Vanguard Accused of Dodging Nearly $35 Billion in Taxes – Expense Ratios May Need to Quadruple According to Expert Report Submitted to IRS

Please note that as a result of the conversations and questions in the comment thread, I reorganized, rewrote, and significantly expanded this post on Sunday, December 6th, 2015 at 2:20 p.m. If you read it prior to this time, you may want to re-read it because it is a far different piece that gets into the specifics of transfer-pricing regulations and potential outcomes for existing investors in Vanguard for the sake of providing greater clarity to those who want to understand the mechanics of the tax dodge / abuse allegations.

From August 2008 to June 2013, David Danon was an associate attorney in the tax department at the Vanguard Group. According to a whistleblower lawsuit filed with the State of New York, which served as the basis for additional whistleblower actions filed with the State of Texas, the State of California, the Securities and Exchange Commission and the Internal Revenue Service, Danon was silenced, and ultimately sent packing, after he persistently warned management that Vanguard was committing a massive tax dodge by using a combination of legal entities and improper pricing structure; an arrangement that went back 40 years. Danon claims that others who had raised similar concerns had also left the firm after facing a backlash for refusing to toe the line on what they believed was illegal behavior.

According to the whistleblower documents (you can read the complaint in PDF here), this alleged tax dodge is one of the key reasons that Vanguard can offer drastically below-average expense ratios. Aside from threatening the very existence of Vanguard’s business as it currently operates, it could also open the door to claims of on-going violation of anti-trust regulations meant to ensure fairness in the marketplace should competitors and regulators smell blood in the water.

Is any of it true? I have no idea. It’s definitely something to at least keep on your radar with major news outlets now reporting on it. For now, let’s look at what the accusations are given the information that has been released to the public so we can attempt to make sense of them.

To Understand the Accusations Against Vanguard, You Must Understand the Basics of Transfer-Pricing Tax Law

First, let’s step back and discuss what Vanguard is accused of doing.

In the United States, we operate using a hybrid form of regulated free market capitalism. We do this because laissez-faire capitalism doesn’t work unless you have certain reset mechanisms in place that keep things fair for consumers and competitors; that avoid monopolistic abuses; prohibit industry collusion; stop us from becoming a landed aristocracy in which, after a generation or three of successful individuals accumulating resources, it becomes impossible for others to enjoy upward mobility based on effort due to all of the levers of power and capital becoming concentrated in the hands of a few operators, investors, and/or their heirs that can then erect barriers to entry that make it practically impossible for upstarts to flourish.

There are all sorts of ways we achieve this as a civilization. For example, your local power company must, by definition, almost always be a monopoly because otherwise it wouldn’t be economical. Why build two multi-billion dollar power plants when only one will do? We, as a country, don’t want bankrupt facilities of that magnitude and danger being run on a shoestring budget so, instead, we established rate boards of citizens and specialists who guarantee the utility companies certain minimum profit levels in exchange for hitting service metrics. We establish gift taxes and estate tax limits and exemptions so those who didn’t earn their wealth can’t inherit ungodly amounts of power and influence without restraint. We denote certain transportation facilities and technological infrastructure as “common carrier”, taking away the ability of the operators to discriminate against customers. We establish civil rights laws and rulings that prohibit discrimination based upon certain personal characteristics.

Comparably, one of the protections we have in place is that a business must charge a fair price for its products or services. Here, there are two areas that often get confused:

- Consumer and Competitor Protections – Things such as the Federal Trade Commission (FTC) using its authority, including under laws such as the 1890 Sherman Anti-Trust Act that arose during the Gilded Age when monopolies threatened to take over certain industries and undo many of the benefits of free market capitalism, to ban predatory or below-cost pricing (you can’t just charge whatever you want for a product or service, especially if the goal is to gain market share and drive competitors out of business), forbid manufacturers, distributors, and retailers from tying the sale of two products together under certain situations, restrict certain exclusive supply or purchase agreements, prevent mergers and acquisitions that could lead to effective control of an industry, and punish those who engage in so-called “Refusal to Deal” violations (e.g., if you own the town newspaper, you can’t refuse to carry ads for the town radio because they are a competitor).

- Tax Protections – These are rules governing the way profitability is calculated, and the formulas that must be used, in order to prevent a firm from cheating the civilization of the tax revenue it is rightfully owed; tax revenue that provides the military that protects its corporate assets, the infrastructure that makes it possible for workers to show up in the morning; benefits such as limited liability against employees, operators, and investors if things go south.

At the moment, Vanguard is being accused of violating the second part of those protections – the tax rules (if that turns out to be the case, it very well could open it up to claims of the first type of violation). Specifically, the whistleblower appears to be claiming that Vanguard has committed an on-going 40 year tax dodge involving something known as transfer-pricing.

It is an esoteric area of tax law that is vitally important now that we live in a world of multi-nationals. Transfer-pricing regulations benefit every citizen. These rules prevent a company such as Starbucks from setting up a foreign affiliate that owns the licensing rights to the Starbucks name then charging the U.S. operations licensing fees to the point it has no remaining profits to be taxed. This is accomplished by establishing minimum profitability guidelines and rules that must be followed when entering into transactions between controlled affiliates.

Typically, when dealing with a controlled affiliate, a firm must follow transfer-pricing rules such as those found in 26 CFR 1.482-5 – Comparable profits method. In essence, and grossly oversimplifying the calculation (there are a handful of approaches and variables that also can be used including the so-called “cost plus method” and “profit split method”), a company is required, by law, to charge its affiliates the closest comparable market rates excluding its own operations when setting its prices. In other words, it must deal with its own controlled affiliate based on a calculation that most closely approximates the prices it would have to pay if it were an arms-length, third-party transaction with an independent contractor. The accounting and auditing techniques to ensure this has been done properly includes tools such as the Berry ratio, which analyzes gross margin divided by operating expenses.

To give you an idea of the scope of transfer-pricing, a quick reference guide created by leading accounting firm PWC for tax year 2013/2014 covered almost 900 pages. Go take a look at it yourself in the source PDF. It governs everything from setting prices on affiliate loans to selling equipment from one subsidiary to another. Again, these rules help prevent someone with a pen and a lot of time from playing the game in a way that you and I have to pick up their costs while leveling the playing field in other ways. Without them, you could simply set up a firm in Ireland, have it “loan” all of the money you use in your domestic operation at an extraordinarily high interest rate, and then suck the effective profit out via interest on the loans, leaving the manufacturing business at break-even while enjoying the profits, earned in the United States, that have now been transferred overseas. (It is a very different thing from another area we have discussed in the past, which is legitimately earned foreign taxes, which have already been subject to taxation after being earned within that foreign jurisdiction, being unfairly targeted for taxation, again.)

Agree with it or disagree with it, those are the rules. While it may occasionally lead to some regulatory headache, it’s an otherwise rational approach to protect the integrity of the free markets by keeping certain firms from gaining unfair cost advantages and protecting the taxpayer from certain firms abusing the rules to lower or eliminate their tax bill, sticking everybody else with higher costs.

What Is Vanguard Accused of Doing?

Whatever internal documents Vanguard’s former tax attorney turned over as part of the whistleblower case purport to show that the mutual fund giant has 1.) failed to follow the required standards that must be used in transfer-pricing transactions for the calculation of taxable profit, and 2.) used multiple legal entities to artificially deflate its remaining earnings (tied to a $1.5 billion contingency reserve that has made headlines) in an effort to reduce effective would-be taxable profit further so it pays the government practically nothing. If true, this would result in the firm itself having an enormous, immoral market advantage as it would be mathematically impossible for it to set its fees at their current rates were they not committing tax abuse as well as allowing Vanguard investors to steal from the rest of society, sticking everybody else with a bill that they should have had to pay. These advantages, over long periods of time, would have been responsible for it taking over much of the industry. The whistleblower claims that employees who discovered the specifics of the alleged abuse, and brought it up to management, were silenced or laid off.

