Like the residents of Lake Wobegon, another year of better data analytics and audience growth has cemented what we’ve already known: As a group, you’re way above average. You are considerably richer and better educated the average person in the United States, more likely to identify as politically independent, more likely to have children, and skew male with far higher than normal interests in science, books, technology, news, fashion, food, gardening, sports, cars, investing, music, video games, and finance.

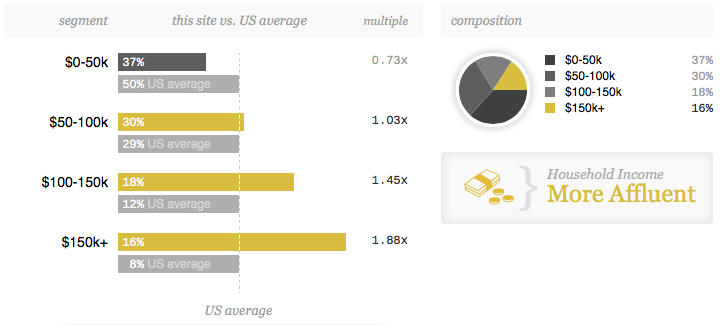

Specifically, 1 out of 6 of you now earns a minimum of $12,500 per month, while 1 out of 3 of you is earning at least $8,333 or more per month inclusive of the higher bracket; both far and away better than the United States as a whole (the last time I checked, the middle quintile of households earned $2,895 to $4,336 per month). Though there is no way to track it, I’d bet a lot of money that the net-worth-per-dollar-of-income figure of this group is off the charts as almost everyone here seems to prioritize saving and investing high on the list of life’s joys. Hand almost anyone who reads this blog a big check and the odds are good that most of the money’s going to be devoted to earning dividends, interest, and rents so we can enjoy the cash flow for the rest of our lives.

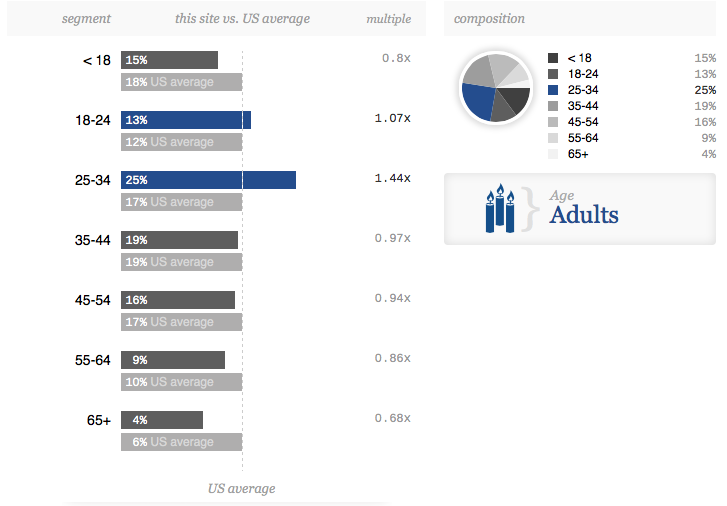

You are disproportionately 25-34 years old but otherwise, you roughly mirror the general population except for the 18 and younger, and 65 and older, age groups, which are underrepresented.

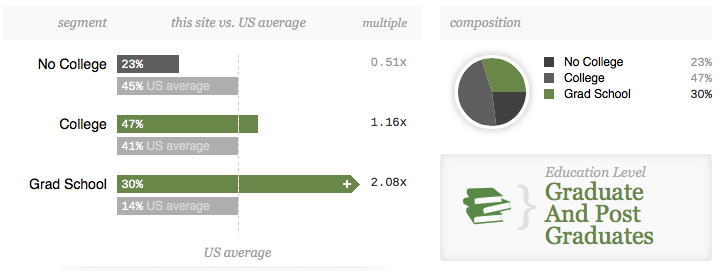

You are 1.16x as likely to have a college degree and 2.08x as likely to have a graduate degree relative to the general population in the United States. You are half as likely as the typical American to have no college education at all.

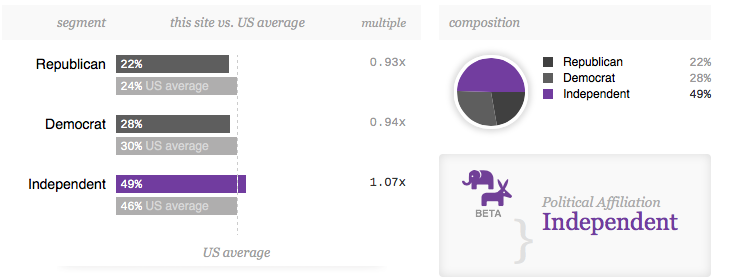

A new quantitative measure tracks political affiliation and, no surprise given most of us seem to identify as rational pragmatists, there isn’t a lot of ideological purity. You are slightly more likely than average to identify as independent but otherwise represent a great cross-section of the country. Specifically, 22% of you identify as Republican, 28% as Democrat, and 49% as Independent.

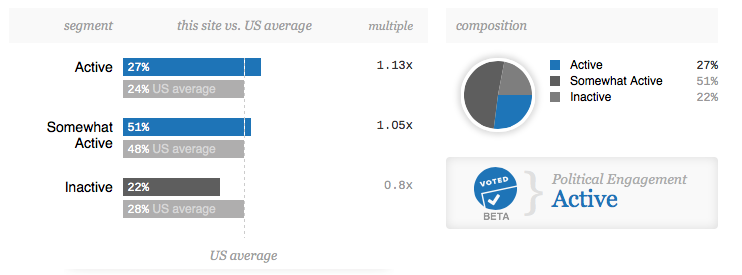

You are more politically active than the average American, taking an interest in the direction of your country, elections, and laws.

