Nestlé Dividend Day 2016

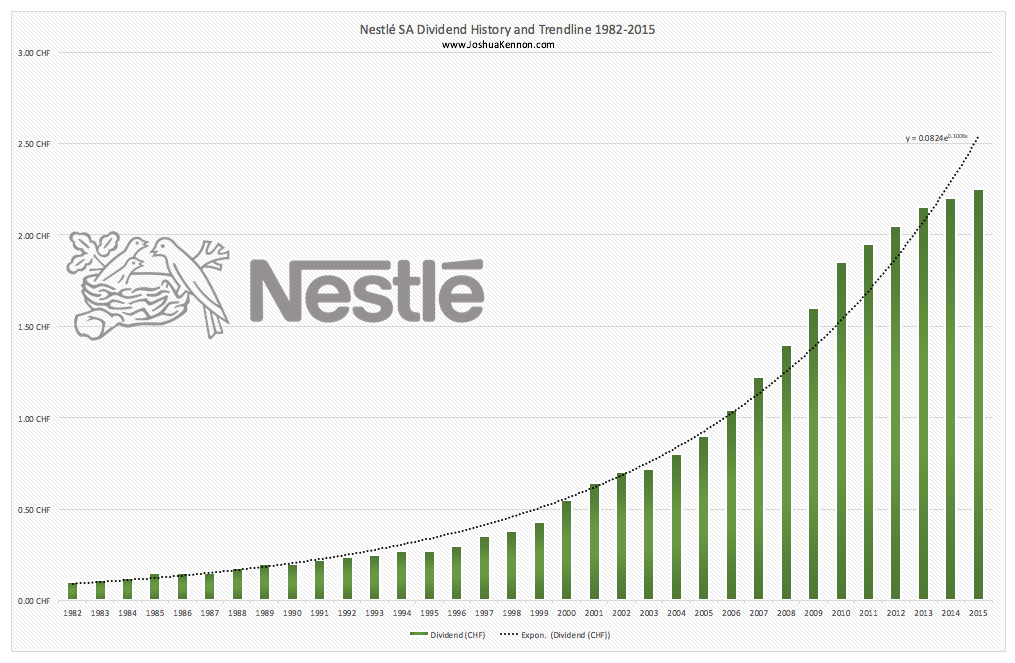

Whether you own the shares directly in Switzerland and collect Swiss Francs or indirectly through the American Depository Receipts and collect U.S. dollars, the once-a-year dividend has now been paid by Nestlé to its shareholders with both dates having now past (or, in the case of the latter, arrived). For fiscal year 2015, the board continued its long tradition of dividend hikes and increased the per share rate to 2.25 CHF, up from 2.20 CHF the year prior, representing an increase of 2.27%; a shining achievement for a company so large in a nation where the central bank has imposed negative interest rates on commercial banks and for a business that, last year, was considered such a safe haven that its bonds actually were selling at negative yields as investors flocked to them, which I mentioned in passing on the post about the folly of investing in 50 to 100 year bonds, considering them a better alternative than cash. (Remember, you have to measure nominal changes in currency relative to inflation. Purchasing power is what counts.)

For American holders of the Nestlé ADR who deal with the currency translation complexities, it looks as if the post-translation dividend worked out to $2.3198 per share, out of which you then had to pay a $0.025 per share currency translation and administration fee to Citibank and a $0.348 dividend withholding tax to the Swiss Government (assuming you did your job and made sure your broker filed the correct paperwork entitling you to the benefits of the U.S.-Swiss tax treaty so the 35% rate wasn’t withheld. Every year, I get messages from a handful of people asking why their dividend taxes were more than double what they should have paid. Unless you’re planning on flying to Switzerland to reclaim the funds, make sure to take care of these details).

