How Joe Campbell Found Himself $106,445.56 In Debt

By Not Understanding the Risks of Shorting Stock, He Lost Everything (and Then Some) In Minutes

One of the major themes running through my body of work, both on this site and in the past 15 years of writing at Investing for Beginners, can be summed up in the statement, “Know your risks”. I hammer it home all the time; “risk-adjusted return”, talk about remote-probability events, explaining how much of wealth building is learning to “tilt probabilities in [your] favor”, admonishment to never invest in something you don’t fully understand and couldn’t explain to a Kindergartener in a couple of sentences.

I want to teach you how to think for yourself, not what to think because history is never going to repeat itself exactly. Instead, you need to be able to identify risks and potential catastrophes that aren’t known or that haven’t manifested themselves in ways identical to the past. It’s the reason I encourage you to study financial history and not fall into the easy trap of recency by casting an eye solely over the last decade; to go back and examine valuation levels prior to the Great Depression, to look at how oil stocks or food stocks behaved between 1929-1933; to study the liquidation period during the 1870’s or the panic of 1907; to accept that a so-called outside context problem could present itself.

Put another way, some of the questions you should ask yourself when risking your (often hard-earned) money are:

- What could go wrong?

- Is there any way to mitigate this risk? (e.g,. finding a way to invest in a real estate project through a legal intermediary, such as a limited liability company, in which you maintain less than 20% equity so the bank won’t require a personal guarantee allowing you to put it into bankruptcy if necessary without exposing more than the value of your investment to wipe-out risk).

- If it went wrong, what are the consequences in absolute and relative terms?

- Could I live with them?

- Is there any way to reduce the consequences (e.g., buying a cheap out-of-the-money call to cap your potential losses as an offset to a short position if you are speculating a particular firm will fail or decline in market value)?

- What is the probability of the event coming to pass?

- Is there any way to decrease the probability (e.g., investors with $5,000,000 or more building their own index fund of directly held positions rather than buying into an index fund or ETF, the latter of which could suffer from a remote-probability embedded gains risk if other investors were to ever make a run on the fund)?

It goes back to the Benjamin Graham rule “at what price and on what terms?” [*See comment section.] The terms are just as important as the price. You look at successful business owners and this becomes readily apparent; things that others don’t even think about but that guide their decision-making process, like a financial company refusing to enter transactions that require posting of additional collateral in the event of a downgrade (since that is precisely the time when they are most likely to need cash), even if it means passing on an opportunity or refusing to hold cash reserves in anything other than U.S. Treasury bills. Such conservatism is mocked when times are good and nothing has gone wrong. It’s criticized as overly-cautious; nonsensical. Until it’s not. You should almost never accept non-compensated risks unless you absolutely must. At the very least, you should be aware of what they are and go into them with your eyes wide-open. That’s it. That’s the entire reason I sometimes point out structural, behavioral, or other flaws with certain products or services even they are otherwise very good. I don’t want you to be surprised.

In fact, Graham himself often talked about security selection inherently being an art of negation. An intelligent investor is looking for reasons not to do something, then deciding if they are deal breakers. He or she wants to know what could go wrong; what could cause losses; what could show up unexpectedly and destroy beautiful capital that could have produced passive income for your family to enjoy.

This Approach Causes Some People Significant Emotional Distress. If This Describes You, Change It. Your Life Can Only Be Improved By Protecting Your Family.

In my experience, this approach resonates almost immediately with certain people, especially those who have a deep-seated optimism. I’ve told you how I’ll pass on 99% of the things that come across my desk – even things that go on to make a lot of money – because I didn’t like the risk trade-off either in absolute terms or relative to whatever else I could get at the moment. It’s okay because, as I’ve also often said, there are always intelligent things to do. If you want to own stakes in publicly traded businesses, there are 30,000+ of them around the world, many being re-priced in near real-time. If you see an opportunity and are a good operator, you can start a business of your own. If those aren’t attractive, you can find a real estate property that offers a lot of intrinsic value relative to the purchase price or, alternatively, can be financed with an arrangement that gives you a lot of upside over a long period of time with little cash flow risk. You can lend money, either through securities such as bonds or certificates of deposit, or in directly negotiated instruments. On and on it goes. Each opportunity has potential downsides that are country-, market-, firm-, and transaction-specific. Hearing the negatives doesn’t in any way discourage this type of person because they look around and know the best investment of their life could be right around the corner. It’s this faith that makes it possible to refuse to settle; to not reach for yield or take on exposures that cause concern.

It also, in my experience, immediately repulses a small minority of people who don’t separate their egos from their ideas causing them to take any sort of acknowledgement of risk as a criticism of them, as a person; a personal attack or evidence of an ulterior motive. You saw it in the 1990’s anytime someone suggested buying Wal-Mart or Microsoft at 50x or 70x earnings wasn’t particularly intelligent. You saw it in the real estate bubble when people suggested that just maybe, perhaps, it wasn’t a good idea to get an adjustable rate mortgage using earnings from the peak of an economic expansion with little to no equity cushion. You see it in gold bugs, who treat the metal like an idol to be worshipped. You see it in people who think a college education is worth any price (it’s not; it’s an investment like any other). You see it in specific businesses like the case study we did of GT Advanced Technologies declaring bankruptcy and wiping out some shareholders who had lost all sense and put most, if not their entire, net worth into it.

Today, you see it most often in index funds, one of my favorite financial market solutions upon which I’ve lavished a lot of praise. I steadfastly maintain that if you are sitting on a 401(k) plan at work, the smartest move, with a few notable exceptions, is almost always going to be to buy a lower cost index fund that is almost entirely passive in its approach. Despite this, you wouldn’t believe some of the messages I get on the topic. Take the recent mail bag response about buying stocks when equity prices are high. In the comments, I happened to mention off-hand that it is foolish for a wealthy investor who has exhausted his or her tax shelter protections to use large amounts of money to buy index funds due to something known as embedded capital gains (and that the risk inherent in doing so is not mitigated by ETFs once you look at the underlying structure despite the advertising line telling people it solves the problem). Precisely for the reasons John Bogle wrote in some of his multi-hundred page books, and in which he openly acknowledges it to be the case, it is often far wiser for a wealthy investor in this situation who wants to follow an index approach to construct his or her own index fund directly by holding the underlying stocks outright in a custody account of some sort. There is no intelligent justification for a taxable investor of significant means taking on a potential, if remote, possibility of being hit with a tax bill while experiencing losses. None. Refusal to acknowledge this fact is simply intellectual laziness.

Judging by some of the messages I received, you’d think I’d have suggested throwing puppies off a bridge. People who do not in any way fit the demographic to whom the problem would apply – you’d need at least several million dollars in a regular, taxable account to worry about this, as well as a decent likelihood of being in an upper tax bracket, which definitely applies to more than a small minority of this community but not the broader general population – thought I was somehow attacking index funds themselves, having ignored everything else I wrote or the context in which the comments were made and the very clear advocation for them within tax shelters and non-profits when the trade-offs in efficiency are worth it and the embedded gains risk is neutralized (many of you know that Aaron and I use them for our family’s charitable foundation due to taking advantage of a donor-advised fund to avoid 990 public disclosures). The fact that I am aware of the inadequacies and might advocate for them anyway, in certain circumstances, doesn’t compute with these folks. In their minds, why would I point out the flaws, including the methodology changes that are quietly happening? They genuinely cannot perceive of a reason a person would otherwise want to know of the shortcomings, let alone publicly discuss them.

