Thoughts on Berkshire Hathaway’s Intrinsic Value – 2015 Edition

Three years and seven months ago, I wrote about the intrinsic value of Berkshire Hathaway. At the time, the stock price was $73.17 per Class B share and we had been buying quite a bit of it throughout the year. I spelled out my reasons for believing the stock was trading for “far less than intrinsic value” and argued (in a rare change for me given I’m usually more, not less, conservative than most analysts) that the analysts and research houses covering the stock, Morningstar in particular, had significantly underestimated the economic engine and real earnings of the firm. Within four months of that post being published, Morningstar revised their intrinsic value figure to something I considered more reasonable.

One of the reasons I found it attractive was the fact that an owner buying at that price could wait 12 to 18 months and find himself or herself in a position of having a cost basis below book value. In many cases, book value doesn’t matter because a firm has engaged in huge repurchase programs that change the utility of shareholder equity for this sort of analysis; e.g., AutoZone. Sure enough, that happened on schedule. The past few years have been so good at the operating level that as of the end of first quarter, book value now exceeds that $73.17 price by 35.775%, coming in at $99.34 per share.

The market value has become more reasonable and the shares trade at $145.26 each, representing an unrealized gain of $72.09, or 98.52%. At one point, the gains on the Berkshire Hathaway and Wells Fargo holdings in the KRIP pushed those two stocks alone past the 52% of holdings market, which is not my idea of prudence so, despite them still being cheap, I engaged in what I call horizontal risk shifting and sold some off, especially in tax-free accounts so I wouldn’t lose any deferred tax benefit, buying up other great businesses that offered the same discount-to-intrinsic value and underlying economic prospects.

A year and two months ago, I posted an annual review of the results explaining that I had been having my own family, including my extended family members, continuously buy up shares for the accounts mentioning that the last purchase had occurred on February 11th at $112.61 per Class B share. In our accounts, the other stocks had blown past Berkshire Hathaway, making it a relatively smaller position so I felt comfortable from an allocation perspective buying more.

So here we are. Berkshire Hathaway represents the 5th largest position in the KRIP (it dropped a couple of relative weight rankings due, in part, to significant additions to two other holdings in the past nine months, including Diageo, PLC, which I’ve been buying like crazy over the past seven months). It’s at $145.26 per share in market value. It has a book value of $99.34 per share. There are 2,464,547,053 Class B equivalent shares outstanding. What do I think of the insurance, energy, and transportation conglomerate these days?

Berkshire Hathaway’s Earnings Power Has Increased Tremendously Over the Past Decade

Surveying the most recent ten year period, the increase in Berkshire Hathaway’s economic engine has been breathtaking. The Great Recession of 2008-2009 gave it the opportunity to lay out billions upon billions of dollars in cash it had been storing for years prior at terms that were unlike any deals we’ve seen in decades. Convertible preferred stocks, warrants, private buyouts … the firm got its on hands highly lucrative securities, many of which were privately negotiated and offered return enhancers not available to average investors; businesses such as Bank of America, Dow Chemical, General Electric, Burger King / Tim Horton’s, H.J. Heinz, and Goldman Sachs. Its outright acquisition activity added substantially to the earning power. It’s true that the real fortunes are made during collapses as those with foresight gobble up assets on the cheap.