In essence – and, again, I’m going to need to oversimplify it here given the complexity of transfer-pricing rules – Vanguard is accused of point-blank refusing to follow the tax laws for the sake of lowering fees for its owners, who, if true, would now be enriched by the tax dodge. Under the tax law, it appears as if its affiliates should have been charging the mutual fund and index funds under its management market average rates. This would have caused substantial income tax to be owed on the money that was legitimately earned within the United States as well as forced it to compete more fairly with other asset management companies such as Fidelity and Schwab, which are presumably following the rules and being put at a disadvantage because of it.

Following the tax laws would not have been incompatible with Vanguard’s mission to provide lower-than-average costs because Vanguard is owned by its investors rather than outside stockholders. That means it could have opted to distribute some of those higher accounting earnings to investors in the form of dividends, somewhat akin (the legal, accounting, and tax parallels aren’t appropriate but from a practical economic standpoint, you’ll see the similarities) to a mutually owned insurance company paying a dividend to its policyholders or a co-op paying a dividend to its members. That is, if you held a lot of money in something like a Vanguard S&P 500 index fund, had Vanguard been ethically behaving in compliance with the law, your expense ratio might have been substantially higher but you would have been sent a big dividend check for your pro-rata share of the Vanguard profits in your capacity as an owner. It wouldn’t have been as large as the current proceeds received from the alleged tax abuse but it would have still been substantial.

Expert Report on the Vanguard Tax Allegations for the Past 8 Years Alone Put Underreported Profits at Nearly $71 Billion with Taxpayers Shafted by Almost $35 Billion

To support his claim and estimate the potential tax dodge (remember that, in no small part due to the abuses, coverups, and frauds of the past quarter-century, Congress passed laws allowing whistleblowers to share in any recovered money, rewarding them for potentially ruining their career and social life as well as incentivizing them for bringing tax cheats to light), the former Vanguard tax attorney-turned-whistleblower went to a respected international tax expert, Dr. Reuven S. Avi-Yonah, the Irwin I. Cohn Professor of Law and Director of International Tax LLM Program at the University of Michigan, asking him to prepare a report for the IRS and SEC.

Before we get into the findings of the report, to give you an idea of the academic’s credentials, which demonstrates the reason his opinion carries so much weight in this field, here are some of the highlights from his University of Michigan biography page. He:

- Has served as a consultant to the U.S. Department of the Treasury and the Organisation for Economic Co-operation and Development (OECD) on tax competition

- Is a member of the steering group for OECD’s International Network for Tax Research.

- Is a trustee of the American Tax Policy Institute

- Is a member of the American Law Institute,

- Is a fellow of the American Bar Foundation

- Is a fellow of the American College of Tax Counsel,

- Is an international research fellow at Oxford University’s Centre for Business Taxation.

- Has taught at Harvard University (Law)

- Has taught at Boston College (history)

- Practiced law with Milbank, Tweed, Hadley & McCloy in New York; with Wachtell, Lipton, Rosen & Katz in New York; and with Ropes & Gray in Boston.

- After receiving his BA, summa cum laude, from Hebrew University, he earned three additional degrees from Harvard University: an AM in history, a PhD in history, and a JD, magna cum laude, from Harvard Law School.

- Has published more than 150 books and articles, including Advanced Introduction to International Tax (Elgar, 2015), Global Perspectives on Income Taxation Law (Oxford University Press, 2011), and International Tax as International Law (Cambridge University Press, 2007).

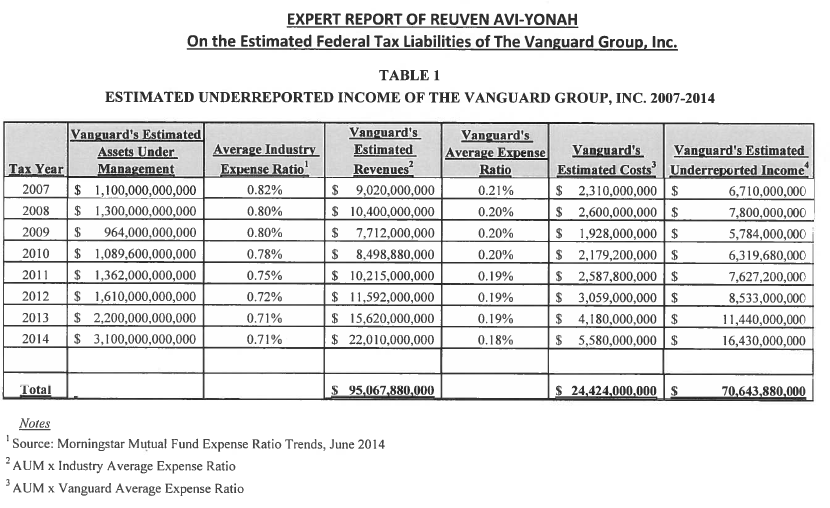

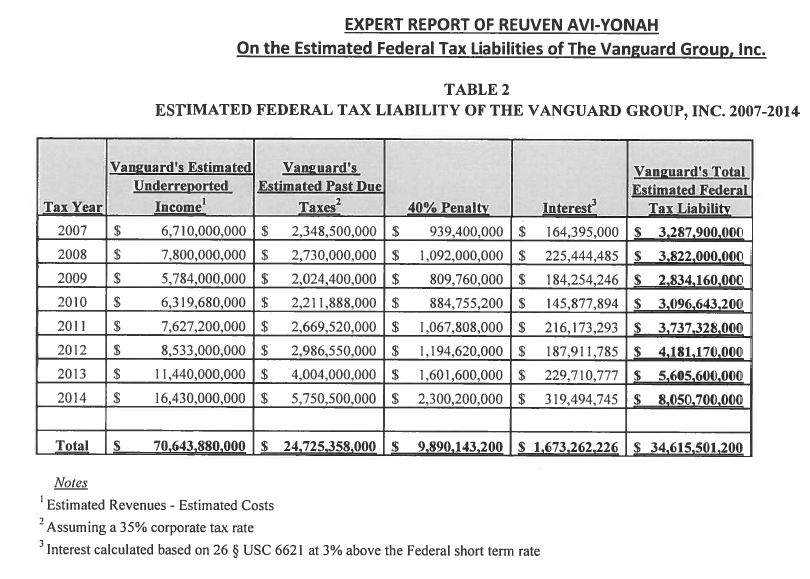

The report is damning. (In case you want to read it for yourself, I have made a PDF version available to download here for your convenience.) Dr. Avi-Yonah conservatively estimates that Vanguard owes nearly $35 billion in back taxes, penalties, and interest for the past eight years alone (I could be mistaken – I need to check a regulation before stating this to be fact – but I believe the report limits the total tax bill to this period because the statute of limitations had run out on the alleged violations that might have occurred in the previous 30+ years so there was no point in going back further as it was inconsequential to the issue of what would be owed today were Vanguard held accountable).

In fact, in his opinion, the transfer-pricing tax violations are so evident to him that he pulls no punches and outright, unequivocally states, “If the IRS were to pursue this matter, it will prevail in court” (emphasis added).

Specifically, Dr. Avi-Yonah’s calculations indicate that, at a very minimum, Vanguard should be charging expense ratios of 0.71% to 0.82% on its internal fund management arrangements under the transfer pricing rules. (Whether you are agree with or disagree with the transfer pricing tax regulations is inconsequential on this point. There are rules for the calculations and Vanguard is being accused of simply refusing to abide by them because it doesn’t feel like it. That isn’t how the rule of law works. You can’t walk into an electronics store, steal a television off the wall, and then go home and brag about how it was moral because of all the money you saved your family members.)

Even still, the IRS might find that the 0.71% to 0.82% is a conservative estimate because the rules require the use of industry-wide expense ratios which have been driven down, in no small part, due to the need to compete with Vanguard’s artificially compressed price structure made possible by the alleged tax abuse. In other words, if Vanguard hadn’t been supposedly cheating in the first place, expense ratios wouldn’t have been that low and would need to be increased. Nevertheless, even with the conservative estimate, between 2007 and 2014, Dr. Avi-Yonah calculates for the SEC and IRS that Vanguard underreported its profit by a jaw-dropping $70,643,880,000. With past due penalties and interest, this represents an unpaid tax liability of $34,615,501,200.