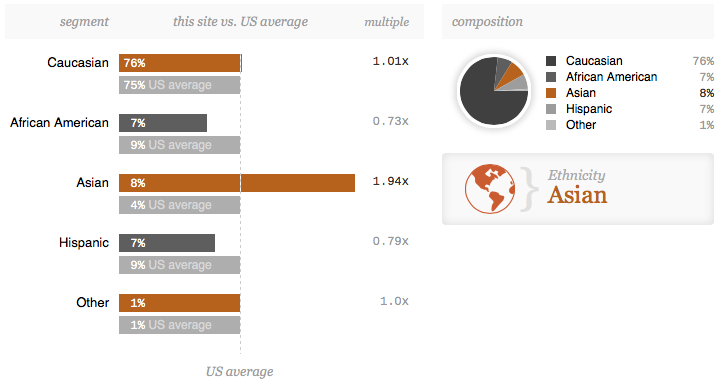

Ethnically, Asian readers are twice as prevalent as you would expect relative to the percentage found in the general population but this makes perfect sense when you cross reference the demographic’s higher-than-average educational attainment and earning power. Roughly 1 out of every 14 of you is black, 1 out of every 14 of you is hispanic, and 1 out of 100 of you identifies as “Other”. Caucasians are right around what you would expect relative to the general population so not much deviation there.

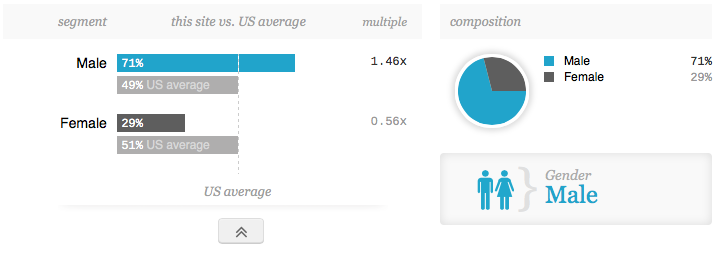

This next statistic fascinates me because I can see it fluctuating with the type of post I write. The female audience continues to grow, now standing at a few percentage points shy of 1 out of 3 blog readers. Yet, as a group, you (the women) are largely lurkers unless I write about family stuff – Christmas, food, the home renovations a few years ago – which causes you to come out of the woodwork (e.g., case in point: The most commented post in the blog’s history was a recipe that my family took 10 years to perfect replicating the Cinnabon cinnamon rolls and a super-majority of the public replies were from women).

[mainbodyad]On the other hand, when I write about economics, statistics, science, accounting, video games, and finance, a significant percentage of female readers go silent, sending me private messages to discuss a topic further but rarely leaving their thoughts for public consumption. It’s incredible to me because among you are forces of nature with intellects, resumes, accomplishments, and net worths that would make a person’s jaw drop; who have no problem standing your own in even the fiercest debate but, nevertheless, you prefer one-on-one discussions. Why the gender divide in the way topics are discussed? I’d like to solve that someday when I have time to research it.

In any event, to the women out there who do publicly comment, I raise my coffee cup to you in thanks. I love seeing your contributions to the community and wish more of you would emerge from the shadows to join in the conversation.

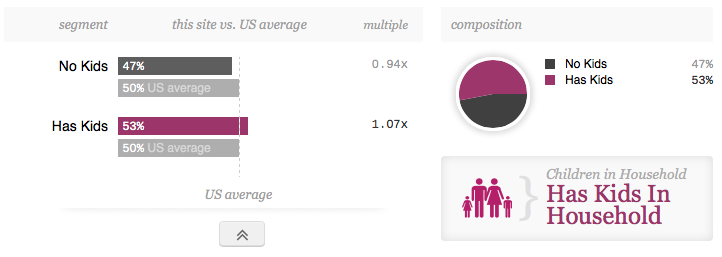

Congratulations! For the first time ever, you are more likely than the general population to have children! Specifically, you are 1.07x more likely than the U.S. as a whole to have released your progeny upon the world. I’m sure you’ve already setup your DRIPs, UTMAs, and trust funds, right? Of course you have. You’re you. You don’t need reminding.

As for how you read the site:

- 62.08% of you read on a desktop or notebook computer

- 24.29% of you read on a mobile device

- 13.62% of you read on a tablet

As to which mobile and tablet devices you prefer, some highlights:

- 35.60% of you read on an Apple iPhone

- 30.68% of you read on an Apple iPad

- 1.70% of you read on a Samsung GT-I9300 S III

- 1.09% of you read on a Samsung GT-I9500 Galaxy S IV

- 1.01% of you read on an Apple iPod

- 0.84% of you read on a Google Nexus 7

Your browser preferences:

- 34.10% of you use Chrome

- 30.03% of you use Safari

- 14.44% of you use Internet Explorer

- 12.67% of you use Firefox

- 4.69% of you use some form of Android browser

A handful of interesting reading habits from the audience share and affinity scores:

- You are 130.0x more likely than the general Internet user to read financialsamurai.com.

- You are 63.0x more likely than the general Internet user to read theconservativeincomeinvestor.com, which is run by one of the popular commentators here that any regular reader of the site will recognize.

