We Are Approaching the Nestlé ADR Dividend Date!

Now that the dividend has been paid on the Swiss shares (April 22nd), the stockholder meeting concluded (April 16th), and Citibank is working with the Swiss Tax Authorities to distribute all of those beautiful Swiss Francs shipped over from Vevey to the United States for holders of the ADR to receive their U.S. dollar equivalent payouts later this month on May 29th when the process has completed (can you believe it’s already been a year since the last time we had this conversation?), I wanted to write about Nestlé. The corporation comes up about once every six months, including the historical case study of long-term returns a few years ago, because it is the embodiment of a certain type of blue chip stock that is so far out of the league of other firms operationally, financially, geographically, culturally, competitively, and from a diversification perspective, it is the perfect teaching tool in a lot of respects. You could easily design an entire graduate-level course covering areas as diverse as corporate valuation, the culture code, war-time considerations for international positions, currency exposures, cost accounting methods, risk minimization through the use of legal structures, and brand equity risk all using Nestlé as the central subject (those of you who enjoy corporate histories should pick up the book I bought back in 2013 for your own library).

As should surprise no one, thanks to businesses as diverse as Nescafe coffee to Gerber baby food, Purina pet food to Coffee Mate creamer, Kit Kat candy bars to Häagen-Dazs ice cream, Perrier sparkling water to Carnation sweetened condensed milk, Nestea to Tombstone frozen pizzas, Hot Pockets to Lean Cuisine microwavable dinners, and dozens upon dozens of other subsidiaries, the payout of the world’s largest food conglomerate has been lifted, yet again, despite significant currency headwinds that make underlying performance look worse than it was (the U.S. Dollar and the Swiss Franc have seen huge increases in value relative to other fiats as people around the world have engaged in flight-to-quality, creating a situation where actual local operating performance is superior than it would appear on the translated financial statements).

[mainbodyad]

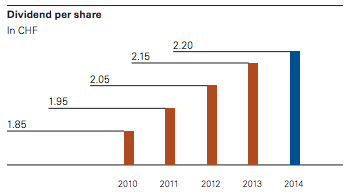

Specifically, the cash dividend has gone from 2.15 CHF per share to 2.20 CHF per share, a modest increase of 2.3% (I was hoping for at least 2.25 CHF but such is life). This follows last year’s increase from 2.05 CHF to 2.15 CHF, or 4.9%. That means in the past 24 months, the payout has risen a total of 7.3%. On a stock price of 72.55 CHF, the new 2.20 CHF dividend represents a dividend yield of around 3.00% which, for reasons we have discussed to exhaustion in the past, hardly any of the financial portals are displaying correctly; e.g., Even in its native Zurich-traded, Swiss shares, the Financial Times website is showing a dividend of 1.43 CHF with a 1.97% yield. Here in the United States, Yahoo! Finance shows the ADR as having a 0.00% yield with no dividend. It’s all total nonsense.

Over the past five years, the annual dividend has increased from 1.85 CHF to 2.20 CHF, or 18.92%. During this same period, Switzerland experienced a cumulative net deflation of 0.49%. Had the dividend merely kept its purchasing power equivalent, it would have needed to fall by half a cent. Instead, it increased 35 cents. In other words, it was all purchasing power gain. That is a testament to the quality, and globally diversified nature, of the underlying businesses. (Which are as excellent as ever. Excluding goodwill, return on invested capital came in at 30.4%. With goodwill, it is 10.8%.)

The stock had grown so cheap, quietly falling as the underlying earnings continued to advance, that at one point during the year it was yielding what would now equal roughly 3.60% on the new payout rate. In a world of near zero percent interest rates, holding the premier packaged food giant on the planet with that kind of cash production is not on the list of one’s life regrets. As I wrote you back in November, it was a time to buy more shares of Nestlé; how we were once again looking at the phenomenon that had played out numerous times in the past century wherein the enterprise never seemed to be the best investment in the upcoming twelve months, but somehow, with few exceptions, almost always ended up one of the top performing corporations over the subsequent twelve years.