Startled by the enormity of the charges, journalists who have been looking into the case have been seeking comment from other experts. One reporter, Joseph N. DiStefano, took the findings to another tax specialist, Robert Willens, whom he called “a prominent New York business tax attorney”. (That’s an understatement. Willens has been named one of the one hundred most influential CPAs in the country, serves as an adjunct professor of finance and economics at Benjamin Graham’s alma mater, Columbia University, was the chairman of the committee on revision of corporate tax laws for the American Institute of Certified Public Accountants, has published several tomes on corporate taxation, and remains a sought after specialist for complex tax situations in corporate America.)

DiStefano recounted Willens comments as, “”It seems like a pretty clear-cut case,” “I know Vanguard says they have meritorious defenses and special circumstances that might excuse them. But the principle in law is that they have to deal with their funds at arm’s length,” and the funds must pay Vanguard’s management company fees as if they were paying an independent contractor, not a special low price”. Willens went on to say that he doesn’t think the IRS will be inclined to use its power to put Vanguard out of business, but instead, seek a settlement that would cause Vanguard’s expense ratios to “absolutely” rise. [Source]

What Does This Mean for Vanguard’s Investors?

It appears to me that Vanguard’s response to the allegations was to declare war on the whistleblower. From what I can tell, it sent its lawyers to court and all but said that what they were doing wouldn’t have been uncovered if their tax-attorney-turned-whistleblower hadn’t been so disgusted by the alleged abuse that he broke the attorney-client privilege. (In other words, had he been a tax accountant, who isn’t bound by confidentiality rules, it could proceed to trial but because he was a tax attorney, he wasn’t allowed to speak about the things he learned.) Using this technicality, Vanguard got his lawsuit thrown out of court, avoiding having to go to trial; a trial which would have been high-profile and involved watching its internal documents on full display for the world to scrutinize. However, the judge made a point of saying “she wasn’t ruling on the merits of Danon’s allegations and that her actions didn’t affect the state’s ability to pursue them”. He is appealing. [Source].

Unfortunately for Vanguard, the New York outcome doesn’t do them any good with the potential SEC and IRS investigations, either or both of which could have far-reaching ramifications for the firm as well as the financial markets. It also doesn’t do them any good in the other states. Texas paid Danon $117,000 as a confidential informant after Vanguard agreed recently to pay millions of dollars in back taxes as part of some other situation that has not been fully disclosed. The California case is still pending.

Broadly speaking, I think there are five potential outcomes entirely aside from the issue of back taxes that may or may not be owed:

- No Wrong-Doing Is Discovered and the Status Quo Remains: Vanguard might be found to have done nothing wrong by any of the regulators and courts that have it under its microscope. I strongly hope this is the case because I have so much admiration for John Bogle and what he has done. At the moment, however, the reaction of the firm, and the findings of an expert who is among the best in the world at his discipline as well as other esteemed tax specialists who have looked at the documents, does not give me a lot of optimism.

- A New Type of Non-Profit Exemption Is Created: Vanguard might be able to use its influence and power to get what I consider to be a moral exception written into the law to make it comparable to a mutually owned insurance company such as State Farm or Liberty Mutual (the two largest property and casualty underwriters in the United States). To do this, it would need to add a 30th exemption to the 501(c) statutes that covered asset management operations. It would begin charging reasonable expense ratios to its funds but then it would start paying a dividend to Vanguard investors (who are also the owners) for their share of the pro-rata (now higher and taxed) earnings. The dividend could come in the form of cash or, if it wanted, additional shares of the underlying index funds or mutual funds depending on how it was structured. Vanguard keeps its low-cost advantage despite some absolute rise in costs, Vanguard investors begin enjoying regular dividends from their ownership stake the same way mutually owned insurance companies do, and there is no more immoral or unethical behavior happening as is alleged in the whistleblower claims.

- Politicians Are Bought and Unfair Advantages Remain: Vanguard might be able to use its influence and power to get what I consider to be an immoral exception written into the law to protect its own interest the same way the sugar lobby (and one family down in Florida, particularly) has been able to artificially control cane sugar due to buying politicians and regulators. The investors of Vanguard will continue to benefit from expense ratios that they now know come from cheating their fellow citizens.

- Demutualization and Vanguard Investors (Potentially) Getting Rich: Vanguard decides to demutualize like the waive seen at the end of the 20th century when some of the biggest insurance companies became joint stock corporations and sponsored IPOs. Shares would be allocated to existing Vanguard investors based on a formula that included their relative percentage of assets under management. It would still be possible to keep the place a low-cost operator like Amazon, CostCo, or Wal-Mart due to the corporate culture explicitly stating, perhaps in some sort of Credo akin to the one used by Johnson & Johnson, that their objective is for [x]% of assets under management to be in the bottom [x]% of industry-wide fees. Long-term Vanguard investors who happened to be in before the demutualization might be paying a lot more but their added costs could be dwarfed by the shares they received in the IPO. It could be life altering for people who suddenly found themselves drowning in wealth they never expected. In other words, it very well might turn some long-term Vanguard investors into millionaires overnight.

- Wipeout: The IRS or another regulator agency effectively puts Vanguard out of business. (While it could happen if there is a Teddy Roosevelt working in one of those agencies, I think it is extremely unlikely. There’s no reason to Arthur Anderson the thing.)

I don’t think #4 can happen while John Bogle is alive, even though he no longer runs the firm, because I get the impression his whole ego is wrapped up in the place to the detriment of his rationality, he’s written about his distaste for publicly traded asset management companies in the past, and he still represents an important figurehead decades after he was pushed out of top management due to his age in a high-profile rift. He has enough sway with Vanguard’s existing investors that he could present a major roadblock should he use the power of his pen to criticize any demutualization plan. Would he be successful? I don’t know. Waive enough money in front of people’s faces and they might take it. (If you were a long-time Vanguard investor and suddenly found out that by voting “yes”, you’d receive a block of stock in the upcoming IPO – maybe tens or hundreds of thousands of dollars in free shares deposited into your brokerage account – would you refuse? Not many people would.)

Even if a demutualized Vanguard achieved the same ultimate mission, I think he’s become obsessed with form over function and couldn’t accept it. I can’t see him adapting like Charlie Munger when the Savings and Loan industry became too revolting for him, resigning in a very high profile way back in the 1980’s because it was no longer compatible with his analysis of the right way to behave. Munger will sacrifice his ego for the optimal. He’d tear down his favorite institution or idea if it was proven incapable of living up to his standards. He’d throw out his life’s work if he found a better strategy or construct. As good a man as Bogle appears to be, I’m not sure he can. I think he loves Vanguard in that special way only an entrepreneur will understand and part of that is the legal structure to which it has become wedded.

It’s Going To Be Interesting To See the Cognitive Gymnastics That Occur Throughout the Financial Industry on the Vanguard Allegations

In fact, I’m really interested to see Bogle’s reaction. I think he will swear, and perhaps even believe deep down in his heart, that Vanguard has done nothing wrong. Unless I’ve been totally duped all this time, I truly think he is a man of integrity who wouldn’t knowingly break the law. I’d almost have to conclude, absent other evidence, that he became so obsessed with his mission of low costs that he went down a wrong path to achieve it, succumbing to a temptation that even he warned against in one of his essays (“… recent years have shown us that when ambitious chief executives set aggressive financial objectives, they place the achievement of those objectives above all else – even above proper accounting principles and a sound balance sheet, even above their corporate character. Far too often, all means available – again, fair or foul – are harnessed to justify the ends. [snip] “Management by measurement” is easily taken too far.” See Don’t Count on It! The Perils of Numeracy: Peril #4: The Adverse Real-World Consequences of Counting, Sub-Section: Counting at the Firm Level).