Even the objections were evidence that the nature of the problem was misunderstood as the offended had no idea larger investors have entirely different systems and pricing at their disposal. I had one gentleman write, incredulously demanding to know how I could justify paying a broker $7,000 to $10,000 in commissions to purchase 500 stocks. He truly was unaware that 1.) institutional pricing for transactions tends to start at $0.005 per share (half a penny per share), 2.) for a decent-size account, you could almost always negotiate 500 free trades to get it started, and 3.) even if retail rates did apply, they would be both a small overall percentage of the capital base and, unlike an on-going expense ratio, would be amortized over the life of the underlying holdings making them cheaper in the long-run. Another talked about the stupidity of managing 500 different stock positions, apparently, again, unaware that it’s not difficult at an institutional level because there are software programs that create the necessary trade tickets which you then upload to the broker, often in CSV format after the file is auto-generated to make the necessary adjustments to keep your holdings within the parameters you outlined. This is not 1965. You don’t have to get a typewriter, ledger sheet, calculator, and pencil spending hours each month making the necessary modifications as you manually enter trade tickets. In both cases, they were taking what worked for them – small investors to whom the problem did not apply – and trying to scale it to large amounts. I’ve repeatedly told you that you cannot do that; always check your underlying assumptions! The rules are different. The prices are different. The systems are different. The opportunities are different. The pitfalls are different. To repeat what I said earlier, you can’t use the same techniques that build a log cabin and apply them to a skyscraper.

(Interestingly, this seems to manifest itself even in non-investing fields so there’s clearly a mental model of some sort at work. I think the world could be much improved if people occasionally reminded themselves, “Not everything is about me”. I was reading an article in The New York Times earlier in the year; don’t recall the specific piece or author but basically it was about budgeting and personal finance on the cost side. Anyone who pays attention to media demographic knows that the typical reader of the NYT has something like 3x higher household income than the median American household, is substantially richer, enjoys far higher rates of educational attainment and literacy, and is generally much more successful in life. Perhaps more than any other mainstream publication in the country, it is a paper by, and for, the elites. Its readership does not reflect the nation as a whole – not by a long-shot – but rather, the people making the decisions; controlling institutions, exerting influence, overseeing pools of capital, and crafting political policy. Some of the top comments were along the lines of, “I’m a mother making $35,000 a year living in Alabama. What idiot wrote this piece?! This advice isn’t relevant to my life.” The narcissism is incredible. The idea that a relevant article written to a niche audience with clearly defined socioeconomic characteristics must be perfectly tailored to the reader who falls far outside of that group or situational parameters to which it applies would be funny if it weren’t so arrogant.)

How Joe Campbell Found Himself $106,445.56 In Debt to His Broker in a Matter of Minutes Because He Didn’t Understand the Risks of Shorting Stock

An excellent example of the reasons I advocate for being fully aware of risks of each and every investment security, structure, contract, or account type, even if it makes you unpopular, has played out in the financial media over the past twenty-four hours. I first heard about the story from messages sent to me through the contact form (a special hat tip to Scott and Adam, who were the first two make me aware of the story, which allowed me to get the details prior to the GoFundMe page being removed). With the story having now gone viral, it’s possible you already know some of the specifics. In case you don’t, let’s examine the facts.

A few days ago, a guy named Joe Campbell from Gilbert, Arizona had $37,000 in an account at E-Trade. According to some sources, Joseph is a 32-year-old small business owner. It was a speculation account he had segregated from his other funds (an intelligent move, which I applaud). He knew that it was the amount he could lose without harming his standard of living. A company named KaloBios Pharmaceuticals, ticker symbol KBIO, was headed toward liquidation as it could no longer afford to carry on business due to significant cash losses. Campbell went to his broker and borrowed shares of the stock from other investors, promising to return them. He then sold the stock, pocketing the cash. The theory was, the stock would eventually go to around $0, he’d buy it back for next to nothing, replace the borrowed stock, and enjoy the difference. In other words, he shorted the stock. Because he had no offsetting security or derivative that could have protected him if he were wrong in his bet that the stock price would decline, his potential losses were unlimited.

On November 18th, 2015, the stock closed at $2.07 per share. Overnight, an announcement was made that an outside buyer was going to try to acquire the firm and keep it going. The shares skyrocketed – that’s what happens when you have a tiny business without a lot of float and a large percentage of that float sold short so there are people who have to buy it back if the price begins to increase – opening at $14.00 per share. There was little opportunity between $2.07 and $14.00 per share for Campbell to buy back the stock and close out the short position, returning it to the people from whom he borrowed the shares. The stock market is like an auction – you can go from [x] price to [z] price without ever seeing [y] in between. It’s the reason I wince internally when people say something like, “I can always sell on the way down if things go badly”. It’s a significant assumption that the opportunity will be there; an assumption that displays a considerable ignorance about the mechanism through which prices are determined in the equity markets that can come back to harm them when they can least afford it. I don’t like seeing people harmed. I don’t want them to believe things that aren’t true.

When Campbell saw what had happened, he refused to accept it was possible out of some insane notion that his broker was responsible for watching out for him (your stock broker does not have a fiduciary duty to you). Perhaps he might have expected, and maybe even received, more handholding if he were paying 2% trading commissions to a specialist at UBS or Merrill Lynch who was watching over his accounts for him, but he wasn’t. He went for the barebones, self-guided approach and that’s what he got. When he reached a representative of E-Trade, the stock was at $16.00 per share. He told them to close out the position but they couldn’t get their hands on any shares until the price was bid up to an average of $18.50 each.

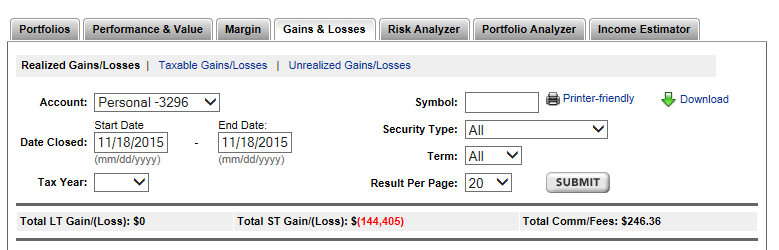

By the time all was said and done, he had a realized loss before taxes of $144,405.31, which he shared in a screenshot:

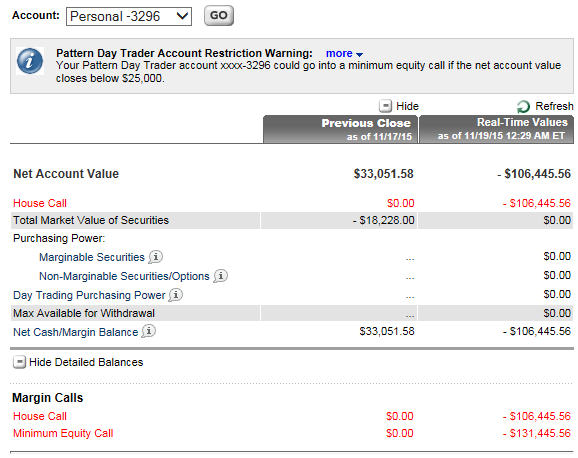

He still owes $106,445.56 after having all of his equity obliterated.

Based on some of his comments, I worry that he doesn’t, quite, understand the situation that he’s facing, even now. This is a real debt, every bit as serious as credit card debt. It will go on his credit report, making it impossible for him to get financing for anything else in his life. Thanks to universal default laws, he will most likely see his insurance rates skyrocket. He might be turned down for jobs in jurisdictions that allow employers to take credit history into account as evidence of character and discipline. The broker can sue him and all but require him to seek bankruptcy protection to make the pain stop. He doesn’t seem to understand the nature of the liability because Campbell says he plans on liquidating his and his wife’s 401(k) – if I were the wife, I would refuse to go along with this as a 401(k) account has unlimited bankruptcy protection, meaning it can probably be salvaged if they otherwise get wiped out (why start from scratch again if you don’t have to do so?) – and then work out an installment plan with the brokerage firm. An installment plan, which, of course, they are under no obligation to provide, this being a demand debt he promised to pay within 72 hours. Short of a miracle, he’s going to default. He broke his word and violated the covenant, taking on risk he could not afford. He still thinks of the broker as a parental figure there to look out for him or work with him when he’s facing hardship. The counterparty is under no obligation to help him pay back the debt or accommodate a repayment schedule. Indeed, they have a duty to the owners they are hired to protect. Perhaps that can be done while easing the stress he and his family face, perhaps not.

