It’s Been Nothing But DRIPs, UTMAs, and Trusts for Days

I’ve spent the last three days working on setting up trusts and custodial accounts for the younger members of my family so we can gift them shares of great companies over the next couple of decades. I’m not settled, exactly, on the specifics. On one hand, I’m tempted to setup a family investment partnership-like entity as an LLC. This would allow me to pool resources, save on costs, and gift membership units under the custodial protections in the Uniform Gifts to Minors Act, while still retaining effective control once they exceed the age of 21 in case they can’t be trusted with money. On the other hand, I think, “No, this is a teaching mechanism. Just setup direct stock purchase plans, exactly like I did for my youngest sister. They need to be able to see their company; watch the dividends grow.”

Speaking of which, I managed to get my hands on the actual transaction history of the Coca-Cola direct stock purchase plan we setup for my youngest sister and that I occasionally mention as a case study. When I gifted her the first share, I made my father custodian so he could handle everything while I was off at college, meaning I had never done a really intense analysis of the paperwork. It took me several hours, but I built a spreadsheet with every transaction the account ever registered other than the initial gift (which is not included in any of these figures as it is still held in the form of a physical stock certificate).

My figures a few years ago when we discussed this were much too conservative. Coke has performed far better than I thought because the contributions were lower than I anticipated, meaning more of the account value came from investment growth. It turns out that after I bought her the share, nobody did anything with the DRIP for several years. They didn’t begin making cash donations until July of 2004, at which point automatic monthly investment withdrawals were put in place, plus a few bigger cash gifts to make up for the prior years as a sort of catch-up “oops … we should have been doing this”.

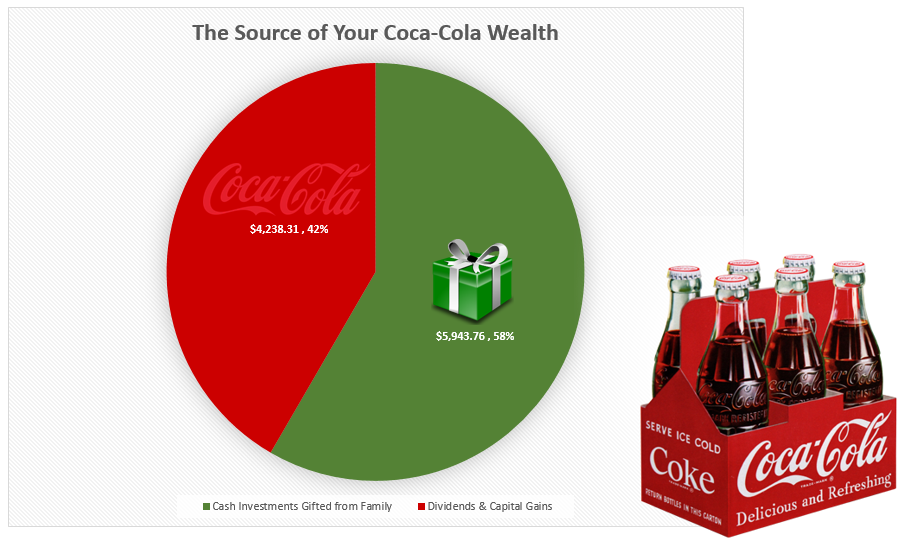

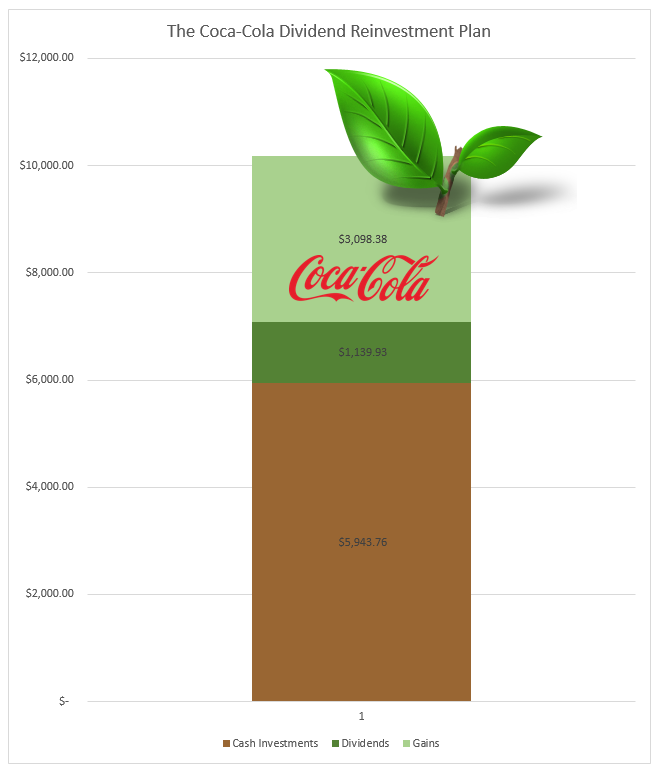

To be precise, excluding the initial gift I gave her, the family made a total of 113 cash gifts to my sister’s Coca-Cola DRIP averaging $52.60 per gift. This totaled $5,943.76. The Coca-Cola Company took that $5,943.76 and worked its sugar magic, conjuring up another $4,238.31 in wealth from two sources – cash dividends of $1,139.93 and unrealized gains due to the underlying company growing its intrinsic value of $3,098.38.