There are some things in Bogle’s recent writings that have given me … pause … to the point that I’ve privately discussed with Aaron my belief that he may no longer be totally objective; not like he was in his earlier days, with his legacy now entirely wrapped up in the overly simplified message that fees are all that count even to the point of rejection of some of the justifications that behavioral economics indicates are relevant. For example, there was a passage in one of his recent books that I thought was more than a little intellectually dishonest; something that would have been unthinkable decades ago. I hate even mentioning it because of my enormous respect for the man – I think in many ways he embodies the concept of “a life well lived” where you contribute to the civilization and serve others – but I think he’s allowed his own “best loved idea”, to borrow a Mungarism as we were just discussing him, to influence his message in a way that is not always positive. This particular passage bothered me because Bogle is a brilliant, Princeton-educated economist who spent his lifetime in asset management where he demonstrated unimpeachable integrity. He was making a point using a particular mathematical relationship that he had have known was not indicative of economic reality due to changes in payout structure and tax laws, but that supported his message on cost. It bothered me so much, I can still remember where I was sitting when I read it. I could understand someone else making the error in good faith but there is little chance he could. It’s beneath him. He is too smart to have to resort to trickery to attempt to convince people of his thesis. In a lot of ways, I think Bogle was, and is, doing the equivalent of “The Lord’s Work” in capital markets so I hold him to a higher standard. Perhaps it’s not fair of me to do so.*

On the flip side, I think you’re going to see some competitors react with glee, perhaps even to the point of distastefulness, if the allegations turn out to be true. For some of these competitors, I have to say: You can’t really blame them. Imagine you were running your business ethically and honestly. You pay your taxes, follow the rules, and compete year after year, decade after decade. They keep beating you on cost but, it turns out, they’ve been lying on their tax return and don’t have this enormous tax bill you do because they are dishonest. Finally watching them get caught, and knowing that their prices are going to have to rise to give you some relief, is a very human reaction. As the experts who have looked at this have conceded, unless Vanguard is found totally innocent or buys its way into an exemption by bribing lawmakers, there is a not-insignificent probability that Vanguard’s expense ratios go up by 400% to around 0.80%. It’s still objectively very cheap and, if combined with either a newly implemented investor/owner dividend or a demutualization as previously discussed, would be far less painful that it sounds at first glance, but it provides more breathing room for Fidelity, Schwab, American Century, and the rest.

I’ve been asked about my thoughts, particularly, given that we are in the process of launching a global asset management company. (I think you are wise to ask these questions; that they are very intelligent because, at least on the surface, it appears that it could introduce a conflict of interest.) To be as blunt as I can about it, and risk offending a few people because I’m going to have to get into issues of socioeconomic status, I don’t think it has any meaningful effect on us either way. Ultimately, you’ll have to answer that for yourself but upon even a cursory examination, it’s a fundamentally different business, focusing on fundamentally different types of clients, providing a fundamentally different experience and menu. Vanguard could quite literally charge 0% per annum on its assets and it wouldn’t have any effect on the compensation system we plan to employ anymore than the availability of free trading at Loyal3 has any effect on what Julius Bär does. The people coming to us do not, and will not, care what Vanguard charges. Vanguard has built an enormous empire appealing to mom and pop investors with relatively small median account balances who have fairly straightforward financial needs. (The firm is somewhat tight-lipped on its entire client base but they do release information on defined contribution retirement plans, of which they are one of the biggest providers. To be specific, in 2014, according to Vanguard’s own numbers, the median participating balance for a retirement account held at the firm was $29,603 [Source PDF, page 5, printed], down from $31,396 in 2013 [Source PDF]. Still, it’s grown nicely since the market bottom in 2009 when the median Vanguard retirement account balance was only $23,140 [Source PDF, page 36, printed number]. Median, as you’ll recall, is the point at which half are above and half are below. In contrast, our expected minimum required account size, absent case-by-case exemptions, is set at $500,000 in investable assets.) The people coming to us, asking to have us invest their money alongside our own, are disproportionately highly successful, often financially sophisticated, individuals and their families. They are fully aware they can buy an index fund, they are fully aware of what the costs will be at the time the paperwork is signed, and in many cases, they have far different needs, objectives, and risks than a typical household, making cost but one variable in an overall decision they’ve reflected upon and made.

In actuality, I find what is happening at Vanguard more than a bit disheartening. It only adds to the ambivalence I’ve felt about it in recent years. In the decade-and-a-half since John Bogle left, there is an arrogance coming out of the firm, especially now that its market share has reached 20%, that could be its downfall. I mean, management forced beneficiary changes on 170,000 client accounts to make their own internal paperwork easier; beneficiary designations that supersede a person’s existing will / estate plans and effectively disinherited who knows how many people. (They now require you to have identical beneficiaries on all identical IRA types, which is an utterly idiotic policy that does nothing but serve their own best interest at the expense of the client.) Still, they’re so much better than many of their competitors, I find myself somewhat uncomfortable criticizing them. If you have, say, $25,000 in savings, you’re not going to find many better options out there if you’re satisfied with the limited range of choices they offer.

Footnotes

*I’ve been asked in the comments about the specifics of the passage. I may try to provide an updated link here in the future.

Reader Comments (54)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

Bob

December 5, 2015

Setting prices at the break-even point is not illegal as far as I know. It is only illegal when you do it to drive out competitors, artificially lowering prices below costs in the present to build up a monopoly and charge higher prices in the future. The passage about "charging prices that are similar to those found in an arms-length negotiation with a third party" is meant to protect consumers (e.g. in the case of companies acquiring monopoly positions to charge higher prices than what would be considered fair), not other companies.

As far as I know, all these laws were put in place to protect consumers. At which Vanguard does a good job in my opinion, by making the market more competitive, allowing investors to earn higher returns instead of the investment companies. Also, I really doubt Vanguard is doing this to drive out competitors with the intention of considerably raising fees in the future. I don't really see how this would benefit the shareholders of the company, which are also the clients of the company in Vanguard's case.

Matt

December 5, 2015

Replying to Bob

Charging prices similar to those found in an arms-length negotiation with a third party is not meant to protect consumers. It is meant to protect the government (and by extension the citizens) from corporate tax evasion (see transfer pricing). The Newsweek article Joshua linked above gives an example of how companies can evade taxes if there are no restrictions on transfer pricing. Note that the argument has nothing to do with consumers, as the consumer pays the same price regardless of whether or not an arms-length transaction has occurred.

Ang

December 5, 2015

Lots to go through here... I think you will probably get more "hate" mail than with the embedded gains discussion (punting two puppies off the bridge this time).

I think it's particularly difficult because it's a "ends justify the means?" question. For all the hand wringing over Walmart driving out inefficient, more expensive neighborhood stores, they did a good thing by lowering costs and improving the absolute standard of living for millions of people. Amazon is now doing the same as far as lowest prices, even if they are playing with their financial statements to retain profitable access to equity markets/employee comp

The hard part is that if you are a rationalist, even though Vanguard is doing a good thing for retirement overall, the way they accomplished it induces a lot of anxiety. I think for most people, in their mind, indexing = Vanguard. It's hard for them to separate the stock index as a concept from Vanguard the company. If Vanguard falls, there will still be other ways to index (iShares, for example). There are so many mental models at play here for Bogle worshippers, so many of them proudly declaring themselves as "cultish". A perfectly knowledgeable and reasonable poster on Bogleheads can declare something innocuous like: "NY or the IRS could still run with the underlying argument, but I don't see where anyone else has the motivation to aggressively pursue a questionable legal theory where the primary beneficiaries of the tactic are millions of American's retirement accounts." without understanding that this issue has nothing to do with the noble effort of offering low costs for retirement accounts - this relates to the superpower of incentives as you pointed out