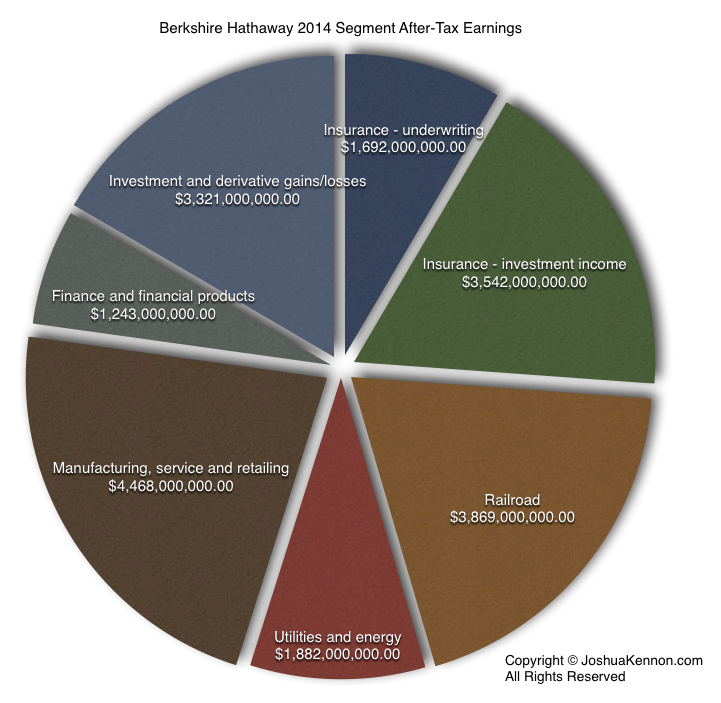

On page 86 of the annual report, you find the after-tax profit by segment for 2014. Leaving aside the $145 million expense for “other” (which matter but are a rounding error in this case so for simplicity, we can discard it for the time being) the net earnings came to $20,017,000,000.

However, as mentioned on page 6 of the annual report, there is another $3,300,000,000 in net income not included due to accounting rules. These are the non-distributed retained earnings generated by stock positions in the equity portfolio; e.g., the profits from Coca-Cola, American Express, IBM, et cetera that were not paid out as dividends. Since Berkshire Hathaway doesn’t own enough of these businesses to qualify for tax-free dividend payouts like it can with its controlled subsidiaries, there would be some tax hit were that money to be sent to headquarters but it’s still a whole lot of purchasing power that belongs to Berkshire Hathaway not showing up in the earnings per share figure or the pie chart (see below). That matters.

Adding back some other small items, this means when you look at Berkshire Hathaway’s earnings per share for the Class B stock, it comes to $8.06 + non-recorded look-through earnings on the common stock portfolio. Leaving aside those non-recorded look-through earnings that are every bit as real as the other profits, the current price-to-earnings ratio on the stock is 17.99x, representing an earnings yield of 5.55%. That’s not directly comparable to other operating businesses because that $8.06 doesn’t represent underlying operating earnings but, rather, is influenced by the investment portfolio, which can fluctuate wildly year-to-year depending upon dispositions and market conditions.

Berkshire Hathaway is sitting on almost $60 billion in cash (with a $20 billion minimum necessary for operations, this represents around $40 billion in surplus money sitting there, earning nothing, that could someday be put to use with lightning speed), real earnings and assets are higher than they appear once you dig through the accounting rules, and the utility segment is almost certainly going to expand drastically in coming years since it represents an opportunity to put to work the tens of billions of dollars being pumped out from the furniture stores, jewelry stores, insurance underwriters, candy companies, mobile home manufacturers, and other enterprises. (There aren’t many other sectors capable of absorbing that kind of capital in a meaningful way while generating good returns. Absent some sort of unforeseen change in market conditions, I think it’s only natural it’s going to come to represent a far larger percentage of the pie over time. There is still a lot of potential for future growth. The same goes for the railroad. Union Pacific, BNSF’s major competitor, is significantly more profitable. It can make a lot more money if it’s managed well, especially now that it has Berkshire’s enormous financial backing.)

Long story short, if you asked me to come up with my estimate of intrinsic value per Class B share, I’d say with a high degree of certainty it sits somewhere between $160 and $170. If you could get your hands on the entire thing (not many folks in the world are capable of such a feat), you could pay a bit more and do fine. The implication is clear that I think it’s still undervalued at a market price at $145.26. Though nothing in this life is certain – crazy things happened and even great empires fail – a person buying today, at this price, should have reason to be fairly confident that he or she might enjoy a satisfactory outcome after 10+ years have passed.

Specifically, you can’t predict the timing of market prices with any certainty – it’s a fool’s errand so don’t even try – but you can probably say that absent some sort of major unexpected event or conditions, Berkshire Hathaway’s intrinsic value per Class B share should be no less than $350 and no more than $500 ten years from now, adjusted for any subsequent dividend payouts. To move beyond either side of those ranges, you have to assume a lot of things go very wrong, or very right. Modeling for almost all reasonable growth rates, economic conditions, likely interest rates, and other variables puts you within that proximity.