Campbell asked for help raising money on GoFundMe, ultimately pulling in $5,310 before ending the campaign. Here is a PDF archive of what happened, in his own words, which was part of the original page he asked everyone to share in the hopes people would kick in a few bucks to bail him out of his predicament. Joe was even willing to share screenshots with the Internet on his donation page (the ones on this page you’ve already seen as documented evidence of the story, which I’m employing under the Fair Use exemption given the public nature of his request for help on a social network), showing the amount he still owed after having all of his equity obliterated.

Should others assist him? I’m torn on the issue and there isn’t much agreement among people when it comes up in conversation. For heaven’s sake, Warren Buffett once allowed his own sister to go bankrupt – literal, total wipeout – from a trade that blew up like this (it involved options) rather than bail her out even though it would have been pocket change to save her the horrendous pain of starting over; a rounding error that couldn’t be spotted on his financial statements if you’d been looking for it. He did it because he thought the brokerage firm should suffer significant losses as they had allowed her to gain much more exposure than was appropriate, assuming that her rich brother would save her if anything happened. He wasn’t going to reward the behavior, even if it meant his sister had to bear the responsibility for her actions. Is that the right way to act? I don’t know.

I do know that, unlike many of the people who commented on the GoFundMe campaign, I’m not inclined to kick the guy when he’s facing this. In fact, I feel sick for him and his wife. If he were a neighbor or a friend, I’d invite them over for dinner, cook them a roast and an apple pie (or whatever else they wanted), tell them it is going to be okay, and send them out the door with arms full of books detailing stories of people who lost far more and ended up going on to major success. I absolutely hate that they are going through this. I’ve spent my entire life working to avoid financial wipeout risk and many of the reasons I write the things I do is because I don’t want you to suffer this kind of catastrophe. There is no reason for it. Making him feel worse or attacking him personally doesn’t undo the damage (though there might be an argument it discourages similar behavior in others). He can, and I hope, will, recover. It will be okay, even if it doesn’t feel like it at the moment. This is especially true given how young and he and his wife are. Mathematically, it is still entirely possible for them to end up wealthy by retirement. If they play their cards right, this is something they can someday look back on and laugh about together.

In any event, Campbell’s losses are far greater than they appear at first glance. Not only is he going to have the emotional stress of dealing with the nightmare, as well as the financial costs of interest, penalties, (potentially) lawyers, higher insurance rates, et cetera, the guy wants to raid his and his wife’s 401(k), which I mentioned earlier. That means paying taxes, losing the tax-deferred compounding, and, because they are younger than 59.5 years old, paying an additional 10% penalty to the IRS. This was a mistake that, depending upon his age, almost assuredly cost him millions of dollars he could have otherwise enjoyed. It happened because he was impatient, entered a transaction he didn’t understand, and happened to be exposed to that transaction when a remote-probability event occurred.

The Moral of the Story

The point of all of this is to remind you that even if everyone around you waives off remote probability events or risks, don’t do the same. (Want to know a secret? Almost everyone around you will waive off remote probability events and risks. Many people don’t like thinking about it. It makes them uncomfortable.) Even if you decide to accept the exposure, anyway, you can at least have the peace of mind of knowing that you’ve done so with full acknowledgment of the downside. You aren’t fooling yourself and that’s important. People who avoid acknowledgment of remote probability risks seem to suffer from the mistaken idea that refusal to acknowledge them means they aren’t present. Nothing could be further from the truth. The nature of the risk hasn’t changed – it’s always there – you’re simply aware of it and can decide to accept it, reject it, or take countermeasures to mitigate it.

Again, I think there’s something neurological going on with a lot of folks who fall into this trap as it manifests itself in too many places. You see men and women who know their spouse is having an affair but as long as it isn’t explicitly stated, they can go on with their lives as if it isn’t real. You see people who know their child is a drug addict but as long as it isn’t explicitly stated, they can pretend it isn’t a problem. You see people who know an employee is stealing from them but they don’t want to believe it so they refuse to confirm their suspicions. It’s related to, but different from, Mokita. Do not tolerate this kind of intellectual laziness and emotional frailty. You cannot fix a problem without identifying the problem. Avoidance only makes things worse. Never be afraid of facts. Interpret them, incorporate them, set them aside as not relevant to your situation, but never fear them. Facts, in other words, should never offend you.

On that note, none of us are guaranteed a happy outcome in life. Sometimes, things just suck. The best you can do is conduct your family’s affairs in a way that tilts the odds in your, and their, favor. That includes:

- Collecting cash generating assets

- Avoiding liabilities (contingent and explicit)

- Sticking to what you know and understand

- Keeping your costs reasonable

- Identifying and nurturing your core economic engine

- Intelligently taking advantage of tax efficiency

- Arranging all of this to serve your own personal needs, whatever those might be. Money exists to make your life better. You do not exist to serve it. It’s a tool; nothing more, nothing less.

All of this could have been avoided if Campbell had focused on risk exposure. What were the odds something like this happened, let alone during the tiny window during which he had short exposure? Miniscule. Nevertheless, since the downside threatened to destroy his standard of living, he should have walked away from the transaction. Avoiding bad deals is just as important as finding good ones.

Do not accept “it’s not likely to happen” as the end of the conversation. Always follow up with, “Yeah, but what if it does?”. I don’t care if you’re an engineer working on a construction project, a portfolio manager building an asset allocation, or an executive at a pharmaceutical company facing clinical trials for a promising drug. If merely discussing bad outcomes causes you distress or fear, you need to get control of your emotions. Perhaps you have no defenses against a particular bad outcome. Know that. Own it. Take responsibility for it. Right now, Joe Campbell is at the mercy of his broker, to whom he is significantly indebted. I don’t ever want you to find yourself in a situation where you have to depend on the kindness of others to keep food on the table. I want you to be financially independent so you can spend the 27,375 days you’ve likely been granted doing what it is you enjoy.

I don’t tell you this stuff to scare you, I tell you this stuff to empower you so you can make decisions – fully-informed decisions – about what you’re willing to accept in terms of trade-off without having to rely on others. As long as I write, I will never do you the disservice, or show you the disrespect, to shield you from the world as it is. There are no silver bullets. There are no magic beans. You must learn to think, analyze, and arrange in ways that optimize your output and upside/downside exposures. This isn’t limited to your portfolio, but rather a philosophy that should permeate your personal life and career.

Reader Comments (52)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Pete Keen

November 20, 2015

When I read this story I hoped you would comment on it. (I literally said "yessss" when your tweet popped up.) Thank you for explaining what happened and what the consequences are. I hadn't even considered universal default.

Ang

November 20, 2015

Read about Campbell yesterday as well as this guy: http://profit.ly/user/woj37/blog/my-face-is-numb-kbio - who at least actually seems to get how badly he screwed up - although he does seem to want to continue trading/speculating in the future. I think you've said this before offhand but it just seems like they could find a much better way to STRUCTURE the deal if they wanted to bet on a downwards movement (not sure if such a small stock would have options being traded, but buying puts would be one good way to go about accomplishing what they wanted)

Joshua, you're way beyond this point already, but did you find, at some point through your learning journey (when you became a lot more knowledgeable than an average layman), that it became almost too much effort to try to educate in a one on one capacity (aka having a discussion with someone on a forum) when someone has their facts wrong? I.E. the denial about the risks of an index IF you hold them in a taxable account AND your holdings are in the multi-millions. It seems a lot of times you have to almost cut through the mental blocks/models (mostly inconsistency avoidance and excessive self regard) and finish a psycho analysis before you can get them to understand the mistakes in the facts themselves - a two step process. I think having your own platform (about.com or this site) helps as it lets you get a complete and clear message across while reinforcing it with linked passages to the past on how to deal with one's own irrationality, but as far as public, one on one interactions - have you about given up at this point because of the "nuisance" of having to deal with natural human mental inconsistencies?