Perhaps you should bold/emphasize this passage: "(On the plus side, I suspect that some of the effective expense ratio increase could be mitigated because the after-tax profit that remains still belongs to the fundholders under Vanguard’s existing structure. The now-higher could be sent out to investors based upon some formula the same way a mutual insurance company pays policyholder dividends. That is, you might pay 0.71% or 0.82% instead of 0.05% on your index fund but you’d get a rebate check once the annual earnings have been calculated.)" instead of having it as a sidebar, that will at least cut down on the amount of "hate" mail driven by love/halo for Vanguard and inconsistency avoidance

Then I also wonder how places like Fidelity (or Blackrock+iShares) has been able to start offering Spartan funds, which have expense ratios similar to those of Vanguard - is it akin to a loss leader that then allows Fidelity to sell services that are actually profitable? I assume they have already evaluated their own corporate structures after this suit came out. The comp structures seem like black boxes to me - but I'm sure there are resources out there that I just am not knowledgeable enough to access. But in my mind, if Vanguard hadn't "artificially" lowered its expense ratios, ishares and spartan funds wouldn't have followed suit. Evaluating the End and the Means is very tough

Tiffany Alexy

December 5, 2015

I specifically logged on to your site to see if you had anything to say about it, Joshua... and I was pleasantly surprised 🙂 Thank you!

todd

December 5, 2015

Joshua,

I have personally met with a person who Teaches a financial/investment class at a University for lunch one time he found me intriguing, he is a big Vanguard supporter. I brought my paper work to show him how a good active fund beats Index funds. He has been on TV and has written 3 books on Financial Happiness. Even in his book talks about Vanguard index funds. He even has been in the paper trying to get IPER's to switch to Indexing. Since he a big pusher of Vanguard index funds I ask him are you not afraid of something might go wrong at Vanguard he said no that they are to big and well run. I told him a person needs to be diversified not only in individual stock, fund, and fund company's.

Here is my thoughts first if Vanguard is in the wrong then as a investor even the one's that don't have Vanguard may lose. If Vanguard have to raise there fees. Other Fund Family's will feel free to raise there fee's.

Vanguard has been good to all investors by forcing other Fund Family's to lower there fee's to try to stay competitive.

As far as Taxes the government is not good at using our money so the taxes that Vanguard maybe not paying is not be wasted the Vanguard investor will eventually spend there money and pay income tax and sale tax on it. So look and we/they are investing the government money for them. Higher rate of return as in income/sales tax for government in the future.

I would like to know Warren Buffett thinks. Since he has mention Vanguard.

undercover

December 5, 2015

Usually, I'm in agreement with your wisdom on issues that you talk about here. This time, I find myself very uncomfortable as my morals are in total disagreement with yours.

To force vanguard to price services, higher is particularly a tactic right from the villains of Atlas Shrugged.

I don't think am one with wrong morals here. The people making the argument that since this company mission is to offer services 'at cost' to the consumer, that this is somehow scamming the government out of money is outrageous.

I get this ugly feeling what the left calls "fairness" is the root cause of this irrationality.

My solution for people wanting fair-mindedness in the marketplace is to allow more competition. Stop government taxation of business/corporations profits. In other words, a 0 % rate is my answer. Now everyone wins in the financial industry.

Then again, I never agreed with an idea you can force your morals of fairness on others. Life is unfair.

Say Amazon was to own UPS and was only charging itself at cost for all shipments. Too bad, so sad for rest of the online retailers. You are free to make your own delivery company if you want!

Or if in far future Walmart was to own a robotics corporation as seen in "I, Robot" and replaced over 2 million humans with a massive (at cost) robot workforce.

Hance destroys their competition with even lower prices. Too bad, so sad. I sure shop at Walmart while everyone else can be whining how unfair Walmart is.

Joshua Kennon

December 5, 2015

Replying to undercover

I'm in the car at the moment but you are misunderstanding the way and reason the government requires minimum pricing that goes back a long time in economics. It's not the sort of collusion or interference you are describing and has more to do with stopping a firm from extracting value from society. If, by the time I get back to the office this afternoon, someone sent written an explanation to you breaking down the details I promise I'll come back and leave a comment walking you through it. I think you'll understand why so many experts and smart people are really, really concerned by the allegations.

innerscorecard

December 5, 2015

Replying to Joshua Kennon

It's amazing that you typed that on your phone!

undercover

December 5, 2015

Replying to Joshua Kennon

Alright, I'm all ears for a more detailed explanation. Maybe I'm oblivious due to my core beliefs. However, what you two are saying about those tax laws sounds insane you are can taxed for money you didn't make... This whole thing hits me as thoroughly immoral.

The heart of the issue is because they're doing it at cost.

To use your point back at you. This is like the government walking into a retail store saying, "well, your prices are too cheap, we should be earning much more in government tax revenue."

Therefor we are taxing you for money we FEEL you should of made, even though you never made it and we are also forcing you to raise your prices for all future customers. We expect a check. You Belong to the government mob now. We set the lowest prices, you don't get to do that!

The craziest part is the SEC has given them an ownership structure exemption that even allowed this happen in the first place! Now people are saying they should of never been given the exemption and should be forced to charge more for what they offer and that they owe back taxes!

Ann thinks Vanguard is skirting the rules. My point is rules are madness. This is pure madness not knowing somewhere deep in the 10000+ papers of other government regulations vanguard breaking one about giving its customers at cost services services (The goverment right hand (SEC) does not know what the left hand (IRS) is doing.)

This whole taxation issue is creating the same feelings I get from this video:

https://www.youtube.com/watch?v=S6HEH23W_bM

LordSquidworth

December 5, 2015

Replying to undercover

That video is so asinine.

I feel like I need to dig out a text book to try and get the brain cells back I think just died watching that.

Ang

December 5, 2015

Replying to undercover

Except in this case, the "consumer" and the "shareholder" are one and the same. YOU are benefiting from tax evasion of the parent company while non-shareholder citizens in the US are left to make up for the tax bill that the government did not collect from Vanguard and its shareholders

joe pierson

December 5, 2015

Replying to undercover

"Stop government taxation of business/corporations profits.In other words, a 0 % rate is my answer"

Isn't that's a form of socialism (as in privatizing its profits and socializing its tax expeneses). I will have to pay the corporate tax bill the government did not collect. If a corporation cannot afford to pay taxes, maybe it shouldn't be in business at all.

Joshua Kennon

December 7, 2015

Replying to undercover

To keep my promise to walk you through this, I spent some time today at my desk, completely rewriting this post in a way that systematically took you through the specifics of the controversy, an explanation of the esoteric area of tax law known as "transfer pricing" and many of the reasons it matters so much.

To understand my points, please re-read the entire (now new) post and then return here. Then finish reading the rest of this comment.

-----------

I'm serious, if you haven't read the article, again, don't proceed.

-----------

Ready? Alright. Let's go.

Reading through the things you have posted, it seems like an underlying thesis, a sort of moral assumption from which you are operating, is that individual freedom to engage in commerce is sacrosanct. I would wholeheartedly agree with that. Unfortunately, you are viewing the issue through the lens of a specific person or business, in a specific pricing scenario, at a specific time and saying, "That's not fair." You are ignoring the system-wide consequences of that approach due to second and third order effects, the power of compounding, incentive-caused behavior, and a host of other relevant considerations.

You need to step back from the tree and look at the entire forest because once you see it in context, you'll realize that the alternative approach results in far more freedom, for far more people, on a net basis despite seeming counterintuitive. Think of it as the difference between a judge on a local jury trial, where justice is your concern, and a Justice on the Supreme Court, where system-wide consistency and efficiency is your concern.

You also need to understand how we, as a country, got here.

After generations of painful lessons, somewhere around 150 to 170 years ago, the United States, and, indeed, much of Western Civilization, began to realize that unrestrained, individual autonomy in commercial matters inevitably devolved into its own destruction; destruction that resulted in less individual autonomy in commercial matters in the long-run; Upton Sinclair writing about rats scurrying over meat at a processing plant and all of that. Whether it was power corrupting or heirs who had done nothing to deserve their position but win the genetic lottery inheriting the levers of influence and capital, those who had outsized success almost inevitably ended up getting so far out ahead of the race that the system broke down. Barriers were erected so it became impossible for new entrants - children born to non-rich parents, immigrants, those who lost everything and wanted to rebuild, new start-up firms - to have an opportunity to work hard and prosper. In doing so, it tore down any moral justification capitalism had to the alternatives because the entire premise of capitalism is that it does more efficiently, more fairly, and more often what an economic system is supposed to do: Allocate resources so the standard of living for the most people is raised in real terms over subsequent generations while unleashing the most human capital.