Conclusion: Were I constructing a portfolio with new money, Berkshire Hathaway shares would be on the purchase list. It’s not nearly as expensive as some other firms and also seems reasonably valued on an absolute basis. You don’t have the right to expect more than this out of the capital markets. This is what fair looks like. In fact, I plan on having some of my friends and family buy more in the coming months if the current market price (or lower) is still available as their regular deposits arrive for me to put to work. I may even pick up some for my own accounts but there are two or three other businesses I’ve been wanting to add as cash levels replenish following the Diageo purchases.

I Do Wonder Why the Regulators Haven’t Considered Breaking Up Berkshire Hathaway

One question I have – and maybe I’ll write more about this someday – is why regulators haven’t broken the place up, yet. Despite my lifelong love of Berkshire Hathaway, and my very real own financial self-interest in seeing it kept together, any intellectually honest self-reflection requires me to admit that, while it doesn’t fit the technical definition of a “systematically important financial institution” as far less than 85% of its revenues come from finance or money related activities, no rational civilization should be content with the sort of concentration of economic and political power that has found its way into Omaha.

This is a single firm that now wages staggering influence in nearly every sector of the American economy. It controls major energy production and pipelines; transportation and distribution businesses; insurance empires; it holds major ownership or warrants in American Express, Wells Fargo, U.S. Bancorp, Moody’s, Munich Re, and Goldman Sachs. It sells $13 billion or so per year in merchandise to Wal-Mart while simultaneously holding 2.1% of Wal-Mart’s shares, excluding its cut of indirect sales from its huge Coca-Cola stake (and, for years prior to the scheduled exchange, Procter & Gamble). It holds majorly influential financial positions in Dairy Queen, Burger King and Tim Hortons, along with Heinz-Kraft and the distribution business, McLane, which counts among its major customers Yum! Brands’ KFC, Taco Bell, Pizza Hut, and Long John Silver’s franchises.

I love all of these profits coming in, and have been significantly enriched by them due to a habit of buying for most of my adult life whenever conditions were favorable, but as a citizen, the anti-competitive concerns are huge for me on a personal level. If Teddy Roosevelt were alive he’d have taken a 2×4 to the place and I can’t say I’d blame him. What sane society thinks this is permissible? The potential for abuse is even greater than at larger firms like Exxon Mobil due to the nature and specifics of the holdings. Reading the annual report this year, I felt for the first time not a sense of pride, but of shame and a whisper in the back of my mind: “This shouldn’t be permitted to exist.” There’s something that strikes me as immoral about it, whereas I don’t feel that way about McCormick holding 50% of the domestic spice industry because it’s contained within the spice industry itself.

I know Warren wrote about the disadvantages of a breakup or spin-off (especially as it pertains to tax law) in his follow-up 50 year anniversary special letter after the actual annual stockholder but he conceded that a regulatory distribution might someday be required as it was with the company’s bank a few decades ago. The only saving grace is the wisdom Buffett and Munger have displayed in keeping leverage so low and maintaining “oceans of liquidity” as he so accurately put it. I get the sense, in a very real way, the only reason it’s given a pass is because of their influence and historical record for good stewardship, citizenry, and regulatory cooperation. Were anyone else at the helm … I’m not so sure it would avoid scrutiny. I’m not so sure it should.

Update: Several years ago, I placed this post, along with thousands of others, in the private archives. The site had grown beyond the family and friends for whom it was originally intended into a thriving, niche community of like-minded people who were interested in a wide range of topics, including investing and mental models. On 05/22/2019, I decided, after multiple requests, to release selected posts from those private archives if they had some sort of educational, academic, and/or entertainment value. This special project, which you can follow from this page, has been interesting as I revisited my thought processes about a specific company or industry, sometimes decades later. In this case, reading about how we approached the analysis of a real-world business was helpful to many of you and the information contained herein is now so old there is no chance a reasonable person might mistake it for current market commentary.