Joshua Kennon

November 27, 2015

Replying to Ang

It's the middle of the night and I'm not, quite, ready to go to bed so I'll indulge in one of the rarer personal answers. I try to avoid stuff like this because I don't want to non-intentionally (and without any necessity) offend someone who might happen to read it but right now, I don't want to fall asleep, it's raining outside, the house is really comforting, and I'm in the mood to talk so here goes ...

Yes. I very rarely read financial forums, comments on news articles related to the economy or investing, or even engage in one-on-one discussion in a group (e.g., if I don't know a person particularly well and they suddenly start going on about stocks, bonds, or other asset classes, I'm probably not going to say anything. It's fairly easy to suss out whether or not they have the right temperament, emotional disposition, or interest in actually learning about or discussing the topic, in which case, I might spend three hours over coffee with them if I have the time on my schedule because I love helping people get a head start and pointing them in the right direction to save years on their journey.)

Otherwise, it's a black hole both for time and emotional energy, mostly because - as odd as it sounds and I'm not even really sure I can explain it myself - I actually care about people becoming financially independent. That's one of the reasons I don't want them to listen to me, but instead, help them build a framework for making rational decisions that are evidence based and in which flaws or shortcomings can at least be acknowledged or mitigated to the degree humanly possible. I don't want to convince them of any one fact, but rather, arm them with a system of processes, checklists, and constructs that allow them to tests facts on their own and come to reasoned decisions. One-on-one, given a chance to observe someone, more often than not I find myself subconsciously tailoring the approach to do exactly what you say - cut through the automatic responses and speak them about the core of the matter in a way that they can understand and to which they emotionally relate. It's harder online, especially since people give so much away by clues not in what they say but how they look, stand, their facial movements, their accents, etc. This political ability runs in my family to varying degrees, especially among the oldest three siblings - people joke my brother and I can talk our way into practically anywhere while one of my sisters was the archetypical captain of the cheerleading squad who went on to work in the hospitality industry and knows how to read / respond to people instinctively - so it runs on autopilot almost without intent or even awareness until we stop to think about it. It's as natural as breathing. Even the small stuff is so reflexive; it came up once in a mail bag question.

Let me give you a real world example of why it's a futile task to even bother attempting to engage, especially online, these days.

You're familiar with much of my work. Therefore, you are aware that contrary to people describing me as such, I'm not, actually, a dividend investor per se. I'm dividend agnostic. What I look for is the most risk-adjusted owner earnings, which is really a free cash flow measurement, consistent with our personal situation at the time (e.g., I may pass on an otherwise perfectly satisfactory investment opportunity if it would expose us too much to a specific danger or area of the economy given our other holdings). I'll buy a stock that pays no dividends. I'll buy a stock that distributes most of its earnings in the form of dividends.

However, it is no secret that academically, it is now all but beyond refute that dividend paying stocks as a class significantly outperform non-dividend paying stocks over long stretches of times when bought and held. There are a multitude of reasons for this, many of which have now been debated, studied, analyzed, and published over the past few generations. For example:

- The requirement to maintain a stabilized dividend rate may, for example, result in management takin on less risk or leverage to protect the expectations of the owners, leading to more prudent decisions that make surviving economic disasters easier.

- Management may not be as tempted to fund overpriced acquisitions since not all of the firm's cash is at their disposal.

- The dividend itself forms a sort of "yield support" during collapses that causes lower overall volatility levels than would otherwise be the case, which makes it easier to raise equity when necessary at more advantageous prices.

- The "return accelerator" function that was a central part of the work of Dr. Jeremy Siegel at Wharton, which we went over in the post on investing in oil majors results in dividend paying stocks accruing more absolute wealthy and equity during times of higher volatility as a result of the way the mathematics work.

However, above all of that, I'm convinced the single greatest driving factor when you look at all of the evidence is the fact that dividend paying firms have lower rates of so-called "accruals" between reported net income under GAAP and reasonably estimated free cash flow (a close approximation of owner earnings). That is, you can't fake cash. When a company has a culture of requiring a big part of the annual rewards to be sent out to owners, it's much harder to fake or fudge the numbers or by getting overly aggressive with the accounting estimates. This means the "quality of earnings", as it is often called, ends up being higher for dividend stocks as a class than for non-dividend stocks as a class. All else equal, companies with lower accruals outperform those with higher accruals over long periods of time because human nature being what it is, managers tend to use accruals to be overly optimistic rather than overly conservative.

In other words, it's a quick-and-dirty way for someone who cannot estimate owner earnings to effectively increase the probabilities - by a substantial degree - of ending up with ownership in firms that generate real, rather than accounting, profits; profits that can be extracted and spent or reinvested elsewhere. The dividend is a sort of signal that, by its very presence, indicates a greater likelihood of quality under the engine. Sticking solely to dividend stocks that pass certain rationally applied and germane quantitative and qualitative tests allows selection bias to work in the investor's favor. It would be akin to a single, straight man who said, "I want to meet a 20-28 year, physically fit, college-educated woman" restricting his search for potential dating partners to the local university gym rather than randomly meeting women in the community. Sure, he'll miss some otherwise good potential matches but the probability of finding what he desires is much higher in the right environment and under the right conditions. You would think this would be common sense. If you want a white picket fence in the suburbs, a wife who bakes, eschews drugs, teaches Sunday School, and believes in strict monogamy, you are not doing yourself any statistical favors by searching for her at an all-night rave in Brooklyn. This principle even holds true for specific industries and sectors as it pertains to equities; certain industries and sectors have economic characteristics that have caused them to be far more likely to create companies that produce outsized returns relative to the benchmark over long periods of time.

(Related to all of this: I think I might have mentioned before that there was a woman several decades ago named Geraldine Weiss who came up with a system that involved sorting dividend stocks that passed certain tests into groups, then only buying when the dividend yield reached a certain level relative to its ordinary long-term trading range with a few adjustments. It's not actually perfect on its own but it's the closest thing I've ever seen to a system that could be adopted by a layman and arrive at what I would consider the "correct" valuation range most of the time. It's better than any simplified approach I've ever seen.)

Anyway, back to the point ... I'm not a dividend investor per se because I can calculate a reasonable estimate of owner earnings for a wide range of firms. As such, I don't need the signal except to the extent I want additional cash flow. I want owner earnings wherever I can get them - private businesses, stocks, bonds, intellectual property, real estate, synthetic equity, etc. It just so happens that as it pertains to publicly traded common stocks, for many of the reasons we've already discussed, firms with above-average economic engines tend to pay dividends (and rising ones at that; at rates that substantially exceed inflation in no small part because there is often a built-in inflationary protection mechanism in the operating side). But, frankly, a lot of the money I've made myself and my family over the years has been in stocks that did not, at the time, pay a dividend.

Give me time alone with a whiteboard and a person sitting in front of me and, in most cases, I can cut through the fog and at least plant the seeds of doubt necessary for them to research it on their own. That's because I try very hard not to assert something unless I can demonstrate the facts are on my side and the facts are beyond dispute. Otherwise, I don't have an opinion or qualify it by stating it is just that - a personal opinion and shouldn't be taken as anything more.