- You are 55.9x more likely than the general Internet user to read dividendgrowthinvestor.com, also written by a site regular many of you will recognize.

- You are 46.8x more likely than the general Internet user to read Dappered.com, a site about men’s fashion, clothing, drinks, shoes, travel, watches, grooming, etc.

- You are 33.2x more likely than the general Internet user to read zerohedge.com.

- You are 23.1x more likely than the general Internet user to read artofmanliness.com, which is about sports, clothes, career, and manly things.

- You are 23.0x more likely than the general Internet user to read SkyrimForums.com. (I’d be curious what type of class system the readership prefers. I almost always opt for destruction and conjuration mage. What are you all? It’d be interesting if a pattern emerged. Who knows? Maybe the community is disproportionately pickpocketing archers who carry out clandestine assassinations.)

- You are 22.9x more likely than the general Internet user to read theslowroasteditalian.com, a site devoted to simple Italian recipes. I’ve never even heard of it but now I’m going to have to go look.

- You are 22.6x more likely than the general Internet user to read thepointsguy.com, which tracks offers on rewards programs, credit cards, and more.

- You are 16.0x more likely than the general Internet user to research municipalities or zip codes on city-data.com. I highly approve. I use this site all the time as it is a great first-pass research tool.

- You are 15.3x more likely than the general Internet user to read GardenWeb.com, a community devoted to growing things including food and vegetables.

- You are 15.3x more likely than the general Internet user to read thefreshloaf.com, a website devoted to amateur artisan bakers and bread enthusiasts with a ton of recipes. I’ve never heard of this one, either! I know what I’ll be doing tonight.

- You are 15.1x more likely than the general Internet user to read the Christian Science Monitor, a news resource.

- You are 14.9x more likely than the general Internet user to read Wired.com, the tech and science site.

- You are 14.5x more likely than the general Internet user to read The Sweet Home, a site devoted to finding the best you can own in your house; e.g., the best rake for leaves, the best dishwasher.

- You are 13.7x more likely than the general Internet user to read Life Hacker for tips about optimizing your life efficiency.

- You are 13.7x more likely than the general Internet user to use, in some capacity, ukessays.com, either paying to have someone write a paper for you or, alternatively, selling your own writing to make cash from your intellectual capital.

- You are 13.1x more likely than the general Internet user to read American Banker. That’s a good trade resource right there.

- You are 10.9x more likely than the general Internet user to read Stack Exchange. What’s crazy, though, is that this blog and that site share a 15.3% overlap in readership; the highest numbers I could find.

- You are 10.3x more likely than the general Internet user to read Golf Digest.

- You are 10.1x more likely than the general Internet user to read Sally’s Baking Addiction. Those maple doughnuts look good …

- You are 9.3x more likely than the general Internet user to Read Men’s Fitness and 9.1x more likely to read Men’s Health.

- You are 9.1x more likely than the general Internet user to read Board Game Geek, a site devoted to board games including original editions.

With so many shared interests, maybe I should add a forum to the site. It wouldn’t be hard to install one and people wouldn’t have to carry on conversations solely in post comments, would be able to start their own topic, etc. Then, on the other hand, I really wouldn’t get anything done because I’d end up spending half my day talking with some of you about bread recipes, video game releases, Supreme Court cases, or Korean dramas. Google wouldn’t even know how to optimize it. It would be the most random collection of topics imaginable; dividend stocks, real estate properties, and debates on ancient philosophy or the need for a modern luddite movement to counteract the rise of artificial intelligence.

Speaking of real estate, there are a lot of you out there with a hand in the property markets. You are 8.7x more likely than the general Internet user to read forsalebyowner.com and 8.2x as likely to watch land, ranch, and farm sales at Land and Farm.

There are just pages and pages of data. You are 8.7x as likely to read Minimalist Baker. You are 8.3x more likely to browse auction listings at Live Auctioneers. You are 8.2x as likely to read American Lawyer. You really like your home theaters as you are 7.9x as likely to read Home Theater Forum. You apparently like to grill things, too, as you are 7.4x more likely to read about the science of smoking meat to get the perfect ribs or hamburgers. You also like to see the world as there is a big overlap in readers between this site and Fodor’s Travel Guides.

Finally, on that note, we’re more global than ever. Roughly 5.58% of you come from the United Kingdom, 5.51% from Canada, 2.68% from India, 2.62% from Australia, 1.16% from Singapore, 1.09% from South Africa, and just shy of 1%, each, from both The Netherlands and Germany.

[mainbodyad]

Reader Comments (51)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Joe O

October 3, 2014

I'm surprised not to see mrmoneymustache.com on the site overlap - I know quite a few of us from the forums over there read over here.

Steven

October 3, 2014

Very interesting stats!

I read the first three sites in the list frequently, I actually found your site when researching a post I'd read on Tims site way back.

innerscorecard

October 3, 2014

I would gladly pay for the forum. Look at Corner of Berkshire and Fairfax for an example of how that would work well. Or the Mr. Money Mustache forums for a good example of a free forum.

Seriously, it would instantly be one of my top forums. The commenters and readers here would be a great group.

In other news, this post reminded me of how much harder I have to work to get to a respectable level!

innerscorecard

October 3, 2014

Tim's dialogues with Joshua in the comments here are some of the best you'll find on the Internet.

emma

October 5, 2014

Replying to innerscorecard

Really - I didn't realize Tim was on this site - would love to see some of the dialogue if you could post the links:

David Tran

October 3, 2014

Very interesting facts.