One major change that has occurred in the years since this post was originally published: Aaron and I relocated to Newport Beach, California in order to have children through gestational surrogacy. Within a window of a couple of years around that relocation, we also sold our operating businesses and launched a fiduciary global asset management firm called Kennon-Green & Co.®, through which we manage money for other wealthy individuals and families. That means we are now financial advisors (or, rather asset managers operating under an investment advisory model as we are the ones making the capital allocation decisions rather than outsourcing those to fund managers or third-parties), which was not the case at the time this was written. Accordingly, let me reiterate something that should be perfectly clear: this post was not intended to be, and should not be construed as, investment advice. Also, for the sake of full disclosure, I’ll state outright that Aaron and I still own shares of Berkshire Hathaway personally and that the stock represents one of the major equity holdings of our firm’s private clients. We express no opinion as to whether or not you should buy it. Any company can do poorly or even go bankrupt. There are no guarantees Berkshire Hathaway will generate a profit or make money for shareholders. We may buy or sell Berkshire Hathaway for ourselves or our clients in the future and have no obligation to update this post or any other historical writing. You should talk to your own qualified, professional advisors about what is right for your unique circumstances, goals, objectives, and risk tolerance.

Reader Comments (29)

Comments are presented chronologically, with replies indented beneath the comments to which they respond.

innerscorecard

May 17, 2015

You often allude to "managing" (I use quotation marks because I don't know the details of the arrangements and it may not be true in the technical custodial sense) the money of not only multiple family members (not just immediate family members too) but also friends. How do you find time for this, as it by itself would be a full-time business (many a person makes a decent living off a $10 million RIA managing basically the money of friends and family...well, and fools too of course), but obviously it isn't for you (and I suppose doesn't even generate fees for you, although I'm not asking you to disclose this if you don't wish to!)?

Joshua Kennon

May 17, 2015

Replying to innerscorecard

Without getting too specific: My entire life is arranged around what I want to do. I figure out the activities I love and reserve those for myself. Everything else is either 1.) automated, 2.) outsourced, or 3.) discarded. I keep my schedule completely open in almost all respects, despite working quite a bit, so I have the flexibility to go with whatever mood I'm in or project I want to focus on at the time, riding a productivity wave. I also have a slight obsession with 1.) scalability and 2.) efficiency.

I spend a lot of my day reading annual reports and deciding what to buy. It requires little incremental time outlay on my end to add one more pool of capital to something I was doing, anyway. With technology the way it is these days, everything else can be taken care of for the right price. Someone could walk up to me right now and, say, "Joshua, I want you to setup a global portfolio for [$x] million on a 1.25% fee" and my day will literally look nearly identical to how it does now. My work process wouldn't change. My schedule wouldn't change. I'd do what I wanted to do - find things to buy, analyze what we already owned, and think about ways to reduce risk - while automating or paying others to take care the tasks that I find boring or that cut into my personal time.

Life is too short to do things you don't want to do. I chose my house, in part, because the neighborhood hired lawn and snow service so I'd never have to worry about how the yard or driveway looked, just pay the fee. If a conflict arises between my time and money, time wins. Time is more valuable. I'd rather have the freedom to go to a movie with Aaron or learn a new pie recipe than give up for more money. I can always make money. I can't get back time spent doing something I didn't enjoy.

innerscorecard

May 17, 2015

Replying to Joshua Kennon

Of course the answer is quite simple!

But it is just that managing money is just such a sensitive thing - we all know the stories of clients of even the best money managers demanding harmful changes in allocation or selling out at the worst money - you are truly blessed to have friends and family members who give you their trust, and also very admirable for taking on that burden for others.

atic

May 18, 2015

Replying to innerscorecard

If I was a person in his family I'd be pretty fire and forget about it too. Less stress in my life, and he beats an index fund :p He's a special kind of ETF, and how much do you interact with an ETF beyond buy and sell on your brokerage website?

stegner

May 17, 2015

Curious on your thoughts on this : http://www.thorntonoglove.com/blog/october-09th-2014

O'Glove believes that sooner or later it will happen, for matters of value.

Dave

May 18, 2015

Reading your paragraphs on anti-trust and breaking up Berkshire Hathaway, I am reminded of a story of John D. Rockefeller. On May 15th, 1911, Rockefeller was out golfing with a priest from the local Catholic Church, when he received word that Standard Oil had been declared a monopoly, and would need to be dissolved.

