[mainbodyad]

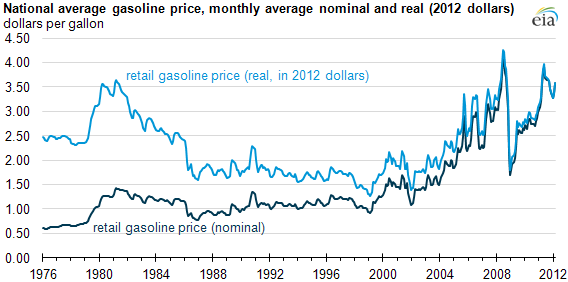

With all of the talk of gas prices falling, I’m reminded of the situation a couple of years ago when fuel costs were on an upward trajectory. Everyone from the little old ladies at church to major economic commentators were lamenting the “record high” energy expenses. Very few people noticed that, as per the U.S. Energy Information Administration data, the actual cost of gasoline in inflation adjusted terms was still very cheap up until the height of the real estate bubble. Though the nominal prices of $4.22 per gallon on the West coast, $3.48 per gallon in the Rocky Mountain region, and $3.83 per gallon nationwide were high in dollar terms, they weren’t some unprecedented catastrophe.

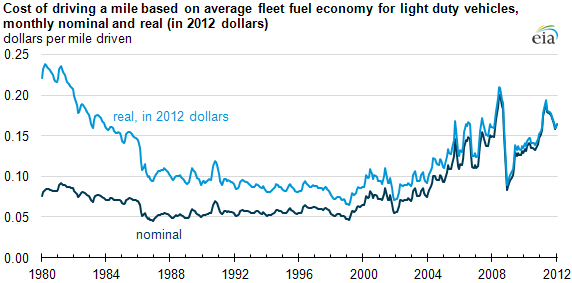

Even that was deceptive. In this case, the inflation-adjusted price of a gallon of gasoline wasn’t the metric that should have mattered. Gasoline is merely a tool to power cars. Cars are merely a tool to transport people. Thus, what counts, is the inflation-adjusted cost of gasoline per mile driven.

One of the cheat codes for success in life is to make sure you are measuring the right things. As Peter Drucker and Henry Ford both put it, “What gets measured, gets managed.” When you begin to ask yourself, explicitly, what you are measuring in your personal life, your business, your portfolio, you’ll often be surprised at how many mistakes are being made around you.

Get the measurement right and you can make better, more informed decisions. Make better, more informed decisions and you can exponentially raise your output and returns, moving toward your goals with greater ease.

[mainbodyad]

Image Credit for Featured Image on Blog Archive: humbak / Shutterstock

Reader Comments (2)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Zaphod

January 8, 2015

Exactly. Excellent post. Such an interesting graph. This points out why its worth it to take two seconds to do a tiny bit of research yourself. If we relied on others or the news for the state of the world we'd be fooled into thinking everything was spiraling down in all categories....when we can look at data and see though it isnt perfect there has literally never been a better time in the history of the world.

Benny Cohen

April 22, 2016

Thank you joshua