Joshua Kennon

October 4, 2014

I was, too, given how many people tell me they are active in the community over there. If I had to guess, I'd bet it's in the top 3 correlated sites but doesn't show up because he hasn't enrolled in the third-party verification Quantcast data set so it has to use rough guesses, making it unable to compare it accurately to the 100+ million websites it tracks.

Roundball

October 4, 2014

I'm such an idiot. I never realized that was Tim.

Surprised that Seeking Alpha didn't show up in the shared websites.

Scott McCarthy

October 4, 2014

Given that the ages here skew young (every group over 35 is under-represented), I wonder if that would be true. Statistically, high income and high net worth both skew older, not younger. The young population here hasn't had the benefit of compounding yet, and given the relatively high educational attainment, those high earners probably have some educational debt weighing them down.

Joshua Kennon

October 4, 2014

Replying to Scott McCarthy

You're definitely right that given how young (overall) the audience is, the members of this community are nowhere near as rich as they are going to be as they continue to compound. If I remember correctly, Dr. Thomas Stanley, the professor down in Georgia who studies America's affluent, got around this in his research on millionaires by coming up with a formula (I think he wrote about it in the endnotes of the Millionaire Mind if you check the small print giving his model) that adjusted for age by arriving at an expected-net-worth-for-every-dollar-of-income-at-a-given-age or something like that. That way, you could tell how much better, or worse, a person was doing than would be reasonably expected.

He (Stanley) did it by profession, too, which was the really interesting part to me. He found certain occupations, which attracted certain temperaments, resulted in far greater net worths than others. Engineers, for example, pile up way more wealth than you would expect for every $1 in income throughout their lifetime compared to the same $1 in income from any other profession because they have a habit of looking at lifecycle cost on major purchases and thinking logically about money as a math problem. They read the fine print on loan documents, buy cars that break down less, watch their investment expenses. It adds up to a huge differential by the end of their lifetime.

Scott McCarthy

October 4, 2014

Replying to Joshua Kennon

I will have to look into that. Millionaire Mind has been on my reading list for some time, but it hasn't made its way to the top yet. That may have just changed.

Joshua Kennon

October 4, 2014

Replying to Scott McCarthy

It's definitely worth reading, though it was published in 2000, so it's 14 years old (I wish he would update it). It's hundreds of pages of data charts shows things like the percentage of millionaires who bought their home at X price and the percentage of millionaires who live in a home currently valued at Y.

The curiosity about the age modification factor was going to drive me nuts so I went and grabbed one of my copies. I found it in the appendices. Check the small print at the bottom explains he measures expected net worth in his calculations by taking age x .112 x income. I know I have it around here somewhere, maybe it was in an article or another one of his books, or explained earlier in the text, but somewhere, somehow, he explains the modification factor (.112) had to do with a reasonable expected capitalization rate of private business earnings and a few other things (e.g., if you own a small business that earns $100,000 but has $100,000 in book value, it's obviously worth much more than $100,000). It was essentially a cheap and dirty way to approximate the IRS estate multiplier technique of net worth estimation. It's been so long, but I remember coming to the conclusion that I was satisfied with the reasonableness of the figures for most, typical small business owners.

He has since modified it, changed the figure to .1, and clarified it for those with long educational periods saying they should deduct the years it took to get their advanced education (e.g., med school) from their age when performing the calculation; see his blog post about it here. He was worried young people would be discouraged because it makes it appear their net worth should be bigger than it is. The problem I have is for business owners, for whom this approach won't work. Their net worth is bigger than they think it is. If you are 25 years old and start an LLC that is successful enough to pay you $150,000 in cash distributions per year out of profits, even if the LLC has a book value of $0 because it requires no capital to operate and you drain it, you are clearly worth at least $1,000,000 even if your balance sheet shows nothing. You could sell those membership units to someone, somewhere, or continue to drain them and use the funds to buy Treasury bonds or rental properties or blue chip stocks.

My favorite thing about it, though, is his search for the highest returning small business categories in America. He said that over and over, his business major students couldn't accurately name even one of the top ten most profitable enterprises for someone to own. (p. 222-224). He goes on to explain this is probably why Korean American immigrants were 3x as likely to have incomes of more than $100,000 per year in the 1970's despite having no college education, arriving with no inherited wealth, and not being able to speak the language - they had to find the most intelligent opportunity they could and ended up in the dry-cleaning business (which is no longer as profitable but it was back in those days) in numbers so great the main trade publication had to publish a Korean version alongside the English version! Meanwhile, the typical American child who went to business school just sort of coasted into whatever they do by emulating their parents or trying to get a job at a corporation, not really thinking about profitability or opportunity beyond selling his or her time.

One of the people he studied made his millions owning junkyards. The guy's mother was horrified, telling him he should go to college, instead, because "anyone can own a junkyard". That willingness to ignore even loved ones when the numbers and trade-off support a calculated, intelligently structured bet comes through over and over when reading the histories of the people he interviews. There's a guy in there named Mel who, over many years, borrowed only $175,000 from banks, never putting in any of his own money. He ended up owning three city blocks, and collects $750,000 a year in income from it. Even his father initially discouraged him but he ran the numbers and knew he could make them work conservatively.

david

October 4, 2014

Replying to Joshua Kennon

BTW, if you want to see the story on mel, you can see it here:

http://books.google.com/books?id=p60tDntHVnUC&pg=PA183&lpg=PA183&dq=the+millionaire+mind+mel+real+estate&source=bl&ots=98zUPLD1eO&sig=c7S09KRr7Exo14w0s4Mehy2RMio&hl=en&sa=X&ei=tXMwVMuUBajGiwLj7IGQDw&ved=0CC4Q6AEwAA#v=onepage&q=the%20millionaire%20mind%20mel%20real%20estate&f=false

I also remember the author's focus on the property management business as good vs. doing development. Of course, when you look through the lens with a ROE viewpoint, everything suddenly becomes much clearer.