Despite that, here's a situation where I'm not going to take time out of my day to try and help someone. Recently, I happened to be browsing Reddit. A user named materialdesigner wrote, "'Dividend investing' is snake oil bullshit sold by incompetent bloggers to a mathematically and financially illiterate readership". When asked to explain his reasons for saying this, he responded, "Because the stock price changes ex dividend, often dropping to compensate for the dividend payout. Dividends aren't free money, and an investment philosophy based on them is fundamentally misguided." Then, when someone challenged him (or her), "Sigh. Nevermind, buddy. "

What is a knowledgable person supposed to do with that? This person knows enough about the mechanics of dividend distributions to understand that dividends most often accrue from net income generated from operations, piling up as cash on the balance sheet until distributed, which is then reflected in the stock price. Once the stock trades ex-dividend, the share price is reduced to account for the distribution. This is correct. There is nothing wrong with that statement. However, that is not the source of the dividend's surplus return - the myriad of reasons we've already discussed are. They are looking at the gear in the clock but don't understand the bigger picture of how that gear makes the clock function. It's not just the dividend generated and paid during one particular measurement period. It's all of the other things that dividend represents we've already discussed. This is my absolute least favorite type of person to deal with in life - the person who is smart enough to be smarter than average but who doesn't have it - that spark - to see how the whole thing fits together. I don't understand, personally, how it's not perfectly evident. It's right there. The whole thing, all the moving pieces and how they influence each other like, again, a clock mechanism. I don't know if it's a different type of intelligence, an emotional thing, or what, but life experience has taught me it's real. Part of me thinks obsessive curiosity plays a role; like a kid turning over a machine in his hands trying to see how it works because something inside drives him to understand.

This poster has none of it. He (or she) is combative. There is no interest in actually having a discussion. There is no intellectual curiosity. They are so ignorant they don't realize how ignorant they are. Again, not being a dividend investor proper, I think it's fair for me to point out as I don't have an ideological dog in the fight. I go wherever I think the best risk-adjusted returns are and happen to be able to analyze data while understanding the underlying influences on equity returns as it was all I thought about, and cared to study, for a major portion of my life up until now; a total obsession that consumed most of my waking hours.

What would I gain by posting a response to a comment like that? Aside from not being open to discussion, certain mental models kick in that I'm certainly not immune from experiencing. I don't like him (or her). It's visceral. They strike me as arrogant, ignorant, condescending, and not particularly bright. They may be none of these things. They could be incredibly awesome - someone with whom I'd want to be friends with for the rest of my life - but all I have to judge them is this passage. For the sake of efficiency, my brain reads it and discards it; "not worth the trouble, let them deal with the consequences of their myopia". The fact that their life could be improved doesn't motivate me because I now value my time more than the quality of their life because of the negativity i associate with their behavior. It's not necessarily right, but it's reality. All else equal, I close the tab and move on to the next picture of a funny cat. It probably helps that the proposed alternative - in many cases, indexing - is good enough that, were they to stick with it, the outcome is probably going to be acceptable, which I'm sure influences my in-the-moment thinking in the same way you'd be less likely to intervene with a bunch of kids throwing paint at each other, where the worst consequence is that they ruin their clothes, than you would trying to push a kid out of the way of an oncoming train, where the worst consequence is much more dire.

This is one of the reasons I focus on the framework. If I correct one misconception, that's where it ends. It's merely a leaf on a branch that needs attention. Folks get these crazy ideas in their head - they cram in facts without understanding the who, what, where, when, and why behind them, which are just as important as the fact itself - and then they don't want it challenged. As someone who cares deeply about his own self-interest (largely, as you know, due to a matter of self-preservation early in life), I don't understand the appeal of going through my time on Earth. If someone can prove to me - really, demonstrably prove with facts and logic - that something I believe or concluded is false, I'm genuinely, profoundly grateful to them both on an intellectual and emotional level. They've done me an enormous service that will pay dividends as long as I draw breath (and possibly after depending upon how it changes the way I influence those around me, including my family). They've helped me discard a falsehood that could have caused me to make a mistake. No matter how hard I try, I do not understand the appeal of wrapping yourself in the false comfort of a lie or error. Why wouldn't a person feel appreciation towards someone who challenged his or her thinking? You are not your ideas. Ideas should be tested, beaten, refined by fire, debated, and clarified. This is especially true for any idea that you did not arrive at on your own but that was instilled in you prior to the age of 25 years old by authority figures, peers, or culture as these can often go without examination and lead to a lot of folly down the line.

todd

November 27, 2015

Replying to Joshua Kennon

Joshua, Word can't explain how I feel when I read your writing about investing. I have AD and in school I didn't read a single book but when my uncle started me in investing I stared reading books about value investing like What Works on Wall Street, Old Money Master, John Neff, Rich in American, Proof of the Pudding, The Future for Investing. But for the past 4 years I have not found a book that can pull me in. Your Writing does. I always love to read my Tweedy Browne funds reports they pull me in. Your writing holds my attention. One thing that I worry about is when you start you Money Management Firm that you may not write as much on this your blog.

undercover

November 20, 2015

This post makes me think of the Titanic meets friendly iceberg. Like with that famous saying: you cannot judge a book by its cover, you cannot judge all the risk with an glance. The real danger is what you can't see.

The captain of the Titanic was defiant to risk and made this statement. “I cannot conceive of any vital disaster happening to this vessel. Modern shipbuilding has gone beyond that.”

And we all know what happened next.

Joshua Kennon

November 23, 2015

Replying to undercover

This is one of my favorite (if frustrating) mental models! It's called Risk Compensation. I should write about it. Basically, when people believe they are safe because of some sort of technological improvement or other advantage, they begin to behave in riskier ways which, paradoxically, increases the overall level of risk. If he had been in a ricky boat, he'd have been less likely to hit the iceberg despite the voyage being more dangerous overall. Humans are funny.

There's a really germane example of it happening right now with a certain Gilead Sciences drug. It's probably going to end up unleashing a lot of misery on the world because it is resulting in people making stupid decisions. That'd make a wonderful case study if I have time for it ...

Roundball

November 23, 2015

Replying to Joshua Kennon

I've always wondered if Gilead Sciences was on your radar. Would love to see which risk issue you see pertaining to their medications- some sort of Hepatitis/ disinhibition scenario?

Adam @ AdamChudy.com

November 24, 2015

Replying to Joshua Kennon

A simple example would be mandatory seat belt laws encouraged people to drive faster.

Rob

November 24, 2015

Replying to Adam @ AdamChudy.com

Agreed. Also how boxing injuries went up when it moved from bare-knuckle to gloved (easier to keep hitting someone in the head when your hand is padded and doesn't break) as well as football injuries increasing when it moved from leather helmets to current ones (no one is going to launch themselves headfirst when they have no protection).

joe pierson

November 20, 2015

The embedded capital gains issue kind of bugs me, isn't it just prepayment of one's taxes? When a massive stock market decline occurs, the fund sells, and you pay taxes on the embedded gains, you're not really paying other peoples taxes, just prepaying your own. (because your cost basis changes, I guess one could look at it like paying other peoples taxes, but ultimately, they will eventually pay your taxes later on). In the end, one may come out ahead or behind because of such of an event, depending on your tax situation during the time the event occurred and when you eventually sold.

Isn't the problem more a matter of not being able to optimize your tax losses/gains, because one gives up that control, ultimately, when you hire someone else to do your buying and selling. Or am I missing something?

Joshua Kennon

November 23, 2015

Replying to joe pierson

1. An important point: The embedded gains don't have to be triggered by a stock market decline, they can be triggered by the fund simply becoming less popular than it was to the point that redemptions exceed outflows and it creates a cash crunch that requires liquidation or payment-in-kind distributions to fill the funding gap.