For the decade ended, the dividend increased from 1.04 CHF to 2.25 CHF, representing a 116.3% increase on a per share basis over the initial dividend and assuming no dividend reinvestment on the part of the owner. That approximates a compound annual growth rate in the dividend of 8% per annum through one of the worst economic decades in generations, inclusive of the near total collapse of the global economy between 2008 and 2009. Just as beautifully, during this same decade, Nestlé substantially shrunk its overall shares outstanding while maintaining its sterling balance sheet. Look at the period right before the world fell off a cliff in 2008. The total shares outstanding were roughly 3,615,600,000. Today, that figure is around 3,085,000,000. Despite those rising dividend payments, each share now represents an additional 14.7% ownership in the firm compared to what it did in the year President Obama was elected to office. That prudent use of capital should continue paying off for long-term owners for decades, even generations, in the future.

With the newest data points, this means I can update my long-term Nestlé records. To give you an idea of how it has done since I’ve been alive, if you bought shares around the time I was born back in the early 1980s, you would have collected 0.10 CHF shortly thereafter (I was born in the latter part of the year so you wouldn’t have had to wait much to get that initial, base payout and it therefore doesn’t represent a compounding period). Following the dividend increases over the subsequent 33 years that came after that base rate, your dividend would have grown to the present 2.25 CHF, representing a 2,150% increase over the base rate on a per share basis, assuming no dividend reinvestment on the part of the owner. That approximates a compound annual growth rate in the dividend of 9.9% per annum. This was achieved over a period of war and peace, inflation and deflation, and stock market booms and busts.

It is the fascinating mathematical paradox we discussed in an older post I wrote about Nestlé … that it never looked like the best investment to buy in any particular year but it almost always ended up being one of the best investments you could buy over long periods of time. It has been a money printing machine. It doesn’t even make the radar of a lot of people due to the fact it is traded in Zurich. Those who do notice it often by-pass it because it looks so boring on paper; a quintessential “get rich slowly” stock. It remains the sort of asset that only predominately wealthy families, pension funds, and highly passive international blue chip funds buy and hold. Yet, decade after decade, prices were increased with inflation, competitors were acquired, share count was reduced, dividends per share were increased and owners were showered in piles of money. When new businesses were acquired, the aforementioned sterling balance sheet allowed the firm to lower the overall cost of capital, its purchasing power allowed it to achieve economies of scales that could hardly be matched, and its deep bench of managerial talent allowed it to spread best practices among subsidiaries.

It is proof, yet again, of a saying from global wealth management: “When the going gets tough, the tough buy Nestlé.” It is almost impossible for a member of Western Civilization to go a meaningful length of time without somehow, directly or indirectly, putting money in Nestlé’s pocket. From baby food to frozen pizza, tea to coffee, pasta to confectionery treats, chocolate to cereal, the often overlooked global blue chip has a diversified stream of earnings that allow it survive under nearly any economic or reasonably probable political conditions. Were you to shatter it, many of the subsidiaries in and of themselves would instantly be among the world’s largest food and beverage companies.

One of the new focuses for the business going forward is food-and-beverage-as-a-delivery-mechanism-for-pharmaceuticals. It will take years, if not decades, to materialize but according to The Wall Street Journal‘s story on April 12, 2016, the Swiss titan has been working on prescription medications that will be tailored to the genetic profile of customers. This is thanks to a research and development program internally that was given $500 million to develop medical foods for people with chronic diseases such as Alzheimer’s, epilepsy, and intestinal disorders. Imagine the profitability if they can do things like develop food that gives folks with Crohn’s Disease relief from their symptoms. They’re striking strategic deals with pharmaceutical companies to develop “amino acid-based products to treat muscle loss”. It’s in anticipation of an aging global population; to go where the money is and create products people don’t even realize they need or demand, yet.