When I read about guys like Mel, I always wonder about the leverage issues. Is it really worth bankruptcy risk when you're young to catapult yourself to a 7 figure net worth much faster, but could also decimate you for a while. Getting back up to that first 100k is a terribly difficult process when starting over. The pivotal point seems to be if you have a smaller amount of capital like 50-200k when you're say 25. I guess the solution for the conservative investor is to simply procure more money outside of investing vs doing higher risk, single bet type things. That is, until you have enough cash to do those kinds of higher risk activities in a more diversified way with several buffers of assets still working for you if it fails. Your capital scaffolding idea has really helped me think through my assumptions and ask myself whether this is something I actually need to do vs just waiting a little longer for a more certain result.

One question for you Joshua - Did you ever take any risks that could have forced you to start over - or "go back to go" in the early years of your wealth journey?

Thanks

Joshua Kennon

October 4, 2014

Replying to david

In answer to your question ...

No. I was, and am, so fanatical about protecting myself against the downside, even when speculating, that it borders on religious dogma. There are no exceptions. There are no qualifiers. If I cannot live with the potential outcome, no matter how small, I walk away. One of the primary objectives in my investment policy manual is that my family and I must maintain our standard of living even if we woke up to Great Depression II. I wouldn't even want them to notice since nothing would change in terms of how we live, what we eat, what we wear, how we shop, etc.

I've found that wipeout risk is often employed by those who lack a certain degree of creativity. Most of the time, you can achieve all the upside leverage you want without the downside exposure. Let's say it were the middle of a property bubble in a fast moving real estate market. If I wanted to gamble, I would not go borrow huge amounts of money to do it. I'd write an option to buy contract, waive a bunch of cash in the face of people with a specified period during which I could acquire their property (even if it wasn't currently on the market), then find a buyer. It would be equivalent to buying call options on real estate by creating the derivative out of thin air. If I were good (and lucky), able to get an interested buyer, I'd capture the differential between the contract exercise price and the negotiated sale price all for the premium I paid, earning massive returns on capital. If I'm wrong, my potential losses are limited to the premium and I'd have avoided mortgage debt, interest payments, insurance payments, etc. Under the arrangement, I can absolutely estimate, to the penny in most cases, the total maximum potential exposure. Yet, I can still capture almost all of the gains if I'm right. If I did borrow money, I'd probably do it through private placement and bury a provision in there that allowed me to convert all outstanding debt into equity in the event of a default, removing the debt immediately and avoiding bankruptcy; e.g., the bondholders would become the equity holders and debt servicing is suddenly not a problem. Banks aren't going to let that happen but individual investors will. You just have to find them. There's nothing unique or novel about these strategies. Plenty of people have employed them. Yet, they seem fairly rare out in the wild. Most people seem to accept existing standards and pre-printed forms as if they are somehow indisputable, never stopping to consider there there are a dozen ways to slice the pie. If you follow the laws, and get everyone to agree to mutually satisfactory terms, the only limit is your imagination.

It's all just people and contracts. It goes back to what Ben Graham taught when he said you need to pay attention to both the price and the terms. The terms are just as, if not more, important than the price. Sometimes, three or four words added as an addendum to a provision in an agreement can mean the difference between escaping with minimal losses and seeing most of your net worth destroyed.

I've never even naked shorted a stock, vowing I would avoid it like the plague after reading about the short squeeze that decimated the fortunes of a lot of rich men in 1901 who took positions against The Northern Pacific. I still remember coming across the tale in a biography of J.P. Morgan I read during high school and it horrified me. If I wanted to swing for the fences on a business going bust, I'd buy put options. Again, the terms of the put agreement allow me to capture almost all of the upside but the potential maximum loss can be calculated and capped. I know going into it what my worst case scenario is so I can decide if the trade-off offers satisfactory mathematical odds. (In theory, if the pricing were more advantageous, I could short the stock itself then buy a call against it as an insurance policy, but I'd still never short naked.)

If you ever find yourself in a position where you are convinced you have to put it all on the line to succeed, you probably aren't being clever enough. There's a solution out there, somewhere, and it is often very simple. Even then, often, the speculative situations aren't nearly as attractive as you probably think. Sometimes, you're better off saying, "Screw it. I'm going to buy another block of Coca-Cola and lock it in the bank vault for the rest of my life." Collecting an ever-growing stream of dividend checks from one of the best businesses in the world is not some great tragedy.

Then again, my aversion to being sent back to "Go" is significantly influenced by the fact I spent roughly half of my childhood in this house after my parents lost everything. I was never, under any condition, going to do something that could cause me to end up back in a place like that. The old chestnut, "You only have to get rich once" was, and is, my gospel.