If you were a long-term owner, this would result in big piles of capital that were working for you that now aren't compounding. That's a tremendous amount of lost wealth over subsequent decades. There is real power in using deferred taxes as a source of leverage.

2. If it does happen during a market decline, think about the compounding effects and opportunity cost. Imagine we go into a 1929-1973 or 1973-1974 meltdown that makes the relative tame (and short) 2009 crash mild in comparison. You have money in a taxable account and suddenly, your positions are decimated. At this point, when asset prices are at once-in-multiple-generation prices and you should be acquiring more, you either have to 1.) sell your painfully undervalued holdings to cover the tax bill, or 2.) use outside cash resources that could have acquired substantial ownership at record prices to pay the IRS rather than buy Coke or Hershey at give-away prices. Even if you could fund it, the real-world lost wealth as a result of you having to pony up funds at the worst possible moment when your opportunity cost is at its peak might not appear on your financial statements, but it is very, very real.

It's like those people shoving MLPs in their retirement funds, banking the management was going to do the right thing, and that if they didn't, the transfer agent would catch it. Look at the future wealth destroyed due to Kinder Morgan reorganizing itself, screwing over its long-term owners, and Pershing, the custodian, not doing the IRS paperwork for 5,000 investors on time, resulting in huge penalties and interest. Was it likely? No. Could it have been avoided? Yes. It is, technically, a timing difference on the core tax bill? Yeah. It's still going to cut future compounded wealth drastically because less capital at the beginning of the compounding period means less to work with as the growth exerts itself on the base. It's the time value of money formula. It matters a great deal.

In both cases, it can be avoided entirely. There is no meaningful downside so why not behave in the more intelligent manner? Why take a risk you don't have to take? Why expose yourself to outflows that aren't necessary? I don't care how successful I am, how much cash I have in the bank, how big my portfolio is, if there is a way to minimize an outflow, I'm going to do it, especially if it's at a moment when I'm going to want cash most. I'm somewhat obsessive about it (one of the first things I do when analyzing promissory notes or financing arrangements is look at accelerated repayment or cross-default clauses for this very reason).

innerscorecard

November 21, 2015

Thanks for remembering!

Ironically there was a Google ad on this page urging me to trade hot penny stocks. (That is one unfortunate consequence of algorithmic display ads, that their content is often hilariously at odds with the context in which they appear.)

Perhaps we'll learn someday...

Joshua Kennon

November 24, 2015

Replying to innerscorecard

Found it!!! You were digging deep in the memory archives so I apologize for taking so long to give you an answer, it had become such an internal part of my operating mechanism I couldn't remember his exact phrasing or where I read it, which made it hard to track down. I finally decided I was going to get it off my task list tonight so I resorted to grabbing his works off my library shelves, sitting down, and manually flipping through the pages, knowing I'd have noted it somehow on the page given its influence on my thinking (this was after I had purchased the Kindle version to try and see if I could search for it by using phrases I thought I remembered, which didn't turn up anything).

I took pictures to make it easier for you to find it in your own editions since it seemed important to you (I think you sent a message, a comment, and a Tweet several weeks apart all gently requesting the source, haha!). You'll never have to wonder again!

According to my notes, I first came across it during the summer between my sophomore and junior years of college, 12 years ago. The concept was originally published in the 1934 edition of Security Analysis on page 29 where he wrote, after spending awhile expounding on the importance of getting the price right:

"Instead of asking, (a) In what security? and (b) At what price? let us ask, (a) In what enterprise? and (b) On what terms is the commitment proposed? This gives us a more comprehensive and evenly balanced contrast between two basic elements in analysis. By the terms of the investment or speculation, we mean not only the price but also the provisions of the issue and its status or showing at the time. [snip] An investment in the soundest type of enterprise may be made on unsound and unfavorable terms".

Reading through the totality of his life's work, he was basically expressing it as "Security + Terms [Price, Contractual Protections, Counterparty Risk, Liquidity Risk, Economic Risk, Management Risk, etc. etc.] = Decision], while noting in the prior page that individual security selection is just that - individual - so that a good investment for one person at a specific price and on specific terms in a specific issuer might not be appropriate or advisable for another person.

Eight years later, in the 1940 edition, he repeated this (only this time it was on page 33 as changes in the text resulted in a different manuscript). My notes this time around were summed up at the top of the page: "This is an expansion of his 1934 principle. "At what price and on what terms?", which was a bit of a butchering because I didn't need the clarification as, by this point, I'd distilled it internally down to the core spirit of the manner and added it to my operating software; always asking, "What could go wrong?". Graham's body of work had become somewhat of an obsession of mine around this time, going so far as to track down his out-of-copy, rarely read texts so it was meant much more in my mind than it sounds like in literal translation of the words. It was right around this part he was talking about the importance of not giving into false specificity; that you don't need to know the exact intrinsic value, only an approximation close enough to provide a high degree of assurance that it is, in his word, "adequate", which he later expounds upon as the "fat man" test we've discussed (i.e., you don't need to know a person's exact weight to know he is morbidly obese when you first see him; intrinsic value can be much the same for certain enterprises at certain times under certain conditions).

I checked both the original editions of the 1934 and 1940 works, as well as the more recent reprints, which you can buy on Amazon. It's in all of them. The modern editors didn't paraphrase or modify it.

I'm having a harder time finding it in the 1951 and 1962 editions but, to be fair, having already sourced it twice I probably only looked for five more minutes. It's possible they aren't there are all because the manuscript had begun to deviate substantially from its past form with Graham and Dodd rearranging sections, updating their past conclusions, removing other passages, etc. Of course, he had nothing to do with the 5th edition so there's no point in discussing it. The modern 6th edition is merely a reprint of one of the earlier editions with added commentary (I appreciate the work that went into it but find it distracting as I much prefer the original text so I can analyze and think about it as it was presented the world, drawing my own conclusions).

I'll try to more faithfully reproduce the literal summation of the quote in the future; "in what enterprise and on what terms" as I tend to be a bit lose with the language. If I forget, you'll at least know this is the part I'm referencing.

Hope that helps. It was a fun distraction and ended up causing me to give me a nice boost of nostalgia as it took me back to much earlier in my life. Now, I have to return to the real world. My schedule is overloaded at the moment so the stuff I could put off got put off ... I have 21 or 22 different tasks I have to complete on the Investing for Beginners site prior to the end of the month, plus two pies I need to bake for a family Thanksgiving event tomorrow. It wouldn't have been so bad if Aaron and I hadn't started a Korean drama called Producer. It was not the best time to open the door to my addiction but what's done is done and I must now live with the consequences. I saw IU, who is one of my favorite singers - I quite literally listened to the (the song Twenty-Three on endless repeat for the hours during which I built the About directory/database; when I first heard it, the disco base line when the chorus starts at around the 1:12 mark put me in the mood to work so I figured I'd do something productive and that's the result, which would not exist right now had she not written that song) - and Kim Soo Hyun. Resistance was futile. It's not great so far, which is kind of shocking given the cast they put together, but there's still awhile to go before we're finished with it. Truth be told, even though I need to block off the next 6 to 10 hours to write at home in the study or office, finishing my About commitments for November, I'd really like to go wrap myself in a blanket, sit by the fireplace, and turn on another episode or four. Even this comment ... I'm procrastinating because when I'm done writing it I have to work. Ugh ....

innerscorecard

November 24, 2015

Replying to Joshua Kennon

Thank you!!!

Yeah, for some reason at the time I asked you, I was really thinking a lot about the fine distinction between price being a subset of the terms of an investment (as is the case in the Graham quote) and price and terms being two angles or dimensions to be analyzed separately (as I thought in my head upon reading your memorable restatement). The reason I thought about this way was because of a discussion I was having with someone about whether companies with ethical issues or fraudulent issues are investable at all. My own views are of course heavily based on my research into Chinese companies, but the same issues to a lesser degree probably exist everywhere.