As of early this morning at around 4 a.m., her Coca-Cola DRIP had a resulting balance of $10,182.07 in it (plus whatever the initial stock certificate I gave her is worth) .

Visually the source of wealth in her Coca-Cola DRIP account looks like this:

Or, if one prefers a breakdown of the dividends and capital gains, like this (I sometimes review my stocks as trees to use a farming analogy, with the brown being the trunk you planted (original investment), the dark green being the fruit you’ve enjoyed (the dividends), and the lighter green being the growth in the tree itself (unrealized gains)):

Going back to the new trusts, custodial accounts, and DRIPs, I’m just not sure what I want to do, how much control I want to wield, or what I’m trying to accomplish. Part of the problem is the age of the kids. The youngest is two. How can anyone possibly know which structure would be the most effective didactic approach? And then, what about asset selection? If I choose different companies for each person, you have the possibility for wildly different results, which could cause some envy; one kid ends up with $100,000 because Clorox does better than Colgate-Palmolive or whatever it happens to be. You can’t predict these things.

I think maybe this go-around instead of using the direct stock purchase plans, I’ll setup custodial trusts, a brokerage account that I control, and sit down with them as I spend 15, 20+ years building it piece-by-piece, block-by-block as a joint project in which I let them have a very big say. That would be the most flexible way to go about it. I’ll also involve my parents in it so they can constantly make gifts of cash or shares to the accounts (e.g., my mom takes them to Disney World and buys them some new shares of The Walt Disney Company).

I’ll figure it out in the end. I need to put it all aside for the evening. There are too many other things on my agenda, and I would like to get in some more time on SimCity now that the Cities of Tomorrow expansion is released. I want it finished before the end of December, though, so I can start tracking everything in January at the start of the new year.

Reader Comments (15)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Andrew

December 6, 2013

Joshua, on the subject of children (I don't have any yet, but like you I am starting to research very early), you have to look at absolute terms of the quality of life before getting into specifics right?

I'm someone who is quite worried about our country. I constantly wonder if the "free" America is going to be an old tale and memory. I wonder if capitalism and the free market will survive.

I was wondering if you heard of the concentration camps that are being set up around the country?

http://beforeitsnews.com/alternative/2013/06/us-concentration-camps-fema-rex-84-programs-2687970.html

Needless to say I'm a little concerned. It's very difficult thinking about growing my business. I'm just starting out. I understand life isn't fair, but is being a slave inevitable for my children? Do I ignore it and focus on business?

Thank you very much.

-Andrew

Paarthurnax

December 6, 2013

I think it's absolutely great that your taking the time and effort to make this happen for your family. if it were me, I would recognize that there are two goals that this project is aimed to achieve, and that attempting one solution to achieve both outcomes may not work quite as well.

You want to teach the younger generation about investing. And you also want them to have a prosperous future. Could you not create your family investment entity for the reasons you mentioned above, than have perhaps a much smaller DRIP style plan or similar that will allow you to sit down and teach them about the fundamentals as they grow up?

Even a few hundred bucks of "learning" funds is plenty for them to learn the concepts of valuation and making sound choices. Let them have considerable input on what happens with this small fund and if it flops, than they can learn not only from their mistake without breaking the bank, but that could also be an opportunity to learn that it's okay to not succeed the first time, so long as you keep getting back in the saddle and trying again. Perseverance is perhaps one of the best things you could teach them.

Andrew

December 7, 2013

Replying to Paarthurnax

These children are blessed to have Joshua in their life. I hope they grow up to be wildly successful, in every aspect.

Paarthurnax

December 7, 2013

Replying to Andrew

They are, though that also puts a bit of weight on Joshuas shoulders. A successful life is the freedom to pursue anything your heart desires while also being able to contribute to society in a positive way.

Being a key figure in the family that inculcates the future generation with quality traits is a big responsibility. My hat goes off to you, Joshua, in taking on that challenge with zeal!

Joshua Kennon

December 9, 2013

Replying to Paarthurnax

That may very well end up being what I do. For now, I have the basic custodial trusts, expiring at 21 years old in Missouri, setup under the UTMA law, and we made an initial donation to it as an early Christmas gifts for the kids. It lets me get started with small amounts as I buy time figuring out the big stuff.

I'm actually at my desk in the home study at the moment reading over a template for a trust since I am not ready to go to sleep, yet, and figured I'd keep working on it. At least I was, until I got sidetracked. I can't help but think I wish I had the power to un-do the mid-1980's tax reform; then I could break out a very old and (these days practically unused) type of trust called a "Clifford Trust" that allows you to put productive property aside, with the beneficiary receiving the dividends during the period before it all reverts back to the grantor. That led me to researching them since it's been awhile, which led me to the December 31st, 1964 edition of the California Law Review article called Clifford Trusts: Use of Partnership Interests as Corpus; Leaseback Arrangements. It's all out of date now, but the stacking of trust benefits with family limited partnerships caught my eye.