Some disagree with me. There seem to be a significant percentage of investors, business leaders, and entrepreneurs who treat making money like some sort of signaling theory for reproductive fitness or source of entertainment. They act as if their very self-worth is defined not by the end results but the misery and risk it took for them to achieve it. I prefer the rose-lined path myself. It may have taken me a bit longer to get there but, really, the utility of each additional dollar begins to drop pretty quickly once you have total control over your time and can buy almost anything you want. If the world goes to hell tomorrow, I don't want to have to pause my game of Civilization to pay attention because I'm going to be fine no matter what. That's how I like to live my life. Not everyone feels that way and you have to do what is right for you; take the risks you can accept. It's your game, and your story, after all. What will make you happiest?

david

October 4, 2014

Replying to Joshua Kennon

Well, thank you very much for the detailed response once again! Getting rid of this sort "all on the line" thinking has been one of the greatest takeaways from reading your posts and comments. That, and creative leverage. I'll be honest, for a long time, it seemed like that's how most people went into business - by putting everything on the line, mortgaging the house, etc. But it just doesn't have to be that way. This sort of all-in thinking also seems to be very prevalent in real estate circles as well.

"Oh, you've got 300,000, you can purchase this 1.5 million hotel. Just sign here. Yes, it's a personal guarantee, but that's just what everyone does. OPM, remember!"

An interesting quote by munger - Risk limits - understand the downside.

http://books.google.com/books?id=LhMGSDiQghEC&pg=PA93&lpg=PA93&dq=damn+right+munger+lose+everything&source=bl&ots=qOti1Zz6nN&sig=xIAo3wk075LECv70W-QtTAFghSk&hl=en&sa=X&ei=paAwVOr9K8i6ogTEnIGgDw&ved=0CC4Q6AEwAg#v=onepage&q=damn%20right%20munger%20lose%20everything&f=false

Joshua

October 4, 2014

Replying to Joshua Kennon

As usual, I find your most helpful thoughts in the comments section.

Dave (nestle)

October 4, 2014

Replying to david

From one David to another...

Just a small story, I am 42 now. Back in my early twenties up until about 32 years old I started 3 businesses. The first was a complete failure, but was done with no debt(all cash savings). The second was slightly profitable, yet I found no joy in it. (I did it more because it was guaranteed to make money, based on my level of involvement). I closed it down.

The third business was done with leverage and more cash savings. That one caused me to start over from zero and below, basically.

What I had going for me was my income potential from my education/job field and my hard working and understanding spouse.

So now, 10 years later, somewhat wiser/more patient/disciplined, and with alot of cold cash(my risk tolerance was severely curbed from my "failures" and other reasons) that I amassed during this last decade, I can tell you that it is absolutely possible to start over.

It gets harder to stomach as you get older, and harder to work to make up another "first $100,000". But hopefully you can learn many things from that type of failure which will make the rest of your life much more financially safe.

My advice is take your time and think, think, think. Then research and think some more, before you take a risk. Make sure it is as calculated as you can make it. But never go though life with regrets, especially when you are young enough to recover. Just don't be a cowboy where you think you know everything because something is coming at you that will hit you hard.

Hope this helps.

Dave (nestle)

October 4, 2014

Replying to Dave (nestle)

Oh, and by the way, I sometimes sit and think of the simple things I missed when I ran those two businesses. How easy those ideas would have been to avoid if I knew then what I know now.

The problem is that life is many times backwards. You sometimes have to make the most important decisions when you have the least knowledge or experience.

innerscorecard

October 4, 2014

Replying to Joshua Kennon

I really don't think the years of advanced education should be deducted from your age at all. It's kind of going back on Stanley's whole real premise, that you should coldly look at the real economic attainment of people and not the social standing. Graduate school may in fact just be a terrible choice economically (and if the starting salaries were high enough, the old model would work well enough - you should in fact feel "behind" if your first job ever is nearer age 30!

Paul

October 4, 2014

Long time reader here, first time poster.. Very interesting data to say the least. Just one question though if you could elaborate a little, Where are you deriving income information from for your page viewers?

TheLonelyHumanist

October 4, 2014

I don't read very many of the sites up there. But I have a browser full of new reading. This list is a tremendous reference.

David B

October 4, 2014

Seconded, lonelyhumanist. I do read a few blogs on that list, but now I have a lot more to look forward to.

Re: your data, I can anecdotally confirm some of them. 28, my wife and my income well above average, however to Scott McCarthy's point our net worth is nothing to write home about. That said, we are homeowners when few of our peers can say the same (bought a fixer upper after the crash and are doing the work ourselves for fun, education and to conserve capital), and are growing our assets in qualified accounts with employer matching. As time goes on, we will begin to see the effects of compounding.

Allen Jarboe

October 4, 2014

Outstanding, I also have new tabs open!

JB

October 4, 2014

If I could request one thing it would be a forum here. Imagine the discussions!

Also, not many other visitors from the Middle East?

Scott

October 4, 2014

With respect to your aversion to limiting risk how would view losing the upside on hedges? I had an incredible year in business however,I left $200,000 on the table locking in a decent margin. Reducing risk was the goal but it's hard to feel excited knowing all the money left on the table.

Cheers,

Scott

Joshua Kennon

October 5, 2014

Replying to Scott

Hey! Long time since I've seen you on the site. I hope everything is going well with you and your family =)

Re: your question. It doesn't bother me but that is because I made a choice twelve years ago to never let it bother me. Back in the winter of 2002, when I was a sophomore in college, I spent almost all of my free time absorbed in Benjamin Graham's writings and he talked about the irrational tendency of people to view money left on the table as a loss, specifically as it related to selling shares of a stock that went on to do very well. He talked about the importance of being able to make a decision, accept the risk trade-off, and live with the results as you were running a book of business based on the average of your decisions over time. Even though it meant you sometime lost out on upside, it also meant you did far better when things went south and, in the aggregate, your record should be superior. You, the business man or investor, were very much like an automobile insurance company. You wrote policies based on averages and sometimes, a policy went bad and you had to pay out. You don't lose sleep over this because you know that overall, it works in your favor and you get richer.