Part of my love for Nestlé is what it reveals about human nature. If you’re a typical American shareholder, you probably own the ADR. You can’t trade options on it. You can’t borrow against it on margin. You have to pay cash for it, in full, and then receive a single, annual dividend payout like you might at a private family business. The stock price sometimes goes sideways for years as people neglect it and the intrinsic value grows internally along with the payouts. Its accounting is conservative. Its returns on capital are far higher than they appear at first glance if you’re just doing quick calculations imported from a finance portal. If you’re 20 or 30 years old, and have a reasonable chance at a 50+ year run in front of you, I’d argue that any halfway intelligent person would consider buying some from time to time, locking it away, and almost never selling it; holding it no as a sort of economic oak tree meant to be left for old age or future generations. Present known factors considered, the numbers seem to indicate that it offers a high probability of satisfactory returns over the next 25 years.

Reader Comments (33)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

fran

May 21, 2016

Dandelions versus oak trees. I really like that analogy.

Dividends are Coming

May 21, 2016

In my case Swiss dividends get taxed at a massive 52.55 percent so that plays a big role in why there always seems to be something better to put my money in than Swiss shares like Nestlé.

In the US it's easy to get the 15 percent treaty rate but unfortunately, here in Belgium (and other European countries too I think) it's a lot more complicated. I first get taxed at the 35 percent rate and because the Belgium government doesn't care that these dividends were already taxed by the Swiss they take out another 27 percent of what's left.

In theory, it is possible to reclaim the 20% excess withholding tax from the Swiss but my broker charges 100EUR for this so for small-sized holdings it's not really worth it.

ffc

May 23, 2016

Replying to Dividends are Coming

I'm in another EU country with the same problem. The following will not work for NESN, but if you are interested in US-based dividend shares, you should take a look into optionsxpress.com. Since Belgium and US have a double-taxation avoidance treaty, after sending the relevant form to optionsxpress, you will only be charged the higher of the two rates (27% in the case of Belgium I presume) in total. Of course, you will have to convince the local tax authority that you have paid the 15% to the US IRS via optionsxpress, but this should be doable.

Dividends are Coming

May 23, 2016

Replying to ffc

As far as I know it's not possible in the case of Belgium. There's been some jurisprudence about this and previous governments promised to abolish it but nothing ever changes. The double-tax treaties limit the foreign withholding tax to a maximum of 15 percent. In case of the US, we fill in a W8-BEN form and the 15 percent rate gets applied automatically but after that we still get double taxed with no legal way to avoid it.

The process for getting the 15 percent rate for US equities is actually a lot easier than getting the treaty rate for dividends declared by companies in European countries. As a small investor, it's often not worth the time or cost to recuperate the difference between the applied tax rate and the treaty rate.

In terms of investing, about the only good thing about Belgium is that we don't have a capital gains tax, but I'm afraid that may change as government is always hungry for more taxes. Government recently introduced a ridiculous "speculation tax" and we also have a really weird tax on spin-offs. By default, Belgian tax authorities treat spinoffs the same way as dividends, we get taxed 27% on the value of spin-off shares. Belgian companies can avoid this by cooperating with the Belgian authorities to avoid the tax but for foreign companies it means Belgian holders have the sell the shares before the spin-off date to avoid the tax.

Andrea

May 23, 2016

Replying to Dividends are Coming

Same here in Italy,

we got 35% from Switzerland + 26% here in Italy.

We can request to get back 20% but here Italian banks charge around 150 EUR so it's even worse.

There is no way around it as far as I know, or you can have a big position that 150/100 EUR is a little portion of your dividend income or it's better to stay away from Swiss stocks who pay dividends.

Jeff

May 21, 2016

Got my first Nestlé dividend yesterday! I picked some up during the dip in January.

My numbers (dividend, tax, fees) from Merrill Lynch match yours exactly.

Jeff

May 21, 2016

I miss the recent comments section of the blog! I let me see old discussions that were still ongoing. Hopefully the forum arrives soon.

Gilvus

May 21, 2016

Replying to Jeff

The forum has been up for a while, but no one has posted. Moderating a forum is a time-consuming (and sometimes stressful) job which would distract Josh & Aaron from the blog, their businesses, and their families. Compounding the problem are spambots: last I checked, a lot of registered users seem to have advertisements in their profiles. I'd say the chance of the forum launching is slim, and I'm okay with that if it means Joshua continues to produce higher-quality work in everything else that he does.