Rockefeller turned to the priest and asked, "Father Lennon, have you some money?" Startled by the question, the priest said, "No, why?". Rockefeller replied, "Buy Standard Oil."

Alex

May 18, 2015

Replying to Dave

+1

It seems to me that most people are under the impression that the break up of Standard Oil was a devastating event for Rockefeller, when in fact it gave him significant positions in several large oil companies that were now being valued at a higher multiple than they would have been under the trust. The break essentially unlocked a lot of suppressed value as these companies went on to grow from titans to behemoths. In fact if it wasn't for the huge power and advantages that the trust held, Rockefeller should have broken it all up himself.

Eric

May 31, 2015

Replying to Alex

Like Munger said in the annual letter, when companies merge, they site cost synergies, and when they break up, they cite unlocking value.

segfault

May 18, 2015

Something I noticed in the most recent annual report: Buffett has for years cautioned that Berkshire's returns won't be as spectacular in the future and that there will come a point when the enterprise is too large to deploy its capital in a way that it may profitably expand. In the most recent letter, I believe he gave a timeframe of 10-20 years for this to occur. I'm not sure whether this is his pessimism, but it sounds plausible. Even if this is true, it doesn't change my positive feelings about the company.

Erich

May 18, 2015

Your analysis of Berkshire Hathaway in the past has been rather accurate but I find the following statement hard to believe: "Berkshire Hathaway’s intrinsic value per Class B share should be no less than $350 and no more than $500 ten years from now" Your statement implies that Berkshire Hathaway is likely to provide returns at or above the typical return for the broader market (at least, what the market has provided historically). First of all, don't you think there is a high probability of a market crash within the next 10 years as equity prices are somewhat inflated (and will likely continue to inflate for a little while longer) due to sustained ultra low interest rates globally? In other words, I find it hard to believe that Berkshire Hathaway will provide market beating results over the next 10 years at its current price; i.e., could you perhaps elaborate on your analysis?

Bob

May 18, 2015

Replying to Erich

I'll jump in and answer with my own overly-simplified analysis. The average company (and the S&P 500 to boot) has returned between 10-12% on equity for the past hundred years or so. Buffett claims that Berkshire should outperform the average company over the long term. So if we assume it compounds book value at a rate of 13% per year for the next 10 years, you get a book value of $339.46.

I think Josh assigned a book value multiple of between 1 and 1.5 to arrive at $350-$500 range.

Berkshire's valuation is less affected by the current low interest rates than maybe the broad market. For one thign, if interest rates increased, Berkshire's investment income would increase. Also, it's unlikely that the shares would ever trade below 1x book value, regardless of where interest rates are.

Breathaholic

May 18, 2015

Joshua,

Hope all is well. I am surprised by your comments about antitrust, not that I should know what you will think, but based on your general admiration for the company. Would you share why you were struck with such line of thinking now? I mean BRK wasn't any smaller last year, not in relative terms at least. And Warren and Charlie never really shied away from making their political views public 10 years ago. Or in case of Warren thrown his weight behind the candidates, he even announced Hilary's run before Clinton did herself for 2016 while at Fortune's conference. Anyway, just wondered what caused your views to shift.

Incidentally, he did say at the meeting this year that he expects with high probability to buy a large business in Germany over the next 3 years. When insurance rates went negative in Europe, I thought it would give BRK great chance to snap up some insurance companies in Europe, given the european landscape I hope it would be German. Iscar is completely foreign operation already. So, maybe BRK will expend outside of the borders just to get diversified in terms of broader geography.

It can't happen, but I hope uncle Warren buys us all of Nestle:) And also gets to add all of Kinder Morgan to BH Energy. If those things were to happen your outer bound of $500 would be breached, otherwise I think doubling from here in ten years is the least that would happen.

Be well.

Tom T

May 19, 2015

On an unrelated note HSY is starting to be valued at an OK price.

Joshua Kennon

May 19, 2015

Replying to Tom T

I completely agree; in action, too, not just theory. I've had family members place several buy orders for the "hold for the rest of your life" portion of their assets within the past few weeks, including one for my brother fifteen minutes ago and one for my mother-in-law (along with more Berkshire Hathaway) yesterday.