To solve this, compromises were reached. In exchange for offering certain benefits - e.g., the limited liability protections gifted to a corporation by society - restrictions were put in place that served as reset mechanisms so the overall system delivered more net opportunity for individual autonomy than an unrestrained, self-devolving system would.

Pricing is a major part of those compromises. You argue very passionately about the importance of the freedom of trade. However, the constitutional and legal system of the United States is set up - and, indeed, allowed only 5% of the world's population to capture 50% of the world's wealth - in no small part because it, instead, priorities preserving the freedom of trade and a semblance of fairness over any one, specific transaction or company.

Read that last paragraph one more time.

In other words, it will tell someone, "Too bad, this sucks for you but the system is more important" and allow a little economic restriction on a micro-level to permit more economic freedom on a macro-level. You are stomping your foot and saying, "But it's not fair ..." I know. It's not. You're right it's not. But it is necessary.

You accept this constitutional and legal framework because, as previously mentioned, in exchange, you are granted a myriad of benefits that make this one of the best places on the planet to engage in commerce. If you go bankrupt, you don't get hauled off to debtors' prison. In fact, your personal assets are likely protected due to the limited liability granted by everyone else in exchange for you playing by a few, basic rules. You have an educated workforce that is available to hire thanks to free K-12 education. You have infrastructure that allows you to bring in and ship out merchandise at far lower costs, effectively increasing your profits as you take advantage of economies of scale shared with all other citizens. The list goes on and on.

Here are examples of some of the handful of restrictions you accept on pricing when you conduct commerce in the United States; restrictions that, in some cases, have been in place since the 1800's and helped lead to the history-shattering prosperity of the 20th century as it equalized opportunity and conduct to a meaningful degree. These are not anything new. It is simply incorrect to state that you are immune from them or somehow they are immoral. They exist specifically because they lead to more moral outcomes for more people more often.

1. If you are a retailer, you cannot artificially raise the MSRP on your merchandise then offer a "sale". JCPenney is facing a lawsuit over it at the moment because it violates the FTC regulation requiring retailers to sell items "at original prices for 'a reasonable length of time' before adding discounts" (see link for source). This prevents people from having to worry about being defrauded in the moment, absent the ability to know if the sale is "real".

2. If you are a power, water, gas, or other comparable company, you can't set your own prices for the thing you produce. You spend billions of dollars to build these facilities, you risk staggering amounts hiring staff and equipping it with the necessary machinery, furniture, and technology to conduct operations, and you have to get approval before raising or lowering the price per unit. Why? It leads to far more systematic efficiency. The restraint put on the business leads to far greater outcomes and fairness for everybody else, which takes priority over your concerns. We, as a country, don't want to worry about a widget manufacturer being effectively blackmailed because you decide you're going to shut off his power right before a major shipment unless he pays you twice as much per KWh.

3. If you are a bank, lender, or payday loan company, you can't set your price at whatever you want. This restriction is so ingrained in human history - at the risk of making a logical fallacy known as an appeal to tradition - it goes back to some of the earliest written records we still have available to us! For example, in Kansas, you can't set your prices above 18% for the first $1,000 loaned and 14.45% for amounts over $1,000 loaned.

4. Under the Robinson-Patman Act, if you are selling commodities, you can't charge competing buyers different prices for the same product or discriminate in the provision of allowances [Source].

5. Manufacturers can force you to raise your prices if it believes you are selling too cheaply because it effectively means you are being a parasite to the rest of the dealer network, extracting value from the whole system as you benefit from their marketing dollars and investments. (See Leegin Creative Leather Products). The fact that you own the retail store, you paid for the merchandise; doesn't matter.

6. You can't set prices at different prices for different types of people that fall into certain types of groups (e.g., charge black customers less than white customers, men less than women, Christians less than Muslims). A restaurant owner was sued and lost as a result of offering a discount to anyone who brought in a Church bulletin on Sunday for this very reason. It was illegal pricing.

On and on we go. There is a legal doctrine in the United States known as the "rule of reason" that determines when restrictions on trade are constitutionally acceptable. Selling "at cost" because it benefits the user is not a moral or legal justification for breaking the rules. Microsoft was on schedule to be shattered like Standard Oil at one time because it gave away an Internet browser as a built-in software program on Windows, harming a competitor's (Netscape) business. The fact they were benefiting consumers didn't matter. The fact they were benefiting stockholders didn't matter. They were wrong.

One of the areas in which you do not have the authority to set your own prices involves transfer-pricing for taxation calculations of affiliated, controlled companies. That is the part we dove into in the now re-written article above this comment section.

You look at it and say, "This is so unfair for a single firm to have to raise its prices for the purpose of tax calculations", thinking only about Vanguard.

Do you know what the alternative is? Seriously, I want you to consider the systematic consequences of what you are saying. Stop and think about it for awhile.

I can tell you what I see.

Imagine me, in a room, with a pen and a calculator, where these rules are no longer in place.

Do you have any idea what kind of damage I could do?

Let's drop the pretense and social graces for a moment and be real with each other. Given enough time, I, and people like me, will own you, your children, and your children's children. We will be able to almost effortlessly restructure our lives to the point we pay nothing for all of these benefits that we share - the military, the infrastructure, the educated workforce, the bankruptcy protections - while you are left to pick up the cost. Your taxes will continue to climb as we miraculously pay less. Like parasites, we will eat your food, drink your drink, and let you pick up the tab. When you catch on, we'll use the accumulated advantage we already have to rewrite the rules underneath you so you never make progress. More and more power and wealth accumulates in our hands not because we are better people, not because we work harder, not because our products or services are better, but because we simply have a higher type of a specific intelligence that happens to benefit disproportionately under such a system and managed to climb the ladder first before pulling it up behind us. Within 100 years, you will have reintroduced a landed aristocracy and, in your quest for a single bit of economic freedom in a single transaction, slit your great grandchildrens' economic throat as they are now all but enslaved in name only to my great grandchildren.

It is as arbitrary and hateful as creating a system where all of the rewards go to someone based on their height, their race, or a random lottery. It is immoral. It is also profoundly stupid. Capitalism, when properly regulated and coupled with certain minimum safety nets, provides exponentially higher standards of wealth than socialism and communism because it does not view man as an angel, but rather exploits his weaknesses and self-interest in service to others. Unrestrained capitalism enslaves us to the equivalent of economic warlords and the government. Stop looking at the transaction in front of you and start looking at the systematic and long-term consequences; the second and third order effects. Saying a person has an unrestricted right to set their own prices is not intelligent if you have any sense of self-interest at all. You might as well take a sledgehammer to the free market because individual people, acting in their own best self-interest, will do it in time if those reset mechanisms and restraints aren't in place. Nobody - seriously no respectable economist in the world advocates for the kind of laissez-faire capitalism you are proposing because it doesn't work in the real world. It's a 14-year-old's fantasy; something believed before experiencing life as it is, not how you think it is. It would be madness to unleash it as it would destroy the prosperity that has been won over the past century and a half. It is as crazy as a Marxist believing in government owned asset efficiency or optimality or a socialist thinking shared ownership of productive means can lead to superior outcomes, ignoring well-documented mental models with applicability to behavioral economics such as the tragedy of the commons.