Then, suddenly, as many of you no doubt recall, the Swiss central bank shocked the currency markets by removing the peg between the Swiss Franc and the Euro, causing the value of the former to increase substantially relative to the value of the latter since it is inherently a superior, safer monetary unit for a variety of reasons including the prudence and discipline of the Swiss people who implemented the now-famous “Swiss Debt Brake“; a constitutional restriction on government spending that includes sufficient flexibility to avoid austerity during recessions and depressions. Though the increase relative to the dollar was more modest, shares of Nestlé rose in U.S. dollar terms as a result. This was a double-edged sword for those of us who own the firm. On one hand, our existing shares, were we to sell them, and dividends, were we to spend them, gave us more purchasing power here at home. On the other hand, buying additional shares of ownership – and almost all of us are net accumulators, even if we plan on gifting everything to our children, grandchildren, nieces, nephews, favorite charities, or alma matter – was now more expensive. First world problems, I suppose.

A Look at Nestlé’s 2014 Operating Performance

Ignoring the profits from the sale of 48.5 million L’Oréal shares as part of an asset swap that gave Nestlé 100% ownership of a joint venture in the skin care industry, as well as the tremendous noise in currency translation rates as a result of the global economic environment, underlying earnings per share increased 4.4% in constant currencies. Of this, roughly half was real, internal growth in unit sales and half came from pricing increases. Financial analysts have aptly described this performance as “decent” in light of a difficult industry environment, which I think sums it up nicely. Most don’t expect the stock to go anywhere for 3-5 years, telling their clients to look elsewhere. (Again, these otherwise smart people are responding to incentives. If a client were to ask the right question, namely, “Can you give me a list of 10 businesses that, were I to own them at today’s prices, would provide the highest probability of earning 8% to 12% compounded over the next 25 years due to having a strong balance sheet to guard against deflation, inherent pricing power to guard against inflation, geographic diversification to reduce political, currency, and cultural risk, and low rates of technological displacement to reduce the risk of a kid in a garage putting it out of business, all of which work together to permit me to naturally build a substantial deferred tax advantage, leveraging my results?”, Nestlé would be on the roster. Few ask that question, though, even though that’s the question that can make them rich in the long-run.)

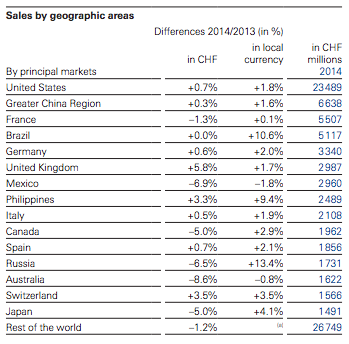

The currency headwinds I mentioned earlier are brutal in most countries as the Swiss Franc demonstrated its superiority. In the United States, sales were up 1.8% in U.S. dollar terms but after being translated into the now-stronger Swiss Franc, appeared to be only 0.7%. In China, practically all of the year-over-year increase was obliterated. In Canada, a 2.9% increase turned into a 5.0% decrease. In Australia, a minor 0.8% decrease turned into an incredible 8.6% decrease. In Japan, sales increased 4.1% but were translated back to the income statement as a 5.0% decrease. None of this bothers me because the academic data coming out of the world’s premier business schools over the past few generations has conclusively shown that most currency translations, despite stomach-dropping volatility from year-to-year, end up working themselves out so that it’s cheaper, if you have the time horizon and liquidity not to bother, to avoid paying for currency hedges.

The currency headwinds I mentioned earlier are brutal in most countries as the Swiss Franc demonstrated its superiority. In the United States, sales were up 1.8% in U.S. dollar terms but after being translated into the now-stronger Swiss Franc, appeared to be only 0.7%. In China, practically all of the year-over-year increase was obliterated. In Canada, a 2.9% increase turned into a 5.0% decrease. In Australia, a minor 0.8% decrease turned into an incredible 8.6% decrease. In Japan, sales increased 4.1% but were translated back to the income statement as a 5.0% decrease. None of this bothers me because the academic data coming out of the world’s premier business schools over the past few generations has conclusively shown that most currency translations, despite stomach-dropping volatility from year-to-year, end up working themselves out so that it’s cheaper, if you have the time horizon and liquidity not to bother, to avoid paying for currency hedges.

