Union Pacific: A Company That Looked Expensive But Was Undervalued

The developments on the income statement and balance sheet of Union Pacific between 2005 and 2013 are an excellent example of why it is important for you to analyze data yourself, and come to conclusions based on reasonable, rational, intelligently organized facts. The willingness to take action when others do not agree with you, and to have your action backed up by solid evidence, can make the difference between being comfortable and ending up rich. Two of the world’s wealthiest titans demonstrated this truth, not only when buying shares of Union Pacific, but other railroads, as well.

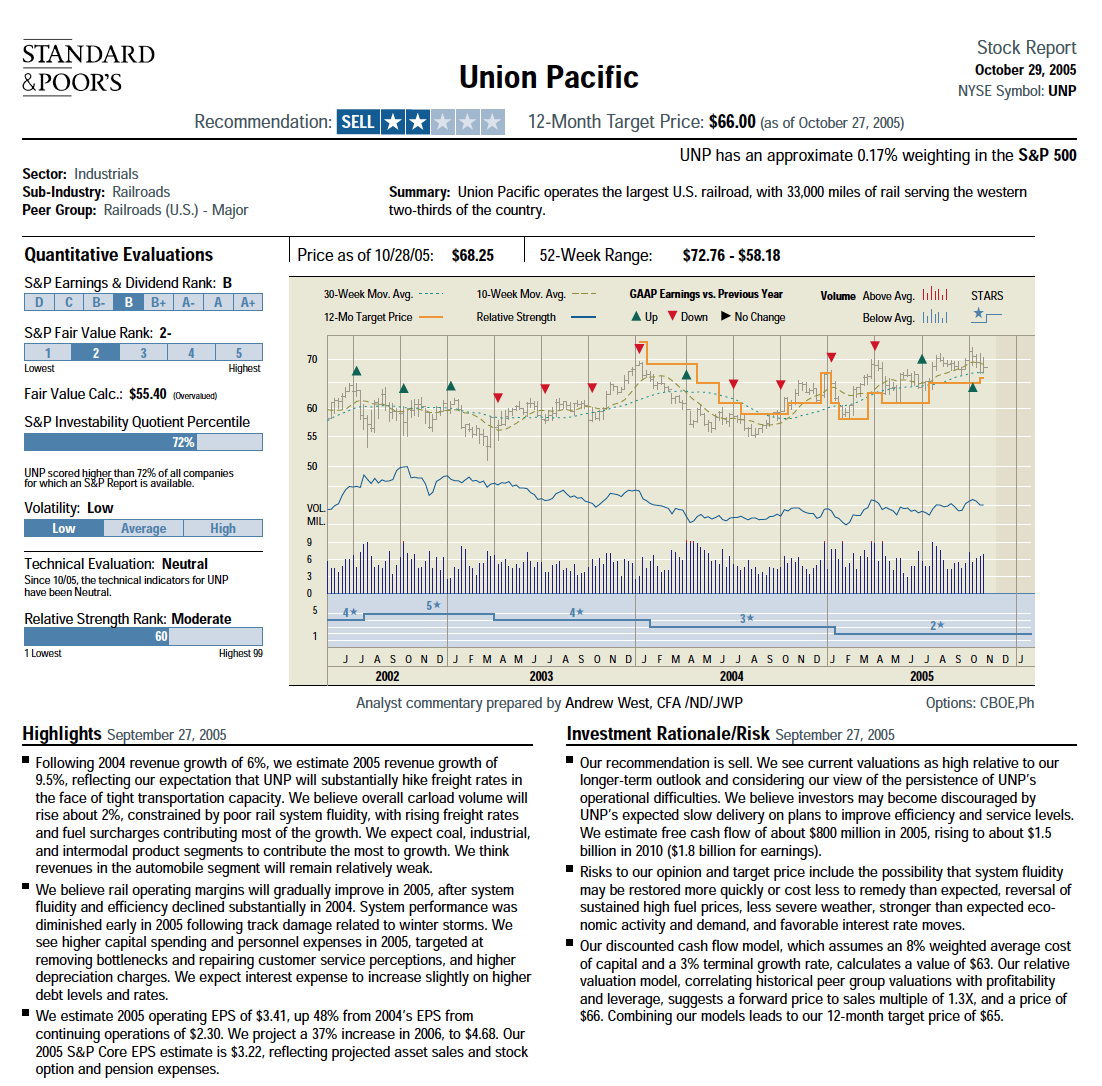

First, the back story. In 2005, the major analysts on Wall Street had sell ratings (extremely rare) on railroad Union Pacific, which appeared to be trading at more than 22 times earnings. Returns on capital appeared relatively low. The dividend was nothing exciting. Volatility was low so it wasn’t a stock traders found exciting. Yet, Union Pacific was still important because it was the largest railroad in the entire United States, having 33,000 miles of track at the time, serving roughly 67% of the nation.

Old Union Pacific Report – Please note that the stock has since had a 2-1 split so the figures in modern charts are divided by half. That is, Union Pacific at $66.25 in 2005 is the same as Union Pacific at $33.13 today.

The stocks did appear expensive. However, at the same time, aggregate track miles in the United States had fallen substantially, productivity improvements had resulted in much more efficient cost per ton carried, and there were only a handful of carriers left in the nation. At some point, the pricing power had to shift to the railroads, which would then have an enormous influx of new earnings that weren’t being accounted for anywhere in the analysis.

Putting their money where it counts, Bill Gates had been buying up shares through his private holding company, Cascade Investment, LLC, and his friend, Warren Buffett, had been doing the same through his holding company, Berkshire Hathaway. It was basic supply and demand. Warren Buffett later said in an interview how dumb he was for not spotting it years earlier, as Bill had. It was sitting there, right in plain sight.