Let me give you a quick example to make this tangible. If I could ignore the transfer-pricing rules like Vanguard, what would stop me from ... I don't know ... bringing my sporting goods business and my parents' sporting goods manufacturer under a parent company with an internal, family-only merger? Then moving the manufacturing plant to a low or no-tax country? Then buying all of our products we sell in the United States through that controlled manufacturing subsidiary but charging prices that result in $0 in annual profit. (Hey, we operate at cost! Look at how wonderful we are. I'll only hire relatives, give them an equity stake, then continually trumpet this from the sky.) Then, after that was done, how about I turn around and set up my own captive insurance company in the Bahamas; write a policy on the manufacturing business so I left it with no earnings, either? Done right, I could go through my entire life without paying hardly any taxes, enjoy tax-deferred compounding on our past earnings even if you worked far more hours and contributed far more to your fellow man. How long would it take me to drive down prices so that I controlled an insurmountable percentage of the niche part of the sporting goods industry where we operate? Me and my family would be getting rich by cheating the system, our competitors would lose the ability to make as good a living because we were able to use our artificially low cost basis to drag down the industry economics, and you, meanwhile, are paying our tab because the shared costs of running the nation still have to be covered. I can prance around all day crowing about my "at cost" manufacturing business and how it benefits the family-owners but I'm doing extraordinary damage that harms my community, my country, my competitors, and you, my fellow citizen. I'm cheating. It's disgusting behavior.

It's more than a little ironic that this conduct is in direct violation of one of Bogle's written values, which comes from Immanuel Kant's "categorical imperative that we must 'act so that the consequences of our actions can be generalized without self-contradition'". This behavior does not meet the test.

Do you really think hard work is going to let you get ahead under these circumstances? We now make the rules and you are at our mercy all because you were more interested in preserving competition for a single transaction rather than preserving the on-going competitiveness of the system as a whole.

This phenomenon plays out elsewhere in our system and you need to be aware of it.

The "sometimes we get more system-wide freedom by permitting individual injustice" philosophy is the reason the military ruins the career of a ship captain if he retires for the night and the subordinate wrecks the ship. It makes the leader more vigilant about handing off authority so the most qualified person is in charge when it is most important.

The "sometimes we get more system-wide freedom by permitting individual injustice" happens when a judge throws out evidence against a murderer, rapist, or other criminal because it was achieved in a way that threatens constitutional rights. Stopping the government from prospering from even the "fruit of a poisonous tree" is more important letting a bad person go free and potentially harming someone else.

This "sometimes we get more system-wide freedom by permitting individual injustice" happens when we ban a person who has travelled to an area with malaria from giving blood. The same for organ sales; they are forbidden due to the incentives they would cause even if both parties agree to it.

This "sometimes we get more system-wide freedom by permitting individual injustice" happens in the workers compensation system. We remove the rights of individuals to sue for unlimited damages even if the employer is wrong because the increased stability, predictability, and liability caps make the broader economy function better for everybody.

This "sometimes we get more system-wide freedom by permitting individual injustice" happens in the automobile market when we require everyone to have liability coverage even if they don't need it. Bill Gates doesn't need car insurance. He could hit someone, get sued for $500,000 in medical bills, and pick it up like spare change without even knowing it had gone missing. Yet, if he's pulled over and doesn't have it, he's getting a ticket. If he wants to drive, he has to meet the standards set to ensure system-wide stability.

This "sometimes we get more system-wide freedom by permitting individual injustice" happens when we force property and casualty insurance companies to underwrite high risk drivers who cannot otherwise afford insurance at artificially low rates with the loss-generating policies allocated under a lottery system by the state insurance regulator. It sucks for the owner of the insurance company who is forced to charge a rate they don't want to charge to a customer they don't want to serve but it makes sure you don't have some driver hit an innocent person and then be unable to pay the medical bills due to a lack of coverage.

This "sometimes we get more system-wide freedom by permitting individual injustice" happens in retail pricing agreements with manufacturers. The Supreme Court upheld the right of manufacturers to force retailers to charge higher prices to protect their brand and stop the parasitic distributors or sellers from riding on the coattails of the rest of the retail network.

In other words, this idea that pricing is determined solely by the business owner has no basis of fact in the constitutional or legal history of the United States. It's bonkers; a fantasy. Individual pricing power is subject to regulators, legislatures, and courts determining that it doesn't interfere with the maintenance of a system that continues to provide individual pricing power. Business are told to charge higher, or lower, prices every day. Businesses are forced to serve customers they don't want to serve to ensure greater overall system efficiency.

TL;DR: You know that television show Supernatural? The episode where Dean is given Death's power and is responsible for overseeing the harvest of souls for the day (Season 6, Episode 11)? He gets the bright idea that individual justice is more important than systematic justice, saving a little girl. In the process, the non-intended consequences of modifying the system created far more injustice in the form of many additional deaths that could have been avoided. Seeing the destruction he's unleashed by focusing on a single event rather than the system-wide consequences of his actions causes him to lament his folly. His ideals, while good, led to outcomes that were in direct violation of his ideals because we wasn't paying attention to how the variables interacted. Wiser, he realized that the system must be fair prior to the individual getting a fair shake or more individuals would get screwed. There is a parallel to this situation.

P.S. It's 2:54 a.m. Please forgive any typos. I'm not going to edit this as I want to get into bed now.

undercover

December 7, 2015

Replying to Joshua Kennon

nvm

Scott McCarthy

December 7, 2015

Replying to Joshua Kennon

It's funny you cite that Act in the context of this conversation, as there are only two exceptions to that general rule in that Act, and one of those exceptions is that you're always allowed to charge lower prices to a co-op or mutual company.

Joshua Kennon

December 7, 2015

Replying to Scott McCarthy

I thought about that and ended up touching on it in the other comment I just left to this same person, including a link to the page on the FTC site, further down the comment thread. I started to get into the reasons that exception exists but at this point, this post (with the responses) are turning into a novella and I have an actual job I need to do. I haven't accomplished much today so I'll probably be at my desk late.

What I don't understand about this whole thing: It's so easy to fix. Why not just fix it?

When I was much younger and interning at NJM, a mutually owned insurance company, they had the same dedication to their policyholder/owners as Vanguard goes to its investor/owners. The difference: They followed the tax rules correctly (interestingly, there were actually, technically, organized as a joint stock corporation not a mutually owned firm, which created all sorts of legal complications I loved studying because I'd never seen anything like it at that point in my life). They collected the income, priced their policies in accordance with the required regulations (though I understand the reasons now, I remember almost revolting when I realized that very high risk drivers were assigned to a special risk pool that they had to underwrite policies for on a basis, and at a price, that they knew would lose money, but which was modeled into their overall profitability picture as it served both the citizens of New Jersey and the company itself, which was granted the license to operate there), then paid those dividends out in a big annual announcement that was trumpeted from the rooftops. They took pride in it. They haven't missed a dividend since 1918 and have, so far, returned $5.8 billion in profits to their policyholder/owners, effectively lowering their costs.

Vanguard could be the same way. Sure, it would require a change in mindset to see the higher expense ratios but they could turn around and couple it with an investor/owner dividend each year. You could almost copy the mutual insurance exemption rules and slap it on the new 501(c)30 section.

I'm convinced the opposition at the firm is because it takes away an enormous marketing advantage they've used to take business from competitors, which allows the executives (I'm speculating here, they don't have disclosure requirements) to have become very, very rich. The irony is that even if it results in lower net savings, actually seeing a Vanguard dividend check each year could radically increase the "stickiness" of their already sticky assets. People who wanted to move to another firm would hate not getting the check. (The turnover in policyholders at NJM was just fantastically low; nobody wanted to leave, in part, I suspect, due to those dividends that were auto applied to premium renewals. Truth be told, if I had stayed in New Jersey, I'd have given them all of my business - car, home, commercial. They were just better than everyone else and seeing the big "paid" line for your dividends covering part of your policy costs would have been too intoxicating. I'd choose them over GEICO any day despite owning Berkshire Hathaway.) In fact, NJM made such a believer out of me that I opted for a mutual insurance company for my own needs; two of them, in fact. The customer service is better and the costs are lower.