If anything, I expect Nestlé’s management team to take advantage of the situation, using the now-appreciated Swiss Francs to gobble up discounted global competitors. The numbers may look ugly but it’s good from a purchasing power perspective for long-term owners. (This is just part and parcel of owning Nestlé. At the stockholder meeting last month, Chairman Peter Brabeck-Lemathe told his fellow owners that, “as long as the Swiss flag flies over our corporate buildings, Nestlé will stick with the Swiss Franc.”)

Nestlé Chairman Peter Brabeck-Lemathe Tells Stockholders That Warren Buffett Has “Pulverized the Food Industry Market”

Speaking of him, among the more reported comments from Nestlé’s management at the stockholder meeting were those of the aforementioned Chairman Peter Brabeck-Lemathe who said, “3G and Buffett have pulverized the food industry market, particularly in America with serial acquisitions,” and “3G’s partners are known in our industry for ruthless cost-cutting and have already proven numerous times that they are capable of reducing operating costs in particular by between 500 and 800 basis points, which has a revolutionary impact on all the other members of the industry.” [Source]

Management then essentially vowed to owners that it would begin using Nestlé’s size and resources to go to war if necessary; that it will remain the top food company in the world. It’s easy to take them at their word. If Nestlé felt like it were backed into a corner, losing to rivals, it could unleash tremendous damage on competitors. It has a non-assailable balance sheet, scale, and scope that makes things like the Buffett-backed venture look cute in comparison, and, despite a generally genteel attitude, can operate with a ruthless efficiency that few others can match.

To put into perspective how gargantuan and powerful Nestlé is, think about Warren Buffett’s Berkshire Hathaway empire for a moment. It holds one of the largest railroads in the world, delivering 15% of all inter-city freight in this country as measured by ton-miles; one of the largest energy groups in the world, which comes in as the biggest regulated utility operator on the planet serving customers in eleven states, producing 6% of the United State’s wind generation capacity, 7% of its solar generation capacity, pipelines that ship 8% of the nation’s natural gas, electric transmission businesses in Canada, electric companies in the United Kingdom and Philippines; all of those retailers, all of those manufacturers, all of those real estate brokerages, car dealerships, leasing operations, and newspapers; its incomprehensibly large insurance group, which in turn holds much of the firm’s 14.8% ownership in American Express, 9.2% ownership in Coca-Cola, 4.5% ownership in Deere & Company, 3% ownership in Goldman Sachs, 7.8% ownership in IBM, 12.1% ownership in Moody’s, 11.8% ownership in Munich Re, 1.9% ownership in Procter & Gamble, 1.7% ownership in Sanofi, 5.4% ownership in U.S. Bancorp, 2.1% ownership in Wal-Mart, 9.4% ownership in Wells Fargo, and will-be-executed 700 million share stake in Bank of America. It goes on and on and on and on.

[mainbodyad]

Now, imagine for a moment that Buffett wanted to merge it with Nestlé in an all-stock deal at today’s market prices. He wanted to take all of those enterprises, which he’s amassed over half a century, and merge it with one final business.

By the time the transaction closed, Nestlé would represent roughly 41% of the new consolidated firm, dwarfing any and every subsidiary in the Berkshire Hathaway family. All of those other holdings together were just barely more than Nestlé by itself. And the only reason the latter isn’t bigger is because, unlike Berkshire Hathaway where Warren has retained 50 years of profits (other than that odd 10¢ dividend back in the 1960’s he jokes was declared when he was in the bathroom), Nestlé has been shipping much of the after-tax earnings to shareholders in the form of dividends and buybacks for the past few generations.

It is the Berkshire Hathaway of food, with dozens of powerhouse subsidiaries run on a de-centralized basis, tons of cash, rock-solid finances, and sophisticated executives. Were an economic war to break out in the packaged food industry, my money is on Nestlé. It’s won since the 1800’s and it’ll keep winning in 2015. There are too many forces aligned in its favor. Even the Oracle of Omaha would wither under its might. If push came to shove, it wouldn’t be unthinkable for Nestlé to buy Kraft-Heinz outright, shedding any problematic assets that could create regulatory issues. It won’t cede its ground. It never has and I doubt it ever will, at least in its present form. A far more likely scenario would be a breakup along product lines, spawning all sorts of new corporations a la Standard Oil or Ma Bell.