I also miss the recent comments section, but it was an eyesore. With the blog being reformatted to serve as an extension of Kennon-Green & Co., the most recent five comments would look like spray-paint graffiti on a mahogany-paneled storefront. Once Josh and Aaron have more free time to devote to the blog, it would be nice to have a tasteful replacement, though. Like an "recently discussed" sidebar that shows which page was commented by which author, but not actually showing the comment itself.

Joshua Kennon

May 21, 2016

Replying to Gilvus

Coffee break time! I've been working all morning and need a few minutes to reset. (To paint the scene, I'm in full-blown old man mode at the moment. I'm sitting in front of a space heater enjoying a Wurther's original butterscotch with a cup of black coffee. All that is missing is a Mr. Roger's sweater.)

The forum that is hidden on the site (if you can call it that - it's easy to find) is a test installation that may not exist shortly. I'm looking into cloud-based solutions. Even if we stay with a server-hosted version, I might isolate it on a different installation from the blog for the sake of redundancy. That's the reason I don't advertise it or let people post there. It was basically my way of messing around with the administrative tools to decide whether or not I wanted that particular forum platform.

The rebranding is a bit more complex. The purpose is not to cause this blog to become an extension of Kennon-Green & Co. when it is established, but rather, separate it in a meaningful way as we severely curtail our online presence. The goal is to have all of the pages end up with no sidebar so you can focus exclusively on the content, substantially reduce the number of advertisements, release podcasts or videos, focus on the more personal stuff (and, as it pertains to investing, the more academic and philosophical part of it somewhat akin to my About site as the other stuff will most likely be released through white papers at KG&C), implement a forum, etc. Concurrently, I'll release a set of guidelines about what I won't do. For example, I won't have a conversation with a client about anything to do with the firm in the comment sections. Their comment will either remain ignored or get deleted. (Not that I anticipate this happening as clients will have a direct email and phone number to reach both me and Aaron.)

As part of the advertising reduction, one thing I am going to do after being asked repeatedly over the past few years is look into accepting direct ad sales so the (fewer) ads that are displayed are a more organic fit with this audience with some fairly tight style guidelines. Kennon-Green & Co. will get free advertising as a perk of me doing all of the work and owning both so they will be visible in the same way Vanguard ads, Schwab ads, Merrill Lynch ads, etc. have been in the past (and will still be in many areas, I expect).

The problem with all of this is that, in the midst of getting Kennon-Green & Co. launched, my Investing for Beginners site is undergoing a massive project I can't really talk about in any detail and they need me to help update my old content, which I wanted to do, anyway. That means that my 18 hour days are now more like non-stop marathons as I have to get most of this done in the next 60 to 90 days.

Yesterday, we spent almost all day getting the Credo finalized (it's heavily, heavily influenced by General Johnson's work at Johnson & Johnson since, as far as ethics and philosophy go, I consider it a masterpiece worthy of emulation), writing out the service description for private accounts, and getting the final formatting decisions made on the Kennon-Green & Co. site. What will likely happen is that after we've sent out the confirmation emails to the waiting list, once we are open for business, we will send login credentials to the waiting list members who will be able to get into the site before the general public.