I think the way I was thinking about it in my head is whether bad enough terms are a zero to add to the value of the price, in which case a good enough price would be good enough, or a multiplicative zero, in which case bad enough terms make something simply uninvestable.

And actually, I found your restatement phrase a lot more intuitive to me than the original Graham quotes on the matter I found, which was why I was so interested in your thinking!

Joshua Kennon

November 24, 2015

Replying to innerscorecard

No problem, happy to help! I understand where you're coming from on the question, especially as it relates to the ethics of an enterprise.

For what it's worth, in my own head, despite how I shorthand it, the formula has really become a modified hybrid that looks more like this (the feeling I get and what I mean when I say it) over the years:

1. "In what enterprise?" [what is the quality of the economic engine and its likelihood of retaining that power?] +

2. "At what price?" [what will I pay for ever after-tax, net-of-inflation unit of purchasing power flowing to me discounted for time?]

3. "On what terms?" [legal protections, call provisions, dilution probabilities, capitalization structure hierarchy, contractual provisions, etc.]

4. "Under what personal considerations?" [the relevant factors that may override or modify the importance of everything up until this point based on the individual situation I, or the person for whom I am acquiring the security or investment, may face.]

That last one in no small part is influenced by psychology and existing holdings of the person with whom I'm dealing. I know some people, even in my own extended family, who cannot stand volatility (I love it, as you can tell). The presence of outsized volatility is going to cause them to make mistakes so it's better to earn 8/10ths of [x] buying a stable blue chip under all conditions than the potential better outcome of 10/10ths of [x] acquiring something I find particularly attractive at the moment, telling them the only metric by which they are allowed to judge the holding is the rate of growth in the dividend distribution relative to inflation (in reality, I'm watching much more but they don't need to know that or think about it). Others just want to go after what they perceive to be the highest returns. Still others are entirely situation specific; e.g., the recent General Electric split-off in our case was influenced in no small part by the huge bank holdings members of my family have, which already give us a lot of exposure to the financial industry. Many of those positions have substantial built-in deferred taxes as a result of unrealized gains, which means that even if Synchrony were relatively undervalued, it wouldn't necessarily be intelligent for us to make the swap given the other risks it would entail, the adjustments that a prudent person would need to make, and the way it would change the overall portfolios. There was a personal element that can not be adequately judged by looking solely at the performance of each stock over the next five years.

Ethics play a role in that, too, so there is some blurring of the lines. My mom has a mandate in her portfolio: She only wants to own happy businesses. There are certain enterprises I am forbidden to buy regardless of how attractive they are, or how much money they could make her, because she doesn't want to generate cash from that type of behavior. It's a pass/fail test that is more important than anything else in her case.

innerscorecard

November 24, 2015

Replying to Joshua Kennon

Great framework. A fifth bullet point that some may like adding (perhaps hazardously to their wealth, in the end) is "In which set of circumstances in the world?" But that's of course part of bullet point one, too.

Stephen H

November 25, 2015

Replying to Joshua Kennon

I love that - "happy businesses". Maybe its not meant to come off cutesy, but I totally picture a mom (my mom?) just saying "Happy businesses only Steve!". Made me smile.

Todd

November 21, 2015

I suppose one possible outcome is that Joe Cambell's situation could end end in divorce. Is his wife liable for the debt in this situation? Perhaps if she didn't sign the margin agreement, she might be in the clear.

Eric L

November 21, 2015

Replying to Todd

Arizona is a community property state. Yes, as a general rule most likely his wife is also liable. If Joe skipped town to say Mexico, the brokerage could go after her for 100% of the debt. I do not think a divorce will get her off the hook as the debt was incurred while they were married.

Joshua Kennon

November 23, 2015

Replying to Todd

Whenever this story has come up, including some in-person conversations over the past few days (it's all anyone has been talking about around me for awhile, even people who ordinarily don't bring up stocks) - this is one of the first things I hear people say. Why is that? It genuinely surprises me. (This is more a philosophical question, I suppose; not directed at you, it's just that your comment brought it to mind.)

If all it takes to get a person to contemplate ending a marriage is a financial loss, why did they get married in the first place? To be fair, I cannot imagine a scenario in which I woke up to find us on the hook for a large amount of money because of something Aaron did (if that were something I needed to be concerned about, I would have put protective measures in place or not gotten married in the first place). Nevertheless, assuming he was operating within parameters we had set as a couple and not secretly doing something on the side (which would be the case - we never do anything without the other's full knowledge to the point we have full veto power over the portfolio buy and sell decisions), it would never cross my mind to get a divorce. This was explicitly covered in the wedding vows when entering the covenant wasn't it? "I take you to have and to hold, from this day forward, for better or worse, for richer or poorer, in sickness and in health, to love and to cherish forsaking all others, till death do us part"? If I didn't meant those words, I wouldn't have said them. They could be hauling our furniture off and putting the paintings on the wall up for auction and I'm not going to love him any less. Be irritated? Sure. But if he made a mistake that big, it's going to most likely be the moment when he needs my support the most. In that moment, it would be more important than ever we were united in adversity so we could get through it together and rebuild.

And, again, maybe this is simply that our personalities are so conservative, and we're so protective of certain things, we don't need to worry about it. I mean, even if God forbid under some unthinkable remote scenario something unimaginable happened that caused me to accrue a lot of debt and declare bankruptcy - I can't even picture what it could be at the moment since we hate liabilities, tend to avoid them like the plague, and think about risk all of the time - there are going to be assets that would be very, very difficult to reach. Even the straightforward stuff; e.g., once we were able following the Obergefell ruling, we took advantage of the Missouri provision allowing married couples to title property as joint tenants in the entirety, meaning we don't own some of our assets, our marriage does, making it harder for potential creditors to reach. A lot of the KRIP securities are held in SEPs and comparable plans from back when we were in college and therefore have no limits on the bankruptcy protection the current laws provide. Once our kids are born, there will be irrevocable trusts setup for their welfare to which property is transferred, effectively removing it from our estate. We'd walk out of court broke on paper but having a lot of money growing tax-free for us, and our children, by the time we retired.

Again, this isn't in any way directed at you, it's just that your comment has caused me to sit here and think about it since it's been on my mind a lot in the past few days, hearing the sentiment so frequently. Looking back, I never hear the same thing about men, though. Are there really all of these women out there that would divorce their husbands if they went broke, made a mistake, or suffered hardship? And if so, why did those men marry those women in the first place? That seems like a far worse transaction than shorting a low-float stock you didn't understand.

Maybe it's that the women in my life tend to be high-quality but ... is this really a thing? I know that, statistically looking at household formation and dissolution data, women initiate a super-majority of divorces, effectively destroying their families with the most common reasons being a lack of personal fulfillment or boredom which seems crazy to me in the first place so maybe there is a gender difference here but I look around at my female friends and family members and I cannot see them leaving someone over money or putting their own needs above the needs of their marriage. My sister-in-law worked so my brother could accelerate the schedule at which he would graduate medical school, supporting the family and marriage over her own needs. My best friend from high school lived in France for months after her wedding, having to commute to England since she couldn't get admitted to the country, to see her husband who was studying at Oxford, that way he could pursue his dream. My mom got a job at H&R Block when I was a child to try and make recovery from the bankruptcy faster when my parents lost everything then, later, went on to sacrifice a new home and work non-stop at the start-up phase of their manufacturing business that brought them their current prosperity. My mother-in-law took whatever job she needed to support her family when times were tough, including at one time waitressing. If they went bankrupt (again, unlikely, as they have an aversion to debt, too), I have no doubt in my mind at all my sister would go pick up whatever work she could to help them rebuild if something happened to my brother-in-law's career. I mean, that's what marriage is ... building a life together, through the good and bad. If Aaron wanted to go to cooking school in Paris tomorrow, and it was really important to him, I'm going to sell the house, rearrange my life, and we'll find a way to make it happen. You work together with your spouse so you both become the people you want to be.