A Quick Note on Nestlé’s Direct Stock Purchase Plan

As always, I expect Nestlé to be the domain of the staid; a cornerstone of portfolios for those who like getting richer without much excitement. Case in point: Unlike most other firms, the stock hasn’t had some spectacular run over the past seven years because it never collapsed along with everything else back in 2009. It just kept going, fluctuating within its normal percentage range as if everything were perfectly calm. On average, the share price alone climbed at around 9% per annum, excluding reinvested dividends, from its mean high and low price in 2008 just prior to the collapse through today. Throw back in the dividend and you get your 11% to 12% total return figure despite what looks like a flat stock chart. History repeats itself. Again. Nobody cares. The oddness of the situation never gets old to me. Right there, in a nutshell, is the investment problem with having most ordinary people manage their own money. It’s so deceptively simple – so stupidly easy – that it just … sits there, in plain sight, making long-term owners wealthier like clockwork while being shunned by practically everybody except pension funds and value investors. “What did Nestlé do last year?” “Oh, nothing much.” “What did Nestlé do over the past seven years?” “Oh, produced a total return at the top-end of historical equity performance.” It’s hilarious to me.

Speaking of which, I meant to tell you! Nestlé’s direct stock purchase plan for the ADR allows U.S. citizens to buy shares directly for $0 in commissions and only a 10¢ per share processing cost as long as you promise to sign up for minimum automatic investments of $50 or more per month, taken right out of your bank account. They’ll let you buy up to $100,000 per year through the plan, keeping your expenses at virtually zero. You can instruct them to automatically reinvest your dividends or have them direct deposited into a linked checking or savings account when they arrive each year. Enrollment online takes a few seconds if it sounds like your cup of Nestea. (Sorry … I couldn’t help myself.)

The only kicker? You have to have one share directly registered to take advantage of this near-free investment method. Here is what I’d do: Go to a broker like Charles Schwab & Company and buy a single Nestlé ADR for a commission of $8.95 or whatever it is in a plain-vanilla brokerage account. Under Schwab’s current commission schedule at the time of this post, you can have paperless entry in the Direct Registration System done for $0 (as opposed to paper stock certificates, which now carry a nuisance fee of $500+ to try and force investors to stop using them). Order out the share so you hold it through the DRS. Once that is done, you’re on the books, eligible for enrollment in the DRIP, and the whole thing cost you less than a movie ticket. It’s a tiny inconvenience (that, frankly, Nestlé should fix as most big companies have these days) but you’ll then be able to make voluntary casit’s worth the few minutes it takes to get it done given the ability to dollar cost average into shares every month at what amounts to virtually no expense.

Important Update: A huge thank you to fellow Nestlé owner Christopher M., who contacted Citibank/Computershare about this today. It turns out, the bank has an outright, inaccurate error on its DRIP page showing Nestlé had begun offering dollar cost averaging for free when this is not, in fact, the case. It still only allows voluntary cash contributions for a flat $5 per order + a couple of pennies processing per share. While this is no doubt a great deal, especially for those who want to periodically write a check for more ADR throughout the year and treat it as if it were a private family business, it’s incredibly disappointing as I thought they had finally gotten their act together and made it easy for long-term owners to acquire shares through regular deductions of their checking or savings account each month. As of Tuesday, May 12th, 2015 at 11:57 a.m., CST, the bank has not corrected the summary page of the DRIP with the error visible to the public despite knowing it exists.

I have uploaded the official, correct Nestlé DRIP prospectus in Adobe PDF for you to read so you can get all of the terms and conditions. In the meantime, maybe we should push Citibank/Computershare/Nestlé to offer this. There is clearly an interest. There is no reason they can’t sponsor a program akin to what Exxon Mobil does, which remains one of the single best DRIPs / Direct Stock Purchase Plans I’ve ever come across (check it out – setup fee: $0, dollar cost averaging fee: $0, voluntary cash purchase fee: $0, batch processing fee: $0 … they pay for nearly everything to encourage accumulation of stock over years and decades.) If the investor relations department can’t do it on its own, it wouldn’t be terribly difficult to get a proposal brought up at the general meeting. There is no rational objection to this so I don’t see why the board would be adverse to something that added true, long-term, buy-and-hold owners to the ranks.