The thing that's been on my mind the past few days is coming up with a specialty type of private account for the - I'd guess maybe 3% or so? - of people who have written or called asking if I'd consider doing some sort of extreme passive portfolio allocation for them; something on par with a ghost ship or at least a low-cost ETF. These are folks who fall more toward the Boglehead side of the spectrum, who are largely do-it-yourself but either want to outsource it so they can focus on their career or want someone to step in and stand watch after they pass away so their non-financially interested spouse doesn't have to worry. The pricing is the trick and it almost has to be negotiated on a case-by-case basis with the specifics of the mandate and service requirements. If someone shows up and says, "I want you to build me an equal-weight portfolio of 100 businesses you believe are extremely high quality, pool the dividends with new deposits I send in throughout the year, and rebalance once per annum", I'm going to charge more than if they show up and say, "Hey, I have $10 million and want something like what John Bogle tried to get Vanguard to offer years ago - just give me, I don't know, something like the largest 50 or 100 stocks by market capitalization, ignore the float-weight adjustments the S&P pushed through in recent years and equal-weight them from the start, and let a natural weight develop over time". Some of them, for whatever reason, might still demand I use only low-cost index funds, ETFs, and/or mutual funds rather than acquire the underlying individual securities, in which case, it would take even less time. (Time is a major consideration here. Passive strategies are a lot less work on both of us than the private accounts run on a global value, high dividend, or balanced defensive strategy, which is how a vast majority of our and our family's personal liquid net worth is invested.)

Most of the time, I'm open to considering it - most low-cost firms that focus on this sort of thing charge between 0.30% and 1.00% on the advisory side plus there is the "look-through" cost of the index funds, ETFs, etc. themselves which, at most firms on average tends to add about 0.19% if I recall correctly (really, really rough estimate). But, again, it's all so specific. Going back to the $10 million example if someone wanted that Bogle-like direct portfolio of equities, if I really thought they were in it for the long-haul (10+ years), I trusted them to stick to the passive mandate, and I knew they understood what they were asking, I'd probably agree to manage it for a fee that ended up weighting out somewhere between 0.25% and 0.50% per annum because I'll have the institutional tools at my disposal to do it efficiently and (almost assuredly) for much lower costs than they could, especially if I can batch several clients together on the rebalance date for the individual components, they get the benefits of individual securities including a much better chance of taking advantage of tax lot harvesting, and it's a lot less work on us. If they insisted, as at least a couple people have, that they want a portfolio of low-cost index funds, ETFs, etc. for them, rather than build something it from the ground up out of individual equities and fixed income securities, the weighted fee might even be lower than that, toward the bottom end of that range.

In any event, it's finally starting to come together. Things are getting finished in different areas and the building blocks are getting arranged so we're seeing the Firm emerge before our eyes.

I hear Aaron. He was working on something and it sounds like he's done. I should probably go grab him while he is free and have him finish approving a pricing structure I am going to use on the private account page. Break time over. Thanks for the distraction.

Gilvus

May 28, 2016

Replying to Joshua Kennon

Ah, I see. My apologies for misinterpreting your intentions. I figured the forum was something you simply don't have the time to deal with yet, seeing as how the majority of the 1200+ registered users are spambots. Even if they weren't, you'd have to moderate the Disqus on your blog and the forum. I wouldn't envy your workload.

I misspoke (mistyped?) earlier - I should've said that the blog was being reformatted to serve as an extension of the Kennon-Green brand, not of the Firm itself. Your previous blog format certainly wasn't inelegant, but the current design is decidedly more...genteel. Closer in spirit and style with the Firm. It makes sense, because as you mentioned this blog will carry KG&Co's ads and direct traffic toward the latter. So despite the bright line in the sand between the Firm's content and the Blog's content, both meaningfully contribute to Kennon-Green brand equity.

Glad to see that the Firm is crystallizing out of the aether 🙂

Joshua Kennon

May 28, 2016

Replying to Gilvus

No worries. You were right in a major way, too, which I should have made more clear. Moderation has been a concern of ours; a huge roadblock I don't want to tackle. Both Aaron and I figured if we ever get around to it, I'd have to bring in community moderators. There's no way that's a job either of us could stay on top of with my other responsibilities. It would have grown beyond us and need to be turned over to a handful of those of you who have been around for awhile and whom we trust to keep the spirit of the place the same. As you said, even Disqus is a problem now. I can't keep track of it all. I miss a good percentage of comments that come through and it's as much luck as anything else as to which ones I see; what happens to be on the screen when I open the admin panel. I'll go back and read old posts and realize I missed half of the subsequent comments that were left, responding years later.