He also made a moral argument that a person who enters into a transaction should be perfectly willing, if he got what he wanted out of it, to see the other party make money. If you have to sell your shares of GE, or put a hedge on your corn or milk production, to make sure you can send your kid to college, it shouldn't cause emotional distress if the other party makes money because things worked out in his or her favor this time. If it had been otherwise, you would have expected him or her to uphold their end of the bargain so you should be glad for them and know you both extracted value from the deal.

All one can do is behave rationally, and act intelligently, with the facts as they are known at the time. To become distressed that a specific roll of the probability dice didn't work in your favor when your overall system is soundly based on average probabilities is entirely emotional and can ultimately lead to big long-term losses.

His analogy of the investor or business owner as an insurance company, with some policies that go good or bad, was so superior that I immediately took it for myself. From that moment, I've never once regretted doing, or not doing, something if I felt, in retrospect, my decision was the best it could be based on the information available to me at the time even if that decision turned out to be wrong. It changed my life and gave me a lot more peace of mind. It also gave me more courage to follow my conviction about what the numbers tell me, not giving in to whatever delusion everyone else seems to be falling into at the time. Even in cases where I recognize, in hindsight, that I made an error, I learn from it, avoid the same mistake in the future, and keep improving day by day.

I mean, think about your hedges. Sure, you have a lost opportunity cost on this one particular transaction, but, ultimately, you are still richer than you were 12 months ago, right? Do that year after year, decade after decade, and the $200,000 ends up being a rounding error. What is the saying ... you don't have to go for every last penny?

Keep seeking wisdom, keep maintaining discipline, keep generating a surplus to compound and someday, you'll look back and the one transaction will be a rounding error. That's what makes it so rewarding. I came very close to buying shares of Panera Bread, Starbucks, and Apple before they went on to make investors very rich, but I never pulled the trigger. And you know what? I still ended up where I am. On average, I made a lot of very good decisions and they add up to something in the aggregate. It makes life interesting.

Scott

October 5, 2014

Replying to Joshua Kennon

Joshua,

Thanks for the insight! I feel better now:) being aggressive in the commodity business with leverage, makes using hedges a great tool to reduce risk. So my philosophy has been that fixing a certain percentage of your input costs and gross price, on the portion of your business that wouldn't be there with a more conservative production number.

Cheers,

Scott

innerscorecard

October 5, 2014

Replying to Joshua Kennon

A relevant quote from blogger Daniel at Awesome Secrets that really etched itself into my permanent memory:

"Suppose someone offers to play a game with you where they flip a coin repeatedly. If it lands on heads, you win $100, and if it lands on tails, you lose $50. You know that you will win money in the long run, so do you care about the result of the next coinflip? Many people can’t help but care. Some people don’t care. An even smaller group don’t even perceive the result of the coinflip. It barely exists to them. They just see themselves being handed $25 over and over, and they sit there with a calm, content look on their face."

dave (nestle)

October 5, 2014

I just finished reading numerous posts at "theconservativeincomeinvestor"

WOW, what a very interesting site! Nice job over there. Thanks.

I dont know how I never knew about it before.I gotta get out more.

Emma

October 5, 2014

Hola from SoCal. I guess I'll be the first woman to respond to this post. Yes, I've noticed that there are very few comments by women. I'm going to check out your most commented post just out of curiosity. Personally, I like reading your financial and mental mode type posts & I tend to skip cooking, family, holiday posts although I have young kids - go figure!

Emma

DividendGrowth

October 5, 2014

Joshua,

Thanks for writing those stats. They are pretty interesting. And thanks for the shout out.

I know we have had our share of disagreements, but I actually do enjoy your site and read it at least a few times per week (if you post too). You have a knack for motivating people to action, which is really what financial education should be all about.

Good luck to you and hope all is going well!

DGI

A

October 5, 2014

Some of the numbers might be inaccurate because some users might be using tracking cookies/analytics blockers or using proxies with non US IP addresses.

Joshua Kennon

October 5, 2014

Replying to A

It's not so much a problem in this day and age. Quantcast's methodology adjusts for stuff like that using statistical sampling. The billions of dollars in advertising involved, and its role as one of the biggest five digital quantitative metric companies in the world, means that is one of the first things people like them need to account for if they are going to have any credibility. Even if they were to exclude that (relatively small) group entirely, it would still be a useful baseline relative to other websites to measure differential in audience even if the absolute numbers were altered.

A

October 5, 2014

Replying to Joshua Kennon

Ah gotcha! Thanks a lot for clarifying that. I am one of those people using proxies and analytics blockers most of the time. Do you think it is acceptable for entities (both governmental and non-governmental) to track people's online behavior and store that information for (practically) eternity? I realise that most of the logs are (supposedly) stripped of personally identifiable information but that is not always the case.

I understand the business case for analytics working in the computer industry, but I have a hard time accepting that the browsing records of millions of people can be stored and analysed within minutes to construct a profile of them. Do you think browsing records and other web activities should receive legal protection similar to medical records, since a person's web activity can tell you a lot about a person? I am not familiar with US laws since I don't live there so forgive my ignorance.

