach allowed you to use only 11% of your account balance to speculate on a huge move in the stock, with a far higher payout, while protecting the other 89% of your money. It's still a stupid trade - this is about as close to animalistic raw gambling as you can get in the stock market - but the risk/reward/return numbers are much more attractive. One of the reasons is if there were a flash crash or something, your margin debt could be instantly called and your position wiped out, whereas the call options are owned outright. There is no possibility of a margin call. You paid for them in full and even if they sit near worthless, as long as they haven't expired, they could theoretically recover. In this case, someone with a penchant for gambling would be much wiser to structure the deal using the derivatives rather than outright debt.

Imagine you wanted to buy up real estate in your home town. You're going to be much better off setting up a real estate entity, raising money from investors, and taking a percentage cut of either the assets, cash flow, or both. Even if the entity itself uses debt to finance the purchases, you, the person trying to make a lot of money, aren't exposed to the downside of debt as if you had tried to buy it yourself.

There are some times that debt is the best option. If you own a manufacturing plant with good returns on capital and find yourself in a low interest rate environment, it can make a lot of sense to borrow on long-term fixed-rate conditions to purchase machinery, which you then get to depreciate, that will earn exponentially more. Yes, it introduces an element of risk but you can do very well if you are conservative so that even a 90% drop in sales won't force you to the courthouse steps.

Likewise, if you see a piece of real estate property you know can be very valuable - one of those few-times-in-a-lifetime chances to grab something strategically great - buying all of it yourself can be worth the risk if you know what you are doing.

But generally if you want to take advantage of a force multiplier of some sort so that you enjoy higher profits than the underlying operation itself would otherwise generate on a pure equity basis, there is a way for you to structure the terms so that you get a fair but disproportionate percentage of the outcome. I mean, Warren Buffett is famous for not using debt but his investment partnerships, and later insurance companies, were really just leverage accounts in drag from his perspective as the operator. He was able to enjoy outsized returns for every dollar in subsequent gain. I can't recall exactly off the top of my head but I think the stocks within Berkshire Hathaway's insurance conglomerates have only compounded at something like 11% or 12% the past couple of decades, which translates into far higher returns on book value because of this leveraging effect. It's about the structure. Structure is just as important as any other variable and the one people don't seem to pay attention to often enough. A good deal can turn into a bad investment if you get the structure wrong, and a bad investment can be salvageable if you structure it correctly.

joe pierson

September 8, 2014

I suppose the 15K/year folks are fairly happy with their situation, and would not give up 20 years of their free time to acquire wealth, the trade of their youth isn't worth it to them. Youth is fleetling.

innerscorecard

September 16, 2014

I think this was just basically a fancy was of saying "look, I made money, therefore what I'm doing is investing!"

Joshua uses the term investing in the Grahamite sense, where investors are not speculators and vice versa.

You can make a lot of money speculating, and there are good speculators who are better than bad speculators, and some even have a sustainable method to the speculation where they make more money than investors. But that doesn't make speculating investing.

(That said, I really appreciate your comments and thought I learned something from them.)

SFrentier

September 18, 2014

Replying to innerscorecard

It's not speculating. Speculating is like gambling. What I do is just like buying a value stock, because you believe the company's stock will increase in value for specific, and thought out reasons. In addition you try to buy the asset at a discounted price, or during it's down cycle when it's trading at lower levels. The concept is similar, the product and value applications are different, as well as the environmental factors that effect your analysis.

innerscorecard

September 18, 2014

Replying to SFrentier

First of all, I want to say that I don't think I'm smarter than you or more financially able or successful. Quite the contrary! Nor do I doubt that you will be able to sustainably make money this way.

But that's not investing! Investing, at least as defined on this site, is the practice of owning things in relation to their intrinsic financial value - whether that's earnings, in the case of stocks, or ability to repay, in the case of bonds, or rent, in the case of real estate.

What you are doing - and I'm not saying it isn't scientific, methodical, or profitable (I would do it if I knew how) - is speculating, because it's based on the psychology of market participants, rather than the intrinsic value of the assets you are buying and selling.

david

September 19, 2014

Replying to SFrentier

There is indeed a difference between intelligent speculation and gambling, as gambling almost always has a negative expected value. Real estate is a bit of a touchy subject because many people have become millionaires through speculation and appreciation that is dislocated from the dividends of the investment. But, I believe what you may be referring to is forced appreciation along with buying at a discount from current market values. In my view, the key is how fast you can get out of the deal while still maintaining the discount (i.e. market values do not drop) and whether or not you would be satisfied holding the property based on its cash flow yield alone.

SFrentier

September 20, 2014

Replying to david

Yes part of the return is based on forced appreciation (developing the property to highest and best use) as well as discount on the buy side. Those things help insure the investment is secure short term. But I don't plan on selling. Securing 30 year fixed debt at very low rates is a long term competitive advantage, and one reason I don't like commercial RE, as you're limited to 5-10 year fixed rate loans.

I suppose you stock guys have difficulty getting past the asset price to dividend (or rent) rate, and see anything diverging from that as speculation. But remember, no matter how successful you are investing in stocks, it's largely an abstract concept, with no sex appeal. Sorry, but a coke stock certificate does not have the same emotional appeal (Josh may be an exception here 🙂 as a beach house in Malibu. (Impressing the ladies- or gents- with the beach house in Malibu...check. With the stock certificate...not so much.) Hence there is a sustainable, and intrinsic value in well located and desirable real estate. It's been like that for centuries in Paris, London, NYC, etc. Just because you cant easily quantify it with your analytical tools doesn't mean it does not exist. And that translates into appreciation. Remember, expensive locales are purchased by the marginal wealth created globally. Every time a new millionaire is minted in China or India, it indirectly benefits RE in my market. Mind you I'm talking about large swaths of areas, SF bay in my example, and not just super high end places, that only appeal to the super wealthy. I.e. The desireability of SF/bay, LA, Seattle, Hawaii, NYC, etc., etc. resonate with people on a very low level. Location defines what they aspire to be, how they see themselves, etc. Choosing one's life location is very deep and ingrained into the human psyche. Benefiting financially from these characteristics involves understanding their intrinsic underpinnings, which go beyond speculations. The analysis is very different from stock investing, but the talent to do so repedititly relies on much more than making a bet.

innerscorecard

September 16, 2014

Wow, David, thanks for the comments. I think you should be in the first class of honorary doctorates of this site.

(After I typed this out, I realized it sounded a little sarcastic. None intended! Just really impressive that you pulled those references so fast! I always have little bits of this site floating around in my mind but can never find them.)