And this ..."I should've said that the blog was being reformatted to serve as an extension of the Kennon-Green brand, not of the Firm itself. Your previous blog format certainly wasn't inelegant, but the current design is decidedly more...genteel. Closer in spirit and style with the Firm. It makes sense, because as you mentioned this blog will carry KG&Co's ads and direct traffic toward the latter. So despite the bright line in the sand between the Firm's content and the Blog's content, both meaningfully contribute to Kennon-Green brand equity." ... is exactly right. I want to pull the past 15 years of work into a cohesive vision, applying quality control to it. I think we're probably only a few months away from a second "Great Purge", if I'm being realistic with myself. I spent some time tonight taking down old posts as it would be too much work to bring them up to date or clean them up. I will figure out how to scale, dang it. I don't care if the site ends up consisting of a single page on a teak wood texture with cafe music in the background and a wall of high definition videos where we sit and talk rather than write. Tricky thing, getting it solved but we'll do it.

(Forgive the disjointed nature of this comment, it's another one of those late night messages. I'm so tired but I'm not done, yet, so I can't let myself go to bed. Our nephew called asking if he could come over today so we ended up going and buying Super Mario Maker for Wii U and building Mario worlds with him for most of the afternoon along with riding a scooter through the neighborhood. It was worth it - they'll only be young once and these types of days are the time when lifetime memories are solidified so it was definitely the best investment of my time - but I have a schedule to maintain so sleep will be sacrificed tonight.)

Gilvus

May 28, 2016

Replying to Joshua Kennon

Great Purge 2 (Electric Boogaloo) is something I've been dreading the past couple of years. It's not that I disagree with your decision, but it would result in a material, significant loss to me and many of your readers...and future generations. I remember at least one other commenter saying that he was building a

personal repository of your most thought-provoking articles so he could

bequeath the intellectual hoard to his kids. The idea has stuck with me, though I haven't begun wholesale copying of your content out of respect for your intellectual property.

This next sentence sounds disdainful, but I'm typing them candidly with no contempt in my mind: I grew up in a world full of average (i.e. mediocre) people; I listened to conventional wisdom for 20 years, achieved conventional results for 20 years, and was never satisfied. Your writings cut through my natural desire to conform. They taught me things no one would ever teach me in school. They showed me a better way to guide the course of my life. I'm no longer rudderless, so when you drop the veil over your old writings I'll find other ways to succeed...but a lot of other people who are still adrift will suffer. I'm thinking of a friend's younger brother (about to enter high school) who is energetic, very smart, and aspirational. He's been receptive to the prospect of self-improvement and learning finance...but he doesn't even know where to begin. He lacks role models. He's unfocused. He's confused and distracted by all the "conventional wisdom" because he's never met anyone who broke the mold. I was hoping to introduce him to your writings, so he can become a heat-seeking missile (in Bedell's terms) at a young age.

Have you considered re-releasing your earlier content as "Scribblings of a Younger Me" or something to that effect? Unabridged, unedited, uncensored. Even if your earlier writings have typos, are painfully honest, and not quite suitable for your rebranding, I consider them to be indispensable components of your legacy. Personally, I found the meandering, 4-in-the-morning ramblings of "Professor Kennon" to be organic and fractal-like, cf. focused, sterile white papers on specific topics. I feel like the former will help people mature into better adults in general while the latter are great if you want to dive into something to master it.

Steve Roberts

May 31, 2016

Replying to Gilvus

Yes! When I find one of those 'old' articles that might be purged and resonates with me, I make a copy (Sorry Joshua) so at least I can reflect upon it later. Sounds like I need to copy the whole blog now.....

Yes I understand that they might be rough or young or not safe for public consumption, but in a world where every conversation I have seems to lack basic critical thought (especially during an election year) it reminds me that critical thinking is still important and we need a safe space (boy I hate using that term) to express those hard thoughts, ask those hard questions and work through them (for better or worse).