The whole thing is weird to me. If one of my male friends were going to marry a woman who I thought would behave that way, I'd be tempted to look at them and ask, "Are you really sure you want to do this?"

Maybe it's a learned skill set? Or a culture thing? I have a close friend whom I've known for decades. When she got married, anytime she and her husband would have an argument, he'd bring up divorce. He came from a situation where everyone was divorced, remarried, re-partnered, dating, re-divorced, etc.; nothing lasted. She, in contrast, comes from a long line of devout Catholics where divorce isn't an option; not on the table, no matter what happens because you make your choice and then you commit to it. Whenever it happened, she'd immediately stop the conversation and explain, "Marriage is for life. No matter how badly you, or I, screw up, neither of us is going anywhere. I wouldn't have married you unless I was going to stick by your side until one of us drew our last breath." If he had done something like this, I have no doubt he probably would have been preparing for a divorce in fear whereas it wouldn't even cross her mind. It wasn't a conditional covenant.

I'm rambling now ... I find the idea interesting, though. It's been taking up a lot of my time, thinking over it. Why is that among the first reaction people feel? Is there any truth to it? What does that say about the state of marriage? About women? About men? Do people really marry someone that doesn't love them unconditionally, flaws and all? If so, why? Low self-esteem? Pragmatic settling? I don't know ... I need to put it on the back burner and contemplate it for awhile.

david

November 23, 2015

Replying to Joshua Kennon

You may find this interesting. http://www2.census.gov/ces/wp/2013/CES-WP-13-62.pdf

It's sad to think that your wife will kick you when you're down. You're only option is to become a good picker.

dave(nestle)

November 21, 2015

Maybe this is a stupid comment but...

I don't think Etrade even had an appropriate handle on the risk they were taking by letting this guy short this stock. They probably had no idea of the probabilities of this event happening, or the potential losses they(Etrade) might face.(and I will bet this(buyouts and/or similar announcements in off hours) is not even that uncommon) Shareholders should be pissed! What if this happened to a much larger pool of clients simultaneously? Did they even check this guy's assets for his ability to pay?

Sorry, just rambling some biased initial thoughts on banks, brokerages and the like...

Joshua Kennon

November 23, 2015

Replying to dave(nestle)

Want to be truly terrified about remote-probability events and the brokerage industry? Look at what has happened with re-hypothecation (especially firms using the United Kingdom's laxer regulatory requirements to effectively gamble with clients' money). It's one of those esoteric areas that the average investor probably hasn't even heard about but it will cause your heart rate to rise when you realize what some financial firms have done, and the risks to which they have exposed client funds. Under the wrong set of circumstances - and this isn't some sort of unprecedented scenario as brokerage failures have happened en masse in the past (Graham had a whole section in at least one of the Intelligent Investor versions discussing how to protect yourself from the risks; people have forgotten they are a possibility) - the world may someday wake up to find that a lot of investors with margin balances log in to their brokerage account to see a big chunk of their account balance missing, seized by creditors for debts they did not incur, because their broker had pledged it as collateral for their own speculative purposes and then went under due to a bad bet of some sort.

Here's a reportedly first-hand from someone who happened to have an account at MF Global when that broker went under and client assets were seized due to re-hypothecation.

Is it likely? Not particularly. Neither was the 1987 crash. Or the 1973-1974 crash. Or the 1929-1933 crash. Or the panic of 1907. Or the 1870's liquidation. I don't like the idea of waking up to find I'm on the hook for someone else's trading losses. One of the best defenses (assuming you don't want to go to the trouble and expense of using the direct registration system for all of your holdings) is only using so-called "cash" custody or brokerage accounts that have no margin capability at all as they must be segregated from the brokerage firm's assets by law. It's a bit less convenient as you have to make sure funds are available prior to settlement on each and every trade but it's definitely worth the peace of mind.

It gets worse, too, because some of this was by design. Remember the 2005 bankruptcy reform bill? The one that made it all but impossible for most students to declare bankruptcy on their student loans among other abuses? Aside from distorting the free market and being socially non-desirable, one of the fine print provisions allowed derivative counter-parties to take precedence over other creditors in the event of insolvency. That means the major institutional banks in New York would recover any of the failed broker's assets before restitution was made to the brokerage clients who had their assets seized; assets that the broker had quietly, and unbeknownst to them, used as collateral for their own activities. You could have some guy in Iowa with a small margin account have his shares of Coca-Cola taken because his broker did something stupid and Goldman Sachs or JPMorgan Chase demanded repayment.

It's one of those things where people probably think I'm overly conservative but I sleep better at night because of it. Take my parents' portfolio as an illustration ... the portion of taxable assets I have them hold at a brokerage firm are within a cash-only account. I don't want any of their securities hypothecated or re-hypothecated. Plus, there's an added bonus when buying smaller capitalization firms with little to no float: Shares held within a cash-only account must be segregated and can't be lent to short sellers (if you hold shares in a margin account, the brokerage firm makes money off you by lending out your stock without your knowledge). Although it may not be the most logical thing to do (in theory, short sellers could drive the price down so it's cheaper to buy more), there's something emotionally satisfying about removing float and, in the process, making things more difficult for speculators. I think the smallest firm on the family's books across the board at the moment has a total market capitalization of somewhere around $65 million. If someone sells shares of this particular business short, they aren't borrowing the stock from us.

Ang

November 23, 2015

Replying to Joshua Kennon

Joshua,

Can you please confirm that only a margin (and from the article, it sounds like global only?) account is subject to this risk? A cash only brokerage account (even if option enabled) is segregated from such non sense correct? The poster (who is probably merely upset and paranoid after having his own money taken away from him) made it sound like all cash and securities in a brokerage account with access to global exchanges is unprotected, but then said he would close all margin accounts, so I'm just a little confused. His promise to put all of his assets into gold and silver isn't really helping clear the message either...

IlovePi314159265359

November 27, 2015

Replying to Ang

It is for margin accounts. Following is a great link (direct download! pdf from FRBPvhil) with explanation as well tidbits such as this gem:

" But, interestingly, a

high proportion of large traders choose

to allow rehypothecation. From the

2010 ISDA margin survey, 44 percent

of all respondents to the survey and 93

percent of large dealers report rehypothecating

collateral"

https://www.phil.frb.org/research-and-data/publications/business-review/2011/q4/brq411_Rehypothecation.pdf

Connelly Barnes

November 23, 2015

Replying to Joshua Kennon

Thanks for this great article Joshua.

Your attitude towards risk has been one of the biggest influences on my investing thus far. As a result, I plan to never have any unhedged short positions.

Thanks for mentioning re-hypothecation risks. My take on this is that it seems prudent to limit the percent of one's assets in margin accounts due to the extra risk. I found more information discussing re-hypothecation risks on Wealthfront:

https://blog.wealthfront.com/false-comfort-of-sipc-insurance/

Joshua Kennon

May 27, 2016

Replying to Connelly Barnes

I know this is six months late but, going back and trying to catch up on comments (it seems like they multiply - I'll visit a thread from five years ago and there are comments I somehow missed as there is a large element of luck and timing in my buckshot approach to responses given whatever is on my desk at any moment) and saw this:

If this were A Christmas Carol and I were Ebenezer, now would be the time where you'd see me leap up after realizing it's still Christmas and all is well, doing my happy dance and calling for a celebratory goose.