I'm not particularly optimistic on reform at the moment. We live in a country where Comcast can't even have its oppressive monopoly taken away, for heaven's sake. It's terrible for society, terrible for commerce. Teddy Roosevelt would have taken a 2x4 to the place but we just keep letting it do what it wants, buying off politicians. What are the odds they actually do this? It'd be so simple.

dave (nestle)

December 5, 2015

(every time I turn around, with these companies' crap...)

I reckon it's time for everyone to immediately close their margin accounts at Vanguard. (haha)

Bob

December 5, 2015

I think I misunderstood. I though this was about predatory pricing.

I wonder though, how can there be a transfer pricing issue when Vanguard doesn't make any profits? I thought companies exploited transfer pricing to report profits in countries with low tax rates and minimized profits in countries with high tax rates. But if Vanguard doesn't make any profit, there can't be any tax evasion issues right?

Trey Henninger

December 5, 2015

Replying to Bob

The transfer pricing issue is that due to the way they have structured their transfer pricing they are showing no profits, when in fact they have made billions of dollars in profits. Those profits however were not reported because they were "reduced to zero" by having a low expense ratio.

The difference is highlighted in Joshua's statement on how it would operate in a new system. Because Vanguard's investors are also Vanguard's owners, the savings that they have made so far through lower expense ratios were essentially an un-taxed dividend payment.

Vanguard is selling a service and creating value of approximately 0.80% expense ratio but only charging 0.20%. That would mean that under the current system they have a profit equal to the 0.60% but instead of realizing that profit and paying a dividend to their owners (after paying taxes) they are reducing their costs to a point of showing no profit at all.

That's against the law. It's tax evasion.

The entire topic of whether or not that law is a moral or just law isn't relevant to the fact that as currently written, it's against the law.

billyjoerob

December 6, 2015

Replying to Trey Henninger

Is it tax evasion? Investment expenses are deducted from capital gains. So the taxes on those savings are paid when the investor pays cap gains taxes. And wouldn't this same argument (that Vanguard is evading taxes) apply to any firm underpricing rivals in order to gain market share?

Joshua Kennon

December 6, 2015

Replying to billyjoerob

Yes. The taxes should have been paid as corporate income tax. Passing it on to investors in the way the allegations state means that:

1. A lot will never be taxed as a big percentage of Vanguard's assets are held in tax shelters such as Roth IRAs and other qualified retirement accounts/plans

2. A lot will never be paid as wealthier investors who own shares outright in taxable accounts can use things like the stepped up basis loophole to have the tax forgiven.

3. In the meantime, the investors get the use of an illicitly funded deferred tax liability, which serves as leverage for taxable accounts and can result in significantly more long-term wealth when you get into holding periods of a decade or more.

The net consequences to the IRS, and thus taxpayers, would be tens of billions of dollars in effective fraud. It would be like you deciding you somehow didn't want to pay this year's tax so you broke the rules to hide it saying it's okay because you might, someday, somehow owe it at a fraction of the tax rate, on a fraction of the assets, many, many years in the future as you currently enjoy money that shouldn't be in your hands.

Trey Henninger

December 6, 2015

Replying to Joshua Kennon

Yeah, to phrase it in a different manner, it would be tax evasion even if none of Vanguard's assets were held in tax shelters, simply due to the *delay* in the tax liability. Even if all of Vanguard's assets were held in taxable accounts AND the stepped-up basis loophole didn't exist, it would be evading taxes by allowing the fund shareholders to only pay taxes in the future instead of pay them when they were realized within the corporation.

DanDarc

December 7, 2015

Replying to Joshua Kennon

I think the dollars in play here are inflated a lot. Like 10X or more a lot.

Why? They're using the average ER for all mutual funds in that report (which was paid for by a party that has a ton to gain). That's how they come up with the 0.7% number. If I'm Vanguard, all I say is "let's compare our S&P 500 fund to a comparable S&P 500 fund." Fidelity is charging .07%, you really think .05% is too low? What about Schwab's .04% ETF? Much argument ensues, net is something like "ok, we charged .01% too low on that one". Next fund. Repeat 150 times.

Rather than under-charging by 50+ basis points, I'm betting the actual is under 5.

Then Fidelity and Schwab, and any other big players that have both a brokerage and their own fund get to play this game too.

Joshua Kennon

December 7, 2015

Replying to DanDarc

If - and again, this is a big if because Vanguard hasn't been shown to actually have done anything wrong officially in a court or by a regulatory action as this is all based on the tax attorney's internal whistleblower claims as well as the tax experts the media asked confirming it looks legitimate that there is a problem happening - I'd suspect that wouldn't work for two reasons. Let's look at Schwab, specifically, since I happened to be going through their financials the other day:

1. Schwab generates a lot of revenue and taxable profit. Like a car dealership offering a cash rebate or low promotional financing, it can subsidize its index ETF products so they appear rock-bottom cheap knowing they will make more money in the long-run on the clients who tend to be attracted to them. That is, even though it offers a sale on a handful of products, its overall pricing strategy still passes the test the same way Wal-Mart can have a Black Friday loss leader sale and sell a limited amount of electronic televisions for non-sustainable prices.

2. Schwab has quietly transformed itself into a money float machine in the past few years to the point that when and if interest rates return to a normalized environment, the bottom line will explode as the surplus income it now collects holding its investors money falls to the bottom line, over the cost basis that is already covered by existing operations. It's somewhat akin to an insurance company being allowed to underwrite a policy at a loss due to the ability to make up the loss and gain a taxable profit on the investment income as the cash is put to work in corporate bonds. They can point the assets they're holding, and the agreement terms they've modified, and say, "See? Look at all this profit and tax revenue that will come in at some point".

Vanguard, at present, does not appear to have any of these business models in place. Thus, the same product or service, at the same cost, would be inappropriate and non-justifiable because it couldn't be sustained if they were paying taxes like Schwab is. They could adapt Schwab's approach, of course, but Schwab also generates a lot of money from its brokerage and third-party custody activities for registered investment advisors, which are leagues ahead of Vanguard's. It'd have to change how it does business.

Still ... let's assume you're right. You're still only talking about the index products. Vanguard is one of the biggest active money managers in the world. Somewhere around $1 trillion in assets under its management is actively managed despite it having a reputation as an index fund shop (it's one of those things were reality and perception don't match up). Even if the cost was permitted to remain low on a handful of the index products, including the largest with which it is most associated, it wouldn't do much good for the trillion plus dollars in other shareholder assets they are running.

If they are guilty, here is what I would like to see happen (assuming the IRS decides to play nice): Vanguard should get Congress to draft a new extension to the 501(c) section of the non-profit laws, adding a new, 30th provision (the 501(c)30) that covered asset management. It would then treat Vanguard akin to a mutually owned insurance company (think State Farm, where the policyholders are also the owners). Vanguard would charge its funds market-based operating expenses, pay taxes and all of that ... only, once a year, it would declare a huge dividend on the surplus earnings it wanted to return to its investors/owners either in the form of cash or additional shares of the funds in which they are invested. The expense ratios might increase for the fundholders but they're also going to get a not-insignificant portion of it back with the other hand and now the whole thing is moral and ethical. It solves everything. Competitors can't complain about them cheating. Vanguard owners pay more but they still are getting a much better deal than they could almost anywhere else. Everything is on the up and up, no problems.

Back in college, I interned at a multi-billion dollar mutually owned insurance underwriter in New Jersey (NJM Group) and they were as devoted to their policyholder/owners as Vanguard is to its investor/owners. When they declared policyholder dividends, returning money from their profitable operations to the customers, they took so much pride in it, it made you feel good; like you were truly serving society. There's no reason Vanguard couldn't evolve into that sort of structure. The United States has a long history of it working in the insurance industry, it can work in the asset management industry, too. Just as NJM bragged about the billions of dollars it had returned to its policyholder/owners since the early 1900's, so, too, could Vanguard point to a figure and say, "Look how much cash we've returned to our investors!". It might even encourage more success ... who'd want to switch to a competitor if you got used to going to the mailbox and finding a check from Vanguard written out to you for your cut of the firm's profits that year? The roadmap is there. It can be done.

DanDarc