It's not a screaming bargain by any means, but it's certainly fair (especially for an economic engine of that calibre). Even if the world falls apart tomorrow and it collapses, losing 2/3rds of its market value, I have a difficult time envisioning a set of circumstances that leads to someone buying at this price not being happy with the decision in 10, 15, 25+ years. The underlying earning power is fantastic.

Bob

May 20, 2015

Replying to Joshua Kennon

I'm not too sure I understand where you guys are approaching your HSY valuation. in the past 10 years, there has been basically 0% increase in the book value per share. The payout ratio is about 50% - so where did the other half of the earnings go?

Eric

May 31, 2015

Replying to Bob

I don't know if book accurately represents Hershey's value. It's really hard to put a value on the brand name and the economic moat they've dug. I'd say a better way to value it is in the earnings yield, which right now looks to be just north of 5%.

Joshua Kennon

June 15, 2015

Replying to Bob

It has to do with how GAAP treats share repurchases on the balance sheet as they are a form of "back door" dividends that reduce book value. When the fiscal year began 10 years ago, there were 246,590,000 average shares outstanding. At the end of 2014, there were 220,830,000 average shares outstanding. That means over the time period in question, the board of directors effectively had the chocolate giant use its cash to buy back 25,760,000 net shares, or almost 10.5% of the company. Those shares now don't get included when Hershey divvies up its earnings as they no longer exist.

For buy-and-hold owners, this means that each remaining share represents 11.6%+ more ownership than it did a decade ago because each share represents 1/220,830,000th ownership, not 1/246,590,000ths ownership. That's a big difference. It's the equivalent of someone who had 100 shares back at the end of 2004/start of 2005 being gifted 11.6 free shares along with the aggregate cash dividends they'd have received along the way.

The "missing" money, or book value, on the balance sheet is from the cash the company gave to the selling stockholders who handed over the 25,760,000 shares that were nixed. All those individual investors who put sell orders in with their stockbrokers might have had no idea the buyer on the other side was The Hershey Company itself; that the cash they were given came from profits and was being used to reduce share count. In a few cases, Hershey would buy back stock from The Hershey Trust itself, which holds a huge concentrated block, to help the trust diversify and make it easier and more efficient to facilitate the buy back program.

Hershey's returns on capital are so high, and its payout so rich between combined dividends and share repurchases relative to tangible capital, that book value is not a useful metric in estimating the change in year-to-year intrinsic value. Instead, you need to calculate owner earnings and then apply an appropriate discount rate to it, comparing it to what you can get for the stock market as a whole or, even better, you next, best personal opportunity.

In fact, share repurchases can create some really interesting distortions from time to time. Imagine that tomorrow, we went into a 1973-1974 meltdown and Hershey, the business, was doing just fine but Hershey, the stock, fell to $15 per share. The company would likely go into overdrive on the buybacks, which would probably make it look like book value was declining at the same time intrinsic value per share was going through the roof for buy-and-hold owners. Were you to rely on book value alone, without understanding how it fit into the overall picture, you'd get an impression that was the exact opposite of reality.

(For what it's worth, on top of the earlier acquisitions I mentioned a month ago, I had my own mother buy shares in her personal IRA this morning when the stock market opened. She just turned 53 years old and unless something extraordinary happens or some unforeseen set of circumstances arises that I don't presently anticipate, I expect to have her hold them for the rest of her life. God willing, that should be at least 30+ years so we're talking a true, honest-to-goodness long-game here. This is not something I'm buying for 2 or 3 years in the future and it's certainly not stupidly cheap like Wells Fargo was a few years ago, but it's a fair deal in my opinion; much fairer than the stock market as a whole in risk-adjusted terms. Off the top of my head, I think there are now 11 family members who are now collecting, directly or indirectly through a spouse, cash dividends from the chocolate company. As far as I'm concerned, it's in the Kennon-Green family to stay. Even if it were to underperform the market, which I don't think is likely over stretches measured in decades given its inherent advantages, the business itself has historically been much more resistant to economic storms than the average firm so I want some of it on the balance sheet at all times in case we go into a 1929-1933 collapse. I'd be willing to accept the differential as an insurance premium of sorts which, again, I don't think is likely. To give an actual illustration: Back in 2008, during the worst panic since the Great Depression, earnings per share only fell 9.6% before high-jumping more than 15% the following year. Even if you're losing your house and have no job, you can probably come up with a buck for a chocolate bar if you want one. The world's woes don't have too much of an influence on the bottom line. It's nice to have a few of those in life because even if the stock is collapsing, you know the firm itself is fine; maybe even come out of it stronger as weaker competitors are wiped off the board. But this is all just late-night ramblings. I'm not suggesting you buy any for yourself, just explaining how and why we approached it the way we did..)