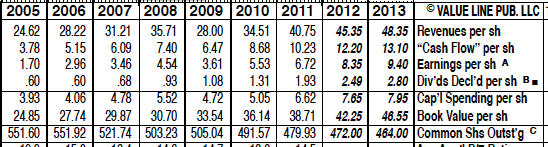

Sure enough, the pricing equation did change and it became much cheaper to ship by rail car than truck fleet as oil prices climbed ever-higher. Union Pacific split it stock once, 2-1, during these years. In today’s terms, earnings per share went from $1.70 to an expected $9.40 this year, an increase of 553%. Cash dividends of $12.42 were paid out since then on a split-adjusted stock price of $33.13, meaning 37.5% of the purchase price has already been shipped back to the investor; akin to a rebate on purchase cost.

Management rewarded stockholders by using additional surplus funds to reduce outstanding shares by 87.6 million through share buy backs. By the end of the period, 1 share represented the same ownership that roughly 1.19 shares would have back in 2005. In essence, the Board of Directors took cash that could have been sent to you as a dividend and reinvested it for you so that your shares represented a greater percentage of ownership in the firm.

In the aftermath of the 2008 panic and meltdown, Warren Buffett used the opportunity to buy the entire Burlington Northern Santa Fe railroad, making it a wholly owned subsidiary of Berkshire Hathaway. Last year, the railroad generated $4 to $5 billion in pre-tax profits for him to reinvest; a very high return on the original shares he purchased. By focusing on how much cash the business should be earning 5 to 10 years in the future, and not the current financial statements alone, he made enormous sums of money for his stockholders.

It’s the old saying made famous by hockey star Wayne Gretzky: Go where the puck is going to be, not where it is. A horse and buggy manufacturer would have looked cheap when Ford was developing the Model T, but it was doomed. That doesn’t mean it would be a bad investment – it’s entirely possible the firm could have been put into run-off and drained for dividends to reinvest elsewhere; at a low enough price, the returns could still be very high. You have to think about these things.