Licensed Image Credits: MAHATHIR MOHD YASIN / Shutterstock.com

Reader Comments (33)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Engineer7006

May 11, 2015

I'm quite suprised by the following:

http://www.nestle.com/investors/faqs/faqslanding#howmany

That Nestle estimates that only 250k people in the world are shareholders as of 2013. I'm happy to be one of them.

As to wierd dividend displaying info, RDS.B never seems to display correctly either, except on the dividend page for nasdaq. It throws off my estimated portfolio dividend on a website I use, but thats what spreadsheets are for!

MIke B

May 11, 2015

Replying to Engineer7006

Engineer,

Agreed, It's good be a holder of Nestle!

It says "number of shareholders probably exceeds 250,000". No doubt there is more 250k of holders. It's hard to estimate the number of people owning in a "street name". I.e. in their brokerage account. At the same time is probably not all that high.

Nestle is not going to make it many people's radars. It's based in Europe, only pays a dividend annually, foreign tax credit issues, requires currency conversations to better understand financials, etc etc. It never occurred to me to buy until reading about here. Thanks Josh for pointing it out.

No kidding on the RDS.B, their dividend is often screwed up too on financial sites. You're 100% right, best to visit the NASDAQ dividend history and use your own spreadsheet.

Ang

May 11, 2015

Josh, newbie question, it's probably because I'm dense, but I've looked into computershare before for Nestle, and it's only a dividend reinvestment plan, which means if you don't already have shares, you can't participate (I think it's a display error by Computershare as when you try to go through the site, it doesn't allow you to direct purchase shares, only reinvest dividends on shares you already own) - is it possible to buy more shares outright if you already have one share through computershare? (In other words, buy more shares using contributed money and not just dividends received)

EDIT: Nevermind, I answered my own question after browsing through the plan forms - voluntary cash contribution is an element of the plan

Joshua Kennon

May 11, 2015

Replying to Ang

If Nestle is still requiring a single share prior to enrollment (which it seems like they are and makes little sense as most companies have abandoned this to allow direct stock purchases for the initial stake, too, these days - maybe someone should write the board of directors), there's a quick way you can do it for less than $9 if you use a mainline broker like Charles Schwab & Company. I added the details to the end of the post right around the time you were typing this question after I had responded to an inbox message asking the same thing. Just make sure whatever broker you use to order out the single share into the DRS does so at a $0 fee and you should be golden.

Once you're eligible for, and enrolled in, the DRIP, you can do voluntary cash purchases (for a $5 commission I think it is - that is, if you wanted to send off a one-time pile of money to buy a block of stock by writing a check or having a lump sum taken out of a linked bank account), or you can do dollar cost averaging for amounts as small as $50 per month automatically taken out of a checking or savings account, which will cost you $0 (Nestle pays the commissions) plus a few cents processing costs per share.

WT

May 12, 2015

Replying to Joshua Kennon

It seems that DRIP isn’t cheap. It will cost me $10 if I want to buy 100 shares. It only makes sense if I invest less than $5k every month on Nestle.

Ang

May 12, 2015

Replying to WT

I must be confused - the terms are $5 for cash purchases and 0.03 for each share, so 100 shares should cost you $8?

Eugene

December 29, 2015

Replying to Joshua Kennon

Joshua, you seem to contradict yourself here. In the article, you mention that you cannot do free dollar-cost averaging (only $5 optional cash purchases), but it in this comment you mention that it is possible with $50/month automatic contribution. What is the actual case?

Joshua Kennon

December 29, 2015

Replying to Eugene

Practically all dividend reinvestment plans these days differentiate between so-called "cash" purchases, which are optional one-time investments in which you either send in a check or have money automatically taken out of your bank account, and so-called "automatic" purchases, which are where you set up regularly reoccurring withdrawals from your bank account (e.g. having $150 on the second Tuesday of every month automatically withdrawn from your checking account like an auto-pay bill, only the money is used to buy more shares in your DRIP account). The latter encourages long-term ownership, demonstrates a commitment to the business, and, from the company's perspective, increases the likelihood that you are serious about treating this like an investment, not trading the stock. As a result, companies will often subsidize automatic purchases that are part of an on-going dollar cost averaging plan by doing it for free or a reduced fee, while optional cash purchases cost more (though still cheap on an absolute basis). If you wanted to dollar cost average with smaller amounts, you would need to take advantage of the automatic investment enrollment and not try to manually send in money except to the extend you had enough to justify it; e.g. you decide to kick in a few hundred extra dollars on a whim knowing the cost will be amortized over the holding period of the optional purchase.

When I get to my desk later, I'll see if I can word it more clearly in the post to avoid confusion (right now I'm on an iPad, which is more difficult to use when navigating the backend of the blog).

Eugene

December 29, 2015

Replying to Joshua Kennon

Thanks Joshua. I called up Citibank today and spoke to an adviser there who confirmed that after one is enrolled as a Nestle shareholder (1 share or more of Nestle ADR (NSRGY) in your name), they do offer ongoing automatic investments for $0.10/share for a minimum of $50/month investment. Since Nestle is such a great investment, but also a bit tricky to navigate, would you consider writing a post to walk through it? There's the part of buying 1 share in your name, enrolling in the plan through Citibank, filling out the right form to bypass the 35% Swiss withholding rate and get a lower rate through the US-Swiss tax treaty, etc.

Thanks!

Eric

May 11, 2015

Too bad you can't defer the 35% Swiss withholding tax through the dividend reinvestment plan. Looks like the 35% still gets taken out of your dividend, then the net amount is reinvested into new shares.

Joshua Kennon

May 11, 2015

Replying to Eric

Fill out the right form and certify your U.S. tax identification number (either SSN for an individual or EIN for a corporation, partnership, limited liability company, etc.) and you should be able to lower the withholding rate substantially to take advantage of the lesser 15% withholding rate American investors can claim under the U.S.-Swiss tax treaty.

Tom T

May 11, 2015

I have not had a chance to look at the current valuation

yet. It's harder for me to find data on them since it appears to be a pink

sheet due to the ADR status. Nasdaq.com,

FINVIZ, the sites I like to use to analyze a company don’t have data on the

company. I guess I will have to go

straight to the 10-K?

Is it a good buy at at its current price, or it is a good buy because most everything else is overpriced....

Joshua Kennon

May 12, 2015

Replying to Tom T

Unlike Diageo in the U.K. or Sanofi in France, Nestle never bothered to sponsor a Level III ADR in the United States. They are so big, and so powerful, they don't need to raise money here. The rich and long-term-oriented stockholders of the world will find them in the same way that Coca-Cola doesn't bother to sponsor an official stock market listing in China or India. If someone wants to own Coke, they're going to learn to read GAAP and analyze 10-Ks. They're going to find a way to buy shares on the NYSE in the United States. Same thought process. Nestle doesn't come to you. You go to Nestle.

Nestle is a Swiss-based firm with its stock traded on the Zurich stock exchange. It is valued in CHF. Its accounting is (properly) done in IFRS not GAAP. It doesn't file a 10-K (which are only for domestic U.S. companies) or a 20-F (the equivalent of the 10-K only for foreign businesses that have higher level sponsored listings here, allowing them to raise capital and issue new shares to American investors). Its audited financial reports are published in this format (PDF), instead.

That means you have to look at the actual stock symbol if you want to research it - the one over in Zurich. It's 16.19x earnings, with a 3.01% dividend yield, a 21.79% ROE, a stock price of 71.80 CHF, and a market capitalization of 236,055,410,000 CHF.

If you try to pull the ADR quotation, you aren't going to find much. It - the one trading OTC in the U.S. under ticker symbol NSRGY - was put together by Citigroup for the sake of convenience. In simplified terms, the bank went over to Switzerland, bought a bunch of the real Zurich-traded Nestle stock, bundled those shares in a trust fund of sorts, then setup a domestic ticker symbol for the trust. When you buy 1 NSRGY ADR what you're really buying is a receipt proving that you own 1 Zurich-traded share in Citigroup's vault (or these days, an electronic entry on a ledger). If you want, you can pay a fee and break the ADR, taking delivery of that underlying share any time you feel like it. In the meantime, as long as you hold the stock through the ADR intermediary, when the dividends are paid in Swiss Francs, Citigroup will convert it all to U.S. dollars for you, file the paperwork with the Swiss Tax Authority, lower your withholding rate to 15%, and then pay the converted dividend out, earning a small fee in the process.

That's why you're coming up with nothing when you try to research it. The ADR is just a legal entity between you and the actual share. The actual share, the ownership in the business, is over in Zurich. You need to be looking at that ticker symbol. It can seem confusing because other ADR - again, Diageo and Sanofi are good examples - actually register with the SEC for a Level III listing so it effectively functions as a primary stock exchange listing much like domestic businesses. You can pull up DEO or SNY and see most of what you need to see just as you can with KO or PFE. Not so with NSRGY. Different things entirely. There really should be a new term or some sort of easily identifiable ranking system. Most investors don't encounter it frequently enough to matter, I suppose, because almost all Americans who own Nestle do so through some sort of Vanguard International Index fund or something, where the portfolio manager is paid to know these sorts of things on their behalf, allowing them not to think about it.

Steven

May 12, 2015

Replying to Joshua Kennon

I always find it amusing that the Swiss stock exchange has dashes in the domain name.

Generally when I see a site with a name in that format I immediately think its a bogus one, I guess that sentiment doesn't prevail in Switzerland!

Erich

May 11, 2015

Nestle looks like it could be a good long term compounding machine. However, it does not look undervalued currently and is probably not a good buy at the moment.

Brendan

May 11, 2015

Thank you for clarifying how to get over the first share hurdle in order to enroll into the direct purchase plan. As I transition from index funds to direct stocks, that's a handy bit of info to have.

Scott Thomas

May 11, 2015

So is it a bad idea to hold Nestle in an IRA? The 35% dividend withholding is partially recoverable in a taxable account, but apparently not in an IRA. So in an IRA, you would love 35% of the dividend. But, you wouldn't have to pay dividend tax on the remainder of the dividend, so does that sort of balance things out? Would love to hear what you all think about owning Nestle in an IRA vs taxable account. Thanks for a great article, and thanks for any thoughts.

Rob

May 12, 2015

Replying to Scott Thomas

Hi. Joshua answered a similar question of mine last December. It can be found in the comment thread of this article:

https://www.joshuakennon.com/im-building-ghost-ship-portfolio-someone-sort-index-fund-steroids/

Ang

May 12, 2015

Replying to Scott Thomas

Foreign stocks for the most part (with the exception of structures like RDS-B, where there is no withholding tax) are best held in a taxable account so you can get the tax credit annually. 35% is higher than any dividend tax rate you would be subject to in the US, mathematically, it's better to hold in a taxable account

Bo

May 12, 2015

I have this discussion quite regularly with my brother in law. If you have acces to buying about 20,000 different businesses via your broker, why not pick the best businesses on the planet and become a long term owner in them? The awnser is always "I'm looking for that quick 10% pop". Which means he's continuously trading on his phone, looking for Chinese tech IPO's and gambling with options. He's not even a dumb guy, went to college, has his own small software company, hard worker, very rational, just not with his investing. The stock market does weird things to people I guess.

My investing strategy is more an accumulation process, buying great businesses for fair prices and holding them for the rest of my life, making sure the dividend I receive every year keeps growing. I want the money to keep raining down on me.

This picture just hits the nail on the head in my opinion: http://i.imgur.com/QJxFD.jpg

jerkstores

May 17, 2015

We've got a brand new baby boy who was born 9 days ago. There's no better stock to get for teaching the kid about business and investing. And if I'm going to be buying him taxable stock I might as well do it in one that wouldn't benefit from being inside an IRA.

Joshua Kennon

May 17, 2015

Replying to jerkstores

Congratulations!!!!!!!!

dave (nestle)

May 18, 2015

Replying to jerkstores

HEY DADDY!

Congrats!!

No greater dividends in life to enjoy than the ones our kids can pay us.

Nirav Desai

June 28, 2015

Replying to jerkstores

I had a baby girl born in Feb. I used the Swiss franc fiasco as a good excuse to pick up a 100 shares in January.

Joshua, you're right about there being no better stock to teach a youngster about investing.

Colin

May 27, 2015

"The Plan Participant Accounts are not insured by the Federal Deposit Insurance Corporation, the Securities

Investor Protection Corporation, or any similar agency."

Why do investors in the Dividend Reinvestment Plan not have SIPC insurance like they would with a brokerage account? Should investors be concerned about this and what would happen if the transfer agent went bankrupt?

gebhot

May 30, 2015

Just wanted to point out that Nestle has been hauled up by the Indian FDA for excessive amounts of lead and also MSG in its Maggi noodles. I guess the contribution of the Indian arm of the giant is minuscule to the total, but still something to watch out for..

Matt

June 10, 2015

Unfortunately it seems that Capital One Sharebuilder can't properly process the foreign tax withholding for Nestle, as I recently found out.

"Regrettably we will be unable to process dividends from NSRGY correctly in your ShareBuilder account. This is due to two issues impeding our ability to fulfill those residence requirements.

The first being that we do not have a direct route to either DTC or the company’s transfer agent to communicate that these shares are held in an account that has provided that information. This is because ShareBuilder has an omnibus clearing arrangement with Pershing LLC. The second problem is that our back office systems and databases are not currently programmed to identify specific accounts that have designated that exemption when processing dividends. These are concerns we are working to resolve in the future for the benefit of our customers.

Please consider the importance of this stock in your portfolio as the foreign tax withholding will effectively reduce your yield. It is worth noting that in a taxable account where you could take a foreign tax credit on your US return, the effect would be the same. That is, the full dividend would be reported on a 1099-DIV along with the foreign tax paid, which you’d take as a credit, so the net of the dividend includable in your income would be the same as the amount left in your account that will be taxed to you as ordinary income when you withdraw it sometime in the

future."

***

That last paragraph also seems wrong since the excess 20% withholding appears to be unclaimable according to the IRS in point #1 here.

Not sure what I can do to fix this, but this is just a heads up in case anyone was thinking of purchasing shares through them. The shares I hold with other brokers were processed correctly without issue, but apparently Sharebuilder cannot correctly process residence requirements.

Steve Roberts

June 10, 2015

Do you hold NSRGY in an IRA or taxable account? It sounds like you have them in an IRA in which case you would "lose" the foreign tax credit.

Matt

June 10, 2015

Replying to Steve Roberts

Nope its in a vanilla brokerage account. There's supposedly something with the way the brokerage is set up (they are not self-clearing) that doesn't let them do it right. Or at least that's what they claimed.

Steven

June 12, 2015

Does anyone know how much the ADR paid in dividends this year? I'm having trouble figuring it out.

Some sites say it was $2.32...but doing the math on my holdings (before various ADR fees and foreign dividend tax) it is coming out at somewhere between $2.27 and $2.28.

Could the $2.32 be based on the exchange rate with CHF at the time the dividend was declared, rather than the time it was paid?

If anyone who can shed some light on this - or post what the math shows in their account - would be appreciated!

Rob

June 13, 2015

Replying to Steven

Hi,

$2.27 before the 15% tax hit ($1.93 after). Current yield after tax, 2.57%

Kapitalust

June 16, 2015

Any thoughts on the recent lead contamination reports in Maggi products in India?

I wonder if there has been compromised tests at the laboratory that conducted the initial tests that showed lead ppm to be above regulated levels? I wonder if the ingredients in the product were grown in areas with higher concentrations of lead? I wonder if the water used in the factory that produces the products have higher concentrations of lead? I wonder if there might be higher overall concentrations of lead around India? More instances of leaded gasoline? Is this some sort of manipulative politics to pull attention away from something else? Is Nestle allowing lax standards for profits? Many ideas fly through my head trying to figure out what factors might be at play. I guess we need to wait for independently verified tests to come out.

But in the mean time, interested in your thoughts!

Steve

June 17, 2015

I've been attempting (unsuccessfully) to order a Nestle Annual Report for some deep analysis. Does anyone know how to obtain this on paper, or is it only an online document?