Finally, do you use any analytics blockers or are you okay with entities tracking your every move on the internet? Thanks again for responding earlier.

Bo

October 5, 2014

Is Tim McAleenan actually commenting on your posts? I read your blog, his and Dividend Growth Investors blog. Thanks for the links, more reading material!

Rob

October 5, 2014

Replying to Bo

Tim comments under 'FratMan.'

Steven

October 5, 2014

Replying to Rob

You just revealed Tims secret identity (I didn't realize that it was him), just don't give up the location to FratMans FratCave!

Rob

October 5, 2014

Replying to Steven

Ha ,these Disqus profiles give everything away. Been a huge fan of both Tim and Joshua's writings for a long time now; extremely informative and thought provoking.

Alexis C

October 6, 2014

Replying to Rob

Thank you! I enjoy FratMan's comments and have thought several times, 'I wish this guy had his own blog.'

Tiffany

October 6, 2014

+1 for a forum. I am on the MMM boards every day - coffee & MMM is now my morning routine. It gets my motivation going for the day and reminds me what I'm going out there to acheive.

Another chick here 🙂 Joshua, I love reading your blog - thank you for all you write. I've learned SO much from here and I check in all the time (though not every day;) I'm not a mastermind like you, and there's still a lot of stuff that goes over my head. But I won't stop reading 🙂 I've tried e-mailing you but it goes to a fashion photographer, haha. Thank you and keep it up, like Emma^ my bread & butter are the finance/psychology/sociology things you post (which is oddly enough how my education/work have combined) rather than cooking/shopping stuff...

Evergreen

October 7, 2014

Girl here. I think the reason why women post less on the technical threads is fairly simple - those posts are more likely to include people who will react negatively to them just because they are a female making the comment. A post about cooking will feel "safe" whereas other ones may not (unless they're like me, who couldn't care less about cooking). Such a large/vocal portion of the Internet hangs a "no gurlz allowed" sign on their doors, that subconsciously women may try to avoid conflict anywhere that resembles those environments. Even posting this, as a not-afraid-of-controversy person, I still feel a sense of wariness. It doesn't take much to bring out the trolls.

Melaine Sebastian

October 8, 2014

If I remember correctly, women are more likely to suffer from "imposter syndrome," where sufferers feel that they are not deserving of their accomplishments and that their opinions are not as valid as others'. I feel like this contribute at least in part to the different commenting style of men and women.

Personally, I would love to comment more, but I'm rubbish at financial topics (despite being very penny-pinching.) Even as a recent honors STEM graduate, I cannot seem to make heads or tails of investing lingo (not for lack of trying.) My ineptitude is what usually keeps me from commenting.

Kandice

October 8, 2014

Thank you for an amazing reading list. I'm always on the prowl for good reading material and you listed several with which I'm unfamiliar. Also, I think the demographics are very interesting. (I also came here from MMM initially.)

Kandice

October 9, 2014

Replying to Kandice

Also, I know the owner of Board Game Geek. Super nice guy.

Jay Tank

October 25, 2014

Yes, Joshua, a forum! That is something I always thought would be a great addition to this already-wonderful blog. Not only would more people come out of the woodwork in the forums, but there would be a veritable explosion of intelligent discussions that we all would undoubtedly have due to our similar interests, reading habits and levels of intelligence.

Sam Dogen

October 28, 2014

Howdy Josh,

Neat post! Nice job figuring out your readership demographic and sharing. I might have to do this one day, too. I've done numerous surveys about the FS community readership so far as reported by them.

Nice community you've built!

Sam

Financial Samurai

Fiona Skallerud

November 3, 2014

I guess I'm one of the females that lurks more than posts. Funny, because I do really enjoy the finance/video game/science posts. I'll have to make more of an effort to post, because I do love your blog (and yes, cinnamon rolls = fantastic as well. I still make them!).

Steve

February 18, 2015

You probably already know this, but I'm actually quite surprised that these are what Alexa reports as your top keywords from search engines.

Now that my curiosity has gotten the best of me, I am going to go Google "Prince Harry Net Worth" and see if you come up in the first few pages.

Joshua Kennon

April 29, 2015

Replying to Steve

It's not particularly accurate in any useful sense. I use another verification service for traffic so Alexa has no way to actually verify my data other than their best guess, which in this case is seriously wrong. Case in point: The post detailing the trust funds Princess Diana left behind after her death isn't even in the top 100 pages ranked by page views as of a report run two minutes ago.

MAB22

January 26, 2017

Replying to Joshua Kennon

Interesting. I was brought to your site just this month for the first time after searching craigslist for furniture gems and somehow finding a link to your MDF Furniture article about why not to buy cheap furniture (Although I could never shun Ikea entirely. It has cost me only $0.00913/day to own a coffee table I bought there 6 yrs ago and it's still holding strong).

Since finding your site, I've read countless posts and have even hopped over to Investing for Beginners to read more. It's a rabbit hole for sure, but a useful rabbit hole. Wish I had found you sooner, Joshua.

Thanks for writing!

P.S. The stats about women being lurkers inspired me to post something, anything, today. . . Even if it's over two years since you first wrote this.

Gilvus

September 22, 2015

2015 edition? I'm not seeing much of a difference in your quantcast data except that the 35-44 age group is slightly better represented, the proportion of mobile views continues to gain above desktop views, and the top ten affinity scores now belong to investing sites. Maybe because your gaming posts have been thin the past year?

Also, the "reddit hug" wasn't included in your data. It would've looked like the Burj Khalifa in your chart.