Bob

June 15, 2015

Replying to Joshua Kennon

That makes sense, and now that I think of it, anytime a company buys back it's shares at a premium to book value, that will cause a decrease in book value per share. I think Hershey's is a rather large premium to book value also, because it earns an extremely high 55% ROE. I think PB is like 15:1.

A

May 20, 2015

Hey Joshua,

WYNN has gone down about 50% from its peak over the last few months due to the Chinese anti-corruption drive. Do you think the 50% drop in share price is justified? Looks like an overreaction to me despite the drop in earnings. I know you mentioned in passing that you like owning gambling stocks despite not being a gambler so any other thoughts on WYNN?

innerscorecard

May 21, 2015

Replying to A

I really think Western investors are far underestimating the Chinese central government's resolve on this one. Xi Jinping has outright said that he wants to reduce gambling by Chinese people worldwide.

A

June 4, 2015

Replying to innerscorecard

I wonder if it's a Peak Earnings trap...

FratMan

May 22, 2015

Joshua, I have shared your distaste for Buffett's pivot towards dishonesty when he enters the political realm. However, I hope you caught his editorial in the WSJ yesterday. It had sparkles of the "old Buffett" that made him admirable in the first place.

And I don't know if you have ever spoken on this, but is it fair to assume that the reasons why you buy Wells Fargo or Coca-Cola in their own right occur only when those stocks trade at cheaper valuations than Berkshire Hathaway itself? Otherwise, why give up the $62 billion cash hoard and the break-up bonanza/buyback potential of getting those companies indirectly through Berkshire?

And...as someone who talks about the importance of Wells Fargo and Coca-Cola in your own life's investment story, how do you think about what will eventually happen to those shares in the Berkshire portfolio...do you anticipate shares of Wells Fargo, Coca-Cola, American Express, and IBM being spun off to you eventually from Berkshire?

innerscorecard

May 23, 2015

Replying to FratMan

It was a great editorial, for sure. Too bad it would be unrealistic for him to push a basic income, instead.

Steve Roberts

May 26, 2015

Replying to innerscorecard

Isn't EITC the best of both worlds? It encourages work while supplementing those with smaller incomes/lower skills.

People could have said the same thing about the industrial revolution. Look at all those agriculture jobs lost! But the economy transformed itself providing better jobs and a greater standard of living for society. I see this revolution as being no different. Instead of working in factories, we are writing apps, creating websites or working in service jobs.

Eric

May 31, 2015

Replying to FratMan

I think that question about spinning off the stock holdings was asked at the Annual meeting. The answer is no.

Jay

May 26, 2015

Hey Josh, thoughts on IBM? Follow Buffett?

jhonsonally

June 1, 2015

‿(̶◉͛‿◉̶)‿ joshua is going back < www.Fox81.Com

I-I-I-I-

Jeff

June 15, 2015

I have some concerns with Berkshire Hathaway...

1) I don't like that they don't acknowledge the serious danger of solar energy to their conventional utilities portfolio. I understand there is a ton of borrowing in that part of the business, and I don't know if the danger of a large number of customers going off grid is accounted for. Look at what happened in Hawaii, even before the Tesla battery announcement. That said, it probably only represents a 3% to 5% danger to overall profits.

2) I don't like how Warren Buffett blew off the Clayton Homes scandal. The accusations are too serious to poo-poo them. While I don't think it will cost BRK any money, I don't like seeing a hero act like a schmuck.