Joshua Kennon

May 22, 2016

Replying to Jeff

I understand how you feel. Unfortunately, trade-offs have to be made and like @Gilvus said, the recent comments section was an eyesore in the new design. I couldn't get it to look right and had to prioritize other things. Maybe someday we can return to it and try to get it implemented but that might be a long time in the future or never.

In the meantime, here's a workaround that should be far better than the short snippet of five recent comments that was in the sidebar.

1. Go to Feedly and either create an account or login with one of your social media accounts (it's free)

2. Once in your new account, click "Add Content" and then, in the box that appears (under "Discover and add content to your feedly") copy and paste this URL, then press enter: https://www.joshuakennon.com/comments/feed/

3. When a box comes up on the page, press the green plus sign to add it to your Feedly reader display. A bar will open to the left and allow you to create a new collection to which you want to add it. Think of it like an inbox. If you did this for other blogs, all of the comments would be mixed together in there for you to read. If you wanted to restrict it exclusively to my blog, just name is something like "Joshua Kennon Comments" or something.

4. You should be able to see the site's comments in chronological order. If you want to read them in their entirety, you can use the "Full Article" view by clicking the gear in the upper right corner. Otherwise, you can view them like a gmail account using "Title Only". There are a couple of other views, too, if you prefer those.

You can do the same if you want notifications of new articles. Add another feed using the URL https://www.joshuakennon.com/feed/ instead. I think there are currently 782 readers who do this. You can't read them in the RSS feed but they will show you when a new piece is published.

When new comments are visible, they are the only thing that show up in the feed. Once you've glanced at the page, if you click on it, again, it brings up the archive of all comments.

That will let you keep track of everything being said on the site, I believe. I use the Disqus admin panel myself but for a non-moderator, this is the closest thing to a top-level view you can get if you enjoy following and participating in discussions. You'll be able to see when certain pages go viral. Recently, one old post got passed around on Facebook and experienced thousands upon thousands upon thousands of incoming readers with a bunch of comments. There's no sign of it on the front of the site but if you use this tool, you would see it unfolding.

I'm not sure what the RSS delay is for the comment thread is on Feedly's platform (they certainly aren't instantaneous) but they do tend to show up rather quickly most of the time, at least within a few hours.

I hope that helps!

Jeff

May 25, 2016

Replying to Joshua Kennon

Thanks!!

lrdey

May 27, 2016

Replying to Joshua Kennon

Thanks for this!

Also a little quick buzz, Crohn's should be the correct spelling.

Joshua Kennon

May 27, 2016

Replying to lrdey

No problem! Thanks for letting me know about the typo. I fixed it and republished the piece so it should show up once the caches have been cleared.

John

May 21, 2016

How about Amazon? 500+ x earnings but a value friend tells me its a fair price to pay for an amazing business

Ang

May 23, 2016

Replying to John

The funny thing about Amazon is that half of its profits now come from AWS - which puts it in the same boat as the Microsoft, IBM, and Googles of the world (although not EXACTLY the same business). I think people just get enamored with the revenue and revenue growth (you see the same thing happening with sales force) and forget that a business is only worth the future cash it can produce. If all of it goes back into the business in terms of lease expenses ("hidden" as financing activity as opposed to operating on the cash flow statement) or discounts, then you won't ever be able to get a benefit from it as an owner

That said, I don't think anyone would disagree when people call it an amazing business, or that it has improved the quality of life (some through convenience, but mostly by enacting the ever important capitalistic facet of creative destruction upon the retail industry - lowering costs for consumers much like Walmart did before them)

Todd

May 22, 2016

Hi Joshua - Have you seen Vanguard's new International High Dividend Yield fund (VIHIX)? Nestle is the top holding at ~3% and it contains many of the other international stalwarts you often mention. In my view, a combination of VHDYX and VIHIX gives you a portfolio with low-cost exposure to nearly all of the high-quality, high-yielding mega caps around the world.