LordSquidworth

December 6, 2013

You could start by avoiding garbage sites like that.

Andrew

December 7, 2013

Replying to LordSquidworth

Do you think it's a lie/not real? (Serious question.) I would be HAPPY to be wrong.

Though, I seen YouTube videos...

It was on a few sites. If it's all wrong then these comments should definitely be deleted. I have no personal proof. It was a serious concern. I'm just starting out in my business life, yet I have (or maybe my generation has) this mountain of tension and worry about the government. Too many things adding up...

Why try to become financially independent (here?) if it's going to be ripped away from us? One great thing I learned from this site is to be prepared though! Diversify all over the world, so if any one country has a problem, you could move.

It just sucks because I LOVE this country...Will do more research.

Lord Squidworth

December 7, 2013

Replying to Andrew

Considering their photos look fake/recolored WWII era photos...

They have a reputation for censoring anything that doesn't follow their line of propaganda...

Yeah... it's a lie/not real...

Andrew

December 9, 2013

Replying to Lord Squidworth

I apologize for disagreeing (since I very much wish this wasn't true), but there is just too much evidence of martial law about to take place in the U.S.

Training through out the country that specializes in gun seizures in urban areas. Indefinite detention without a trial (insanity). Prolonged Detention (thrown in prison till you die for committing a crime even a decade in the future). A massive influx of domestic authority ammo. Domestic tanks. Drones getting the go-ahead to take out Americans. Country-wide gun bans being pushed. 40 BILLION dedicated to increase domestic military media. Domestic authority being trained not to give warning shots. The constitution disintegrating before our eyes. This isn't fiction!! I terribly wish it was!

This is Holocaust 101. I'm very sorry, but Hitler did this exact thing literally. I highly doubt the Jewish were expecting it to be as bad as it was. They had nothing to compare it to. We do.

I'm as skeptical as they come, but some of these people who work with the DHS are horrible, horrible people who have absolutely zero respect for our constitution. You can quickly look it up. I'm not saying this to exercise my fingers. I'm saying this because I care. We are long term investors. We are naturally conscious of the future. Martial law will undoubtedly hurt our investments. I'm angry because I'm just starting out in my life and don't have enough time to diversify into other countries.

(But...this blog is way too positive to have this conversation...I deeply apologize. I'm desperate for someone intelligent to talk to about this...someone who knows history...this mountain of evidence something terrible is happening.....feel free to delete..)

joe pierson

December 9, 2013

Replying to Andrew

You are what you eat, and you think what you read.

Choose your sources wisely.

Andrew

December 9, 2013

Replying to joe pierson

What I said in my post was wrong? Because there are quite a lot of sources...various news outlets. The Gov's official laws themselves. Government officials. Various blogs. Youtube videos. I get that lies are rampant on the Internet and cable, but truth does exist...It's not 100% lies.

...I don't really understand what you mean.

But alright I think this is enough on this topic here. I don't think anyone wants to hear it.

Adam

December 7, 2013

Any opinion on how to manage things from the other end? What would you do if you were trying to help parents/grandparents structure investments and assets already in place?

Stanley

December 16, 2013

Just a question. Under IRS, I am considered as a non-resident alien for tax purposes, and thus subjected to 30% of withholding rate (my country is not eligible for the the tax reduction that comes with filing a W-8 Ben form). Being a student, I have yet to have any income, although I think I would be able to invest $50 into the plan monthly with my saving.

I can relate to the feeling of money pouring into the bank, and watching your dividend grow because of a decision made years ago.

However, I have read the brochure for DRIP and was surprised that there is a $2 fees for automatic fund deduction, and an additional fee ($0.03) for every share purchased. Of course, $2 is not a very huge sum, although I'm not sure if it's a good idea to pay 4% on fees which could instead go to contributing to my portfolio.

So should I start on the DRIP plan now, given my circumstances? Or should I wait till much later, where I am able to contribute more, making the $2 fees negligible but missing out on earlier days of compounding?

Also, the 30% withholding fees - does it make sense to invest in Coca Cola, or should I look elsewhere to invest where the tax do not take that huge a chunk? (I tried looking into contributing into Roth IRA Plan to avoid the 30% withholding fees, as Joshua have written in his About.com post, but alas, it would seem that it was only open to US resident)

Bill

September 2, 2014

Joshua,

I was wondering if you could give us an update on this topic? My two boys are 5 and 3, and I've been trying to decide how/when/where I should start setting some money aside for them, and to teach them how to invest. This post of yours gave me some thoughts, but I'd like to see what you've decided (if anything yet). Thanks

-Bill

Sean Dobberstein

February 20, 2015

This is awesome that you are doing this for your younger relatives! Any chance you could post a sample spreadsheet (without actual figures of course)? I'm just curious how you set them up and organize them. Also, those graphs are pretty awesome if I must say so myself!