3) I don't like how hard it is to see who owns what in the annual report. What amount of the stock portfolio is owned outright vs owned by insurance float? It could be that a) it doesn't matter, or b) I just am not reading it carefully enough. I don't like not understanding.

Joshua Kennon

June 15, 2015

Replying to Jeff

Regarding the third item: As of the end of the most recent fiscal year (2014), Berkshire Hathaway's consolidated statutory surplus (read: net worth calculated on a more conservative basis than GAAP) aggregated across all of its insurance subsidiaries was $129 billion. Float (read: money they hold but don't own on top of statutory net worth) stood at $84 billion. That is insanely conservative compared to standard industry practice (the premiums-written-relative-to-statutory-surplus ratio is one of the most important metrics when attempting to understand the inherent leverage in an insurance operation). Berkshire could easily write 3.5x the amount of business they are now but won't because of management's obsession with profitability and risk control. Buffett has talked about how decreases of more than 3% per annum are nearly impossible with the current book of business under even the most adverse of situations, in some cases involving large contracts that allowed the firm to hold on to billions of dollars for decades until the end of the term; money the customer couldn't take back even if it wanted or needed.

Looking at that in isolation is misleading because not all of the stocks are held within the insurance subsidiaries. Some of the Coca-Cola, for instance, is held at Nebraska Furniture Mart (and possibly even the NFM retirement plan) because back in the 1980's when he was using everything he had to buy as much as he could, he'd make purchases wherever the cash was sitting. Charlie Munger had piled up cash for years at Wesco when it was a controlled subsidiary that had its own independent stock listing because of a promise made to the Peters widow out in Pasadena. When the financial crisis hit, he unloaded the reserves and was buying up Wells Fargo for pennies on the dollar. (It used to be really interesting because I think prior to the buyout offers for all of Wesco in 2010, Berkshire's controlling interest in the firm was held through Blue Chip Stamps, Inc., which had declined to the point it was doing only like $40,000 a year in sales; so you had this massive sub-holding company held through this now-all-but-defunct operating business. It made uncovering the details a lot of fun.) All of this is to say, the float isn't relevant for some portion of the stock portfolio. Now, nearly all of the bonds are held within the insurance entities but that's another discussion ... he's taken bond exposure down to something like 14%, which is the lowest in 50 years. We are living in a bond bubble. I've said it before but watching him drop that number that low is shocking from a historical perspective. He's opting for outright cash, instead. That says so much.

It's a case of knowing where to search. You have to take not only the Form 10-K filed with the SEC, but the Form 13-F. Then, you have to pull the National Association of Insurance Regulators (NAIC) filings for each of the insurance companies and teach yourself how statutory accounting differs from GAAP. (I would never consider buying an insurance stock without looking at the NAIC report. It's far more useful in understanding the risks inherent in the actual underwriting and investment activities of a firm. You can request copies of the annual report of any insurance company in the country from NAIC headquarters in Kansas City by purchasing them online. You can get five for free. For the investment portfolios, you're interested in Schedules D, DA, and DB.)

On top of this, you want to look at the filings each subsidiary sends to its home state regulator as you can pick up some interesting information. For example, take a look at this PDF filed with the insurance regulator in Nebraska for National Indemnity, which is the parent umbrella through which Berkshire holds most of its insurance companies. You see that the parent company gives the insurance group a revolving line of credit (making it easy to infuse money quickly from the other operating profits). You can also get a general idea of the holding company structure. You can then pull the state regulatory reports for each of the subsidiary companies, such as this old PDF one for GEICO in Maryland.

As a kid, I loved mystery novels. Think of it like an Agatha Christie story or a game of Clue. It's the same deal. You have to uncover everything you can about Berkshire Hathaway. The SEC is just one room in the mansion - the library. There are many other rooms available depending upon the firm. Railroads have their own regulator. Utilities have their own regulator. Insurance companies have their own regulator. Banks have their own regulator. Secretaries of State have certain filings on hand (do you want to know, for example, who sits on the board of directors of a particular subsidiary?) All of which provide information the others can't; witnesses you need to interview to recreate as best you can an outside understanding of the way the firm is structured. Poke around the study; take a peek in the hall; open the cabinets in the kitchen. It's a lot of fun.