Travis

May 24, 2016

Fidelity automatically withheld the reduced 15% rate but Interactive Brokers withheld the full 35%. Response from IB was:

Please be advised that IB is unable to submit elections to the Depository on a per-client basis regardless of account type. As such, one dividend tax rate is applied and the withholding is passed through to the shareholders upon payment of the dividend.

Since you are a US citizen, you may be entitled to a reduced tax rate in which you will need to reclaim the funds at the end of the year. You may contact a tax advisor on how to reclaim this withholding tax as IB cannot reclaim tax on behalf of our clients.

jack's smirking revenge

May 25, 2016

Replying to Travis

I got the same message from Scottrade! Argh! Anyone have a full list of brokers that support the reduced withholding?

We should be able to still get the difference back on our taxes (foreign tax credit), subject to confusing limits...

Kyle

May 25, 2016

Replying to jack's smirking revenge

Last year share builder(capital one) took out the full 35% and we had to get the difference back when we did our taxes this year. Our dividend amount was under the IRS limits, so we didn't have to do any extra paperwork(Joshua has written about the required paperwork in the past) When I called ShareBuillder to complain, I received a similar response to that Travis got from IB.

This year though Sharebuilder updated their system and only took out the 15% rate which was a pleasant surprise.

Eric Vaughn

May 25, 2016

Replying to jack's smirking revenge

TD Ameritrade only withheld 15%. Same as the past few years.

Steve Roberts

May 25, 2016

Replying to jack's smirking revenge

Tradeking withholds the 15% rate (where applicable)

I have this for a number of foreign stocks in that account.

FlyerM

May 25, 2016

Replying to jack's smirking revenge

Wells Fargo Advisors withheld 15%

Jeff

May 25, 2016

Replying to jack's smirking revenge

Merrill Lynch does it correctly.

Klint

May 26, 2016

Replying to jack's smirking revenge

Vanguard also withheld only 15%

Steve

June 3, 2016

Replying to jack's smirking revenge

Computershare withheld 15%

Born97

May 30, 2016

We delivered organic growth of 4.2%, composed of real internal growth of 2.2% and pricing of 2.0%. Sales were CHF 88.8 billion, impacted by foreign exchange of –7.4%. The Group’s trading operating profit was CHF 13.4 billion with a margin of 15.1%, down 20 basis points on a reported basis affected by the strong Swiss Franc, up 10 basis points in constant currencies. This performance was achieved while we again increased substantially our investment in brand support, digital, research and development, and our new nutrition and health platforms. Net profit was CHF 9.1 billion. The reduction of CHF 5.4 billion versus last year was mostly due to the one-off impact from the disposal in 2014 of part of the L’Oréal stake combined with the revaluation of the Galderma stake. There was also some effect from foreign exchange. Earnings per share at CHF 2.90 were down 36.1% for the same reasons. Underlying earnings per share in constant currencies increased

by 6.5%. The Group’s operating cash flow remained strong at CHF 14.3 billion and free cash flow was CHF 9.9 billion or 11.2% of sales.

is just the real eps 4.19 chf: 74.00 chf result P / E 17,66?

Bob Snelgrove

June 7, 2016

According to Fidelity, the dividend peaked in 2014 @ $2.417, dipped to 2.276 in 2015 and was 2.319 in 2016, all Q2 stats. Is this accuarate? I thought the article said they have steadily increased the dividend over time?

Steve Roberts

June 8, 2016

Replying to Bob Snelgrove

You need to account for the exchange rate (which varies from year to year)

If you are collecting your CHF in Switzerland, it has increased every year.

http://www.nestle.com/investors/sharesadrsbonds/dividends

neil5

June 27, 2017

I know that Nestle is a good company, however I personally hate dealing with the foreign withholding tax issue. Is there a minimum of 15% foreign tax withheld on dividend payments for this holding? If so, then I assume there is no reason to hold Nestle in a tax-sheltered account such as an IRA where foreign tax withheld cannot be recaptured when paying US taxes (as I understand it).