You Don’t Have To Catch Every Great Idea – You Just Need a Few Big, Good Ones In Life

I remember sitting in Omaha during the shareholder meeting almost a decade ago in 2005, listening to Buffett and Munger talk about railroads. I never did buy any shares of Union Pacific or Burlington Northern Santa Fe (though I now own the latter through my Berkshire Hathaway stake). At the time, I was using all of my surplus cash to acquire stock in Direct General, which was bought out by a private equity firm, Yankee Candle, which was bought out by a private equity firm, and AutoZone, which was trading for around $83 during this period and $374 today. (I sold most of the AutoZone stake years ago for a large gain to fund other investments in the private business that have since made significantly more. It isn’t an exaggeration to say that AutoZone was one of the stocks that helped fund a lot of my early activities. I have a deep fondness for that company.)

When I first came back to the Midwest after graduating from college and wasn’t sure exactly what I wanted to do first, my parents let Aaron and I setup office in a corner of their old factory building. I spent most of that first year reading annual reports, buying additional investments, and building the foundation of what would later become our major cash generators.

With a family background in retail, the automobile parts retailer made more sense to me than the railroads did. I could see that even if the business never grew, management’s penchant for waiting until the stock was cheap and then buying up massive blocks to destroy was going to result in the shares compounding at about 15% as long as I paid less than $91 to $93 at the time. I could see that there weren’t many serious competitors and that people would want to go to a specialty store rather than something like Wal-Mart if there were a car problem. Whenever it was below my intrinsic value price, I’d write checks. I’d pick up $4,000 here or $12,000 there, draining my bank account. My parents’ office in those days, where they let me put a desk in the corner between the time I came home from college graduation and setting up my own business, was across the street from an AutoZone. I’d walk out into the parking lot and watch the cars pull up to the store, feeling just as much an owner of it as I did the other businesses I held.

I was too young and inexperienced to spot the railroad economics. I got Yankee Candle. I got Direct General. I got AutoZone. They made sense to me. Even though my childhood heroes were buying shares of the railroads, I refused to acquire stock because I did not understand the dynamics of the enterprises at the time. Never buy something you don’t understand. If you miss the opportunity, that is okay. The world is full of opportunities. Find something that makes sense to you. The United States economy alone generates more than $15 trillion every year. There are not a shortage of ideas or operations. There is no pressure to act. Take your time, find the right match, and only proceed when the words of Benjamin Graham and David Dodd in the 1934 edition of Security Analysis ring true: “An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.”

You have to think. Some companies look like they are generating a lot of profit today, but it isn’t going to last. Other companies don’t look as profitable, but the industry is undergoing a transformation. Still other firms are as close to timeless cash generators as can exist in an uncertain world.

Reader Comments (3)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Michael Starke

February 19, 2013

I would love to see a post with a more detailed explanation of your thoughts on holding cash versus full investment. With my (relatively) small portfolio, I've focused on getting some return rather than holding out and finding "the best" return.

I liken the problem to NP-Complete Problems (http://en.wikipedia.org/wiki/NP-complete_problems#Solving_NP-complete_problems) in Computer Science. The gist being that there are algorithms for solving "complex problems" in the optimal way, that are so computationally expensive that the run time increase superpolynomially (the complexity, c, for input size n, when expressed as a function of n increases faster than a polynomial expression, e.g. c = F(n!) (n-factorial)), making the algorithm unsuitable for solving anything but the smallest of input sets. Instead, we fall back on tricks (like randomization, heuristics, etc.) for achieving suitable run times. This can lead to a "good" solution that approximates the optimal solution.

It would seem to me that this could be another case where the perfect is the enemy of good. If I know a set of companies, and have found no new issue to invest in, is it irrational to instead of waiting, and sitting on cash, to invest in the best thing I know about at the time? If my "elephant gun" is not yet sufficiently large to actually do appreciable damage, am I better served just continuing to make small wins and improving my yield on cost?

TheLonelyHumanist

February 20, 2013

Rail was the future 200 years ago and rail is the future today.

FratMan

May 15, 2013

"Warren Buffett later said in an interview how dumb he was for not spotting it years earlier, as Bill had."

I'm curious: Does Bill Gates call most of the shots at Cascade, or does Larson? I'm curious as to whether Gates is the selector and Larson is just the administrator, or whether Larson gets the authority to make